The National Association of Realtors (NAR) reports Existing Home Sales Wane 17.8% in April

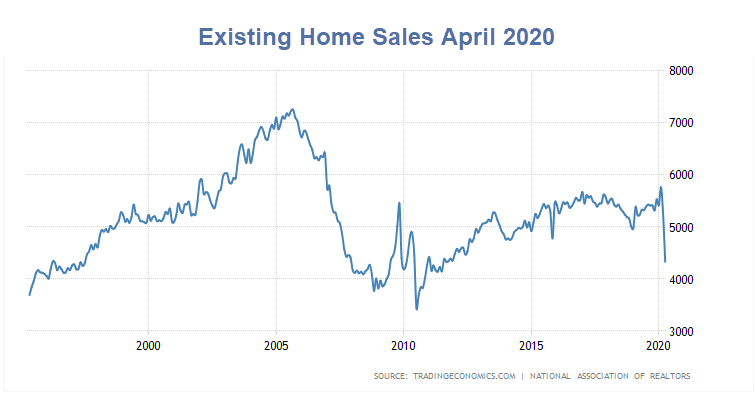

Total existing-home sales, completed transactions that include single-family homes, townhomes, condominiums and co-ops, dropped 17.8% from March to a seasonally-adjusted annual rate of 4.33 million in April. Overall, sales decreased year-over-year, down 17.2% from a year ago (5.23 million in April 2019).

“The economic lockdowns – occurring from mid-March through April in most states – have temporarily disrupted home sales,” said Lawrence Yun, NAR’s chief economist. “But the listings that are on the market are still attracting buyers and boosting home prices.”

Immense Cheerleading

Supposedly listings “are still attracting buyers” despite the fact that sales are down 17.8% on top of a 8.5% decline in March.

Note that April’s existing-home sales are the lowest level of sales since July 2010 and the largest month-over-month drop since July 2010.

Prices Rise

The median existing-home price for all housing types in April was $286,800, up 7.4% from April 2019 ($267,000), as prices increased in every region. April’s national price increase marks 98 straight months of year-over-year gains.

“Record-low mortgage rates are likely to remain in place for the rest of the year, and will be the key factor driving housing demand as state economies steadily reopen,” Yun said. “Still, more listings and increased home construction will be needed to tame price growth.”

Not the Bottom in Transactions

April will not mark the bottom in sales. Here’s why.

- Existing sales are recorded at closing whereas new sales are counted at signing.

- April sales represent transactions that occurred in February and March.

May sales (transactions in March and April) are sure to be worse. Even June sales could be worse.

Expect Prices to Drop Too

Yun’s statements regarding sales price constitutes more cheerleading.

- Prices are up in April only because data is so skewed by the huge drop in sales.

- Many people pulled listings due to Covid-19. Sellers will want prices they could have gotten in February, but alas, those prices are gone.

- The hit to personal income ensures that a decent chunk of would-be buyers just vanished.

Grim Economic Data

- May 8: Over 20 Million Jobs Lost As Unemployment Rises Most In History

- May 15: Retail Sales Plunge Way More Than Expected

- May 15: Industrial Production Declines Most in 101 Years

To expect buyers to return en masse and price to hold up as well is irrational.

Looking to Buy? Wait!

Ignore the cheerleading from the NAR. Better prices await buyers who are patient.

Mish

Elon Musk is selling all 7 or more of his homes…getting liquid to avoid going bk. Or planning to migrate to Mars to build the city of Musk? He may throw childish tantrums occasionally but he’s a long ways from an idiot. Suspect a lot of folk with money have many homes, a sustained downturn may put plenty on the market…

Gosh, if we can just put a few more million people out of work, maybe we can tank the economy enough to get a real bargain, and provide additional contrived excuses to bail out mismanaged state and local govt’s.

Half of the 10 year housing recovery just vanished in a month. Any bets how many months it will be until the ENTIRE housing recovery has been erased?

Homeownership isn’t just for families anymore. Lots of big boys have skin in this game. You know, the TBTF kind.

Of course this looks deflationary. So does everything else but prices remain static.

That being said, Lawrence Yun obviously subscribes to the Benny Hinn power of positive thinking just like our moron-in-chief. It explains why every word out of their mouths sounds like a lie.

“The economic lockdowns – occurring from mid-March through April in most states – have temporarily disrupted home sales,”

I notice by the chart, that home sales are still temporarily down from the level they were in 2005. 15 years of temporarily.

Going forward.

Not surprising Yun failed to mention a single word on forbearance.

From Black Knight:

Black Knight says that about 46 percent of borrowers in forbearance at the end of April, 4.25 million in number, made that month’s payment while 54 percent did not.

…

But Black Knight says that May seems to be shaping up a bit differently. As of this report, only 21 percent of those in forbearance had made their May payments. This means that up to 1.4 million who made April payments are at risk of becoming past due in May. This could lead to another sharp increase in the national delinquency rate next month.

A can of paint won’t fix forbearance. Few buyers will want to include negotiating with the lien-holder as part of their home purchase process. Few lien-holders will want a house to sell at less than face value of the loan because the existing homeowner won’t be able to make up the difference; thus taking a loss. All it will take are a few cash buyers and sellers with lots of equity in their house to get a deal done to force prices in the neighborhood lower.

But as a potential seller with a ton of equity i.e. So Cal house paid off and looking to go bigger. I’m not even considering a change because it takes time for things to sort out and the top of the market compresses more than the lower and middle when the fall comes. So my Delta for the buy will be smaller later.

No one I know with equity will move unless they get paid well or are forced out. It will take a hell of a lot for that “forced out” situation to happen. A heloc for 40% of my house value will cover my living expenses for 8 years if no one in my house has a job.

People with money only take good deals because they can wait anything out.

The market wont shift because of sellers with equity. It will shift due to cash buyers and people that need to get out and will get close to break even.

Secretary Mnuchin slowly moving the economic goal posts

April 26th:

“I think as we begin to reopen the economy in May and June, you’re going to see the economy really bounce back in July, August, September,”

May 21st:

WASHINGTON (Reuters) – U.S. Treasury Secretary Steven Mnuchin said on Thursday he believes the U.S. economy will “bottom out” in the second quarter and start to improve with the third quarter, with a “gigantic increase” in fourth quarter activity.

A gigantic increase in infection rate is what he means. We are providing this virus with a high quality petri dish over the summer, and then we will all take a shower in said petri dish come “flu season”

“Yun’s statements regarding sales price constitutes more cheerleading.”

…

Yes. Re: higher price … low mortgage rates WAS a factor. Checked typical 30 yr mortgage rate for April 2019 – in the 4.25% to 4.50% range. April 2020 – in the 3.25% to 3.50% range. Ran the mortgage calculator and ~ $150 / month cheaper for $300K mortgage. Not surprising higher prices considering more Bang for buck + big drop in inventory.

Sellers pulling their homes off the market will likely rue the decision.

I’m convinced that we all got Lawrence Yun wrong. He’s really a wanna-be stand-up comedian. Granted, he’s not very funny, but he really, really tries. For years now.

Doctor Doom says decade of depression to come….and a careful reading of the Fed notes and reports say they are preparing for it…

Houses in this area are still flying off the shelf. “Good” ones don’t sit very long. It’s mostly those fleeing the NE and IL judging from the license plates and accents. As long as their cash/credit holds out they are buying anything and everything. Long term some of these building are trash (hastily built, poorly built, built to a cost) but for now, buy,buy,buy!

This region sort of dodged the 08-10 housing crash, just a slight wound. This time when it tanks, I don’t think it’s going to be a sucking chest wound. “Tech” won’t save them, it’s mostly vaporware and ‘apps’ these days.

Les, where are you located? Just curious.

Sorry. Meant to say SE. CLT,GSO,RDU.

Pretty much same here in our area still. It’s been hot in the entire region N of Dallas and Ft Worth for a while so there was a ton of momentum. But the earthquake has already occurred and the tsunami is coming.

Any property priced less than 1 million sold in a week👍🏻 That’s SoCal market. I’m looking for vacation home for myself , personal experience.

Sticker prices are not down that much….only 1%. “Real values” have decreased 18% in the last 20 years, as lower interest rates create a false sense of value. The “monthly payment” mentality. However, I stick by my opinion that 30 year mortgages in the 2% to 2.5% range are just around the corner, and that will continue to prop up the asking prices.

Again, people have to live somewhere. Housing panic is overblown IMHO.

“Housing panic is overblown IMHO.”

…

Time will tell. I think we’re in for a hard recession … and housing won’t be immune. Too much debt in the system will hold back any sort of V bounce back.

I don’t know, but a lot of home purchases in recent years have been rental investments (i.e. AirB&B, VRBO, etc.), and those investors have lost their servicing income. In addition, lots of 2nd homes out there, with property taxes heading higher to cover massive state budget deficit holes.

I don’t believe that a much weaker housing market is out of the question. I agree with Mish, I think prices will be heading much lower when the reality hits that the economy is not going to experience the V shaped recovery.

Housing prices are linked to income. With 20% unemployment income is going to drop across the board. Add to that the fact that real estate is highly over valued and highly over leveraged and you have the makings of a crash….

There’s a segment of the SFRs that were purchased post ’08 under speculative intentions: Blackstone, foreign investment, AirBNB. Mortgage rates have no bearing on this type of ownership as a lot of these homes we ‘re bought cash. These owners traded a very liquid asset for a very ill liquid asset which means they will need to drop prices more quickly than a home in foreclosure. These investors are also hedged in commercial real estate and student housing. These two assets will decline in value over the next few years. Thus, forcing these investors to sell their residential assets to cover their losses. These sales will affect the values of surrounding homes that families are looking to purchase with a mortgage.

unless you have some kind of recession proof job i would not be making any new long term commitments in terms of housing for the forseeable future. cash is king, but flexibility in your life situation will be key to survival

There may be recession proof jobs, but there is no such thing as a depression proof job.