The latest data from the McDash Flash Forbearance Tracker shows that the surge in mortgage forbearance plans has tapered off.

Estimated Monthly Advances

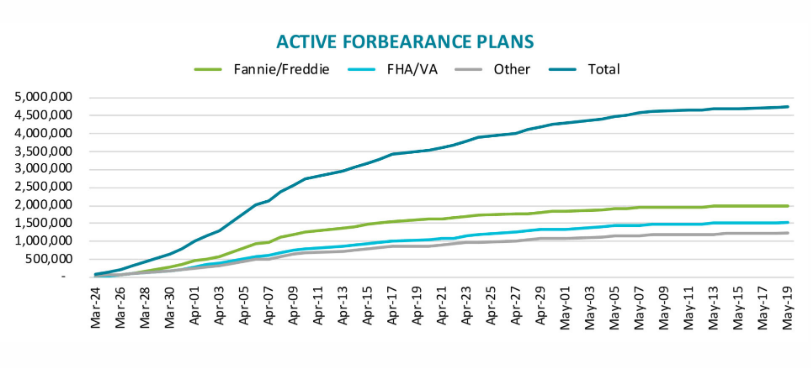

Key Points

- As of May 19, 2020, 4.75 million homeowners , 9.0% of all mortgages, have entered into COVID-19 mortgage forbearance plans.

- The unpaid principal balance is over $1 trillion.

- An estimated 7.1% of all GSE-backed loans and 12.6% of FHA/VA mortgages are now in forbearance.

- The rate of increase has now declined by 93% from the first week of April when the number of active forbearance plans increased by nearly 1.4 million in a single week.

Existing Home Sales Plunge 17.8% Much Worse is on the Way

In case you missed it, please see Existing Home Sales Plunge 17.8% Much Worse is on the Way

Mish

Basically just back to the days of the neg am loans

And more Fed bailouts for RMBS for both residential and commercial loans.

Please choose which category of loan you would like your $10,000 Biden-Warren dollars to be applied to:

….Just make sure it is all, to the penny, plus some extra, applied to one loan or another. No way would we want to risk up to several pennies ending up with someone who is anything other than a leeching bankster… That would be flat out un-American!

Ag Monster Box

And don’t forget the irony of those of us who still owe state or federal taxes using the money to pay those off ☺

I have a feeling all GSE/VA-backed loans will be re-cast into 100-year mortgages.

Where that would leave you as an MBS holder seems “unclear”.

Perhaps the Fed just buys them all at par.

Add this statistic: The number of mortgages in forbearance is more than 85% of the annual sales of existing homes for April. That speaks volume about the supply of foreclosures that will eventually be placed on the market.

No point in forbearance unless absolute only option … as lenders generally want it ALL paid back in lump sum … or extra payments in relative short amount of time.

“…as lenders generally want it ALL paid back in lump sum … or extra payments in relative short amount of time.”

In that case they should call it “deferred default” instead of “forbearance.”

When offered the chance to hold on to a significant amount of cash with no penalty and no credit hit, I’ll generally take it even if I just have to turn around and pay it anyway at some point. Life’s unpredictable – at the very least the interest on that money in a high-yield account buys me a cup of coffee and there’s no harm done when they demand the lump-sum. Or, my house could burn down tomorrow and my car could blow up at the same time and I’d be thankful I held onto that extra cash.

Lenders aren’t exactly “offering” cash, are they? Don’t you have to sign a statement saying COVID-19 has caused you economic hardship and you are not able to make your regular mortgage payment?

Perhaps not “offering”, although you would be forgiven for thinking that given that on every website for a bank or credit service operation it’s the largest banner that greets you on logging in. I think that if it is within the law for one to do so it is almost always advantageous to accept temporary debt relief that has no financial penalty or credit score repercussions attached; and in this case to my best understanding the law is very generous to the borrower regarding those economic hardship clauses.

Yes, absolutely Morn.

Mish, noticed in a west suburban local paper legal notice about a house going up for foreclosure auction sale soon. Location is on north Grant Street in Westmont, IL easily found on Zillow site. THE FORECLOSURE STARTED IN 2007!!! The banks have been hiding this inventory all along, since nobody is accounting for mark to market.

I don’t think credit stays the same with a forbearance, they will report it to the agencies who will then begin to downgrade scores.

“No point in forbearance unless absolute only option”

For the borrower, they get to stay in their house and, I believe although I haven’t verified it, keep their credit from getting immediately hammered. All while hoping enough people in swing states end up in the same situation as them, to make a bailout appear a likely vote getter.

For lenders, if they can keep up the illusion, that they’ll at some point get paid, until bonus day; they can, again, pull off yet another “bonuses then bailouts” maneuver. It’s America after all. That’s what we live off, darnit.

The rubber will meet the road in a couple of months

as 8 weeks of PPP and $600 / week extra (thru July 31st) end.

Of course, it will only take a single tweet for DJT to go from A Quick Beautiful V Shape Recovery … to Need $trillions MOAR!

Put me down for latter … especially now that Kudlow hedging his bet.

But a can kick (or 3) won’t change ultimate destination for housing. Down.