The December Construction Spending Report shows continued weakness, especially in residential construction.

Total Construction

Construction spending during December 2018 was estimated at a seasonally adjusted annual rate of $1,292.7 billion, 0.6 percent below the revised November estimate of $1,300.6 billion. The December figure is 1.6 percent above the December 2017 estimate of $1,272.6 billion. The value of construction in 2018 was $1,297.7 billion, 4.1 percent above the $1,246.0 billion spent in 2017.

Unexpected Weakness

Econoday highlights the unexpected weakness.

Construction spending fell 0.6 percent in December with year-on-year growth declining to a tepid 1.6 percent, the weakest growth rate in at least 3 years.

The unexpected monthly decline (consensus forecasts called for a moderate increase of 0.3 percent) was led by private residential construction, which fell 1.4 percent in December, as a 3.2 percent drop in spending on new single family homes overshadowed a 3.1 percent rise in spending on new multi-family units. Spending on remodeling fell 0.4 percent.

Muting the overall spending drop was a 0.4 percent increase in private non-residential construction, bolstered by a 3.3 increase in health care, a 1.7 percent rise in manufacturing, and a 1.0 percent increase in lodging.

Public construction spending fell 0.6 percent in December, driven by a 7.8 percent drop in health care, a 5.1 decrease in residential spending, a 2.9 percent decline in power, and a 0.9 percent drop in spending on highway and street construction. Partly offsetting these were increases in office construction and commercial construction of 6.4 percent and 6.1 percent, respectively.

State and local construction spending was down 0.5 percent in December, while federal construction spending fell 2.2 percent.

Year-Over-Year Comparison

Normally one uses non-seasonally-adjusted numbers for year-over-year comparisons.

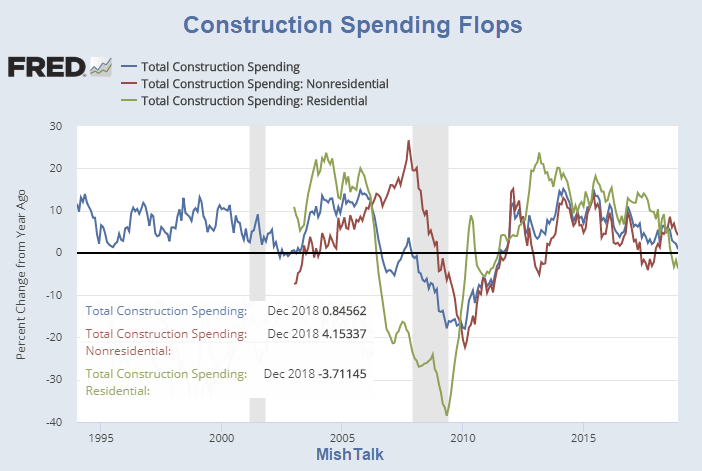

Fred shows those numbers as +0.85, +4.15, and -3.71 for overall, nonresidential, and residential respectively.

Econoday notes a year-over-year overall growth rate of 1.6%.

If one use seasonally-adjusted numbers for the comparison, Fred shows those numbers to as +1.58, +3.95, and -1.53 respectively.

No Surprise

Add this to the list of recession-looking data.

Houses are not affordable and the slowdown is obvious. No one should be surprised by this.

Mike “Mish” Shedlock

value of public construction still relatively strong at 4.2% YOY growth. The big question is how is this being funded and why hasnt the segment seen any crowding out as a result of increased Treasury issuances?

Residential flopped the most. 65% of millennial home buyers are disillusioned

with home ownership, they were unaware of the cost of maintenance/improvement. Lumber history. Mortgage interest rates up, Lumber prices falling sharply now. Could see this coming.

With immigration slowing down and even reversing in some places real estate is going to decline. There is still more empty office space in America from the credit crisis than from the 1980s commercial real estate bust.

I’m shocked I say,all those massive new gov’t building,state of the art prisons on almost every block now,hundreds (thousands)of new state of the art police palaces errrrrr stations seemingly everywhere,massive renovations on military palaces errrrr bases,brand new welfare offices,gov’t offices everywhere,Amerika is the only country that has a brand spanking new state of the art PRISON goin online somewhere every single day!!

An increase in non residential is surprising since many stores are shutting down. I guess there may be a demand for office space.

There’s huge demand for commercial space in any city. Residential as well. I doubt there’s a software developer currently occupying no more than a cubicle in all of the Bay Area, who wouldn’t like to, as a sideline venture, have a photography studio, recording studio, robotics development/test facility etc. etc. As well as 2000-5000 square foot of living space close to work.

What minuscule fraction of that is actually being built, has noting to do with demand, and everything to do with keeping the five year planners who gets to decide, in lieu of a market, what is allowed to be built.