Foreign Direct Investment (FDI) in the US should be rising. Tax cuts spur investment and the US economy seems much stronger than abroad. Nonetheless, FDI is negative.

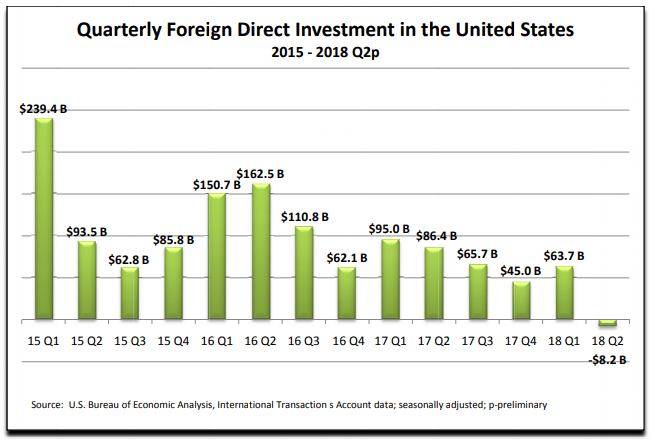

The lead-in chart is from the Organization for International Investment report on Foreign Direct Investment in the United States, Preliminary 2nd Quarter 2018.

Second-quarter 2018 foreign direct investment flows in the United States were in negative territory, resulting in a divestment of $8.2 billion, following a relatively strong first quarter. The second quarter was marked by unusually high selloff and purchase activity, which suggests that some $100 billion invested in the United States has transferred ownership abroad. In that quarter, U.S. affiliates paid off $32 billion in loans to related parties. Clearly, much of this unprecedented FDIUS activity is due to changes in ownership. Yet, it can partially be viewed as a response to import tariffs and other trade actions from the Trump Administration as international companies hit the pause button on potential investments.

Foreign direct investment in the United States in 2017 was the fourth-strongest for the past decade, but was down 40 percent from 2016. This followed record-breaking years in 2015 and 2016; FDIUS for each year reached nearly half a trillion dollars.

>These investments benefit the American economy as international firms build new factories across the United States, buoy their well established U.S. operations, fund American research and development activities, and employ more than 6.8 million Americans in well-paying jobs.

Looking at foreign direct investment more broadly, foreign companies invest in the United States for many reasons. A list of positive factors include the large U.S. market, world-class research universities, a stable regulatory regime, and a solid infrastructure that allows businesses to easily access the U.S. market.

Whether the United States will retain its status as the world’s most attractive investment location hinges mainly on future macroeconomic developments and changing financial conditions.

Annual FDI

FDI From China Alone

On July 30, 20128, the WSJ reported Chinese Investors Pulled Back in U.S. in 2017

The cumulative level of Chinese investment in the U.S. declined in 2017, according to a new Commerce Department report, showing Chinese investors’ enthusiasm for American assets was waning even before trade tensions ramped up.

China’s appetite for U.S. investment had picked up in recent years, nearly quadrupling from 2014 to 2016. Yet despite some high-profile transactions and rapid growth, China isn’t a large investor in the U.S., making up less than 1% of the more than $4 trillion of foreign direct investment in the country last year.

China’s decline stood out for two reasons. First, because of rising trade tensions between the two nations. Second, because the overall foreign direct investment position in the U.S. continued to increase last year, rising by $260.4 billion in 2017, according to Monday’s report, leaving China an outlier. The Commerce Department said the overall increase “mainly reflected” increased investment from Europe, “primarily Ireland, Switzerland and the Netherlands.”

Although investment from China to the U.S. is small overall, it has been of special concern for the White House and Congress. The administration considered a plan this year to restrict Chinese investment into the U.S., ultimately deferring to a congressional initiative to bulk up the committee that reviews proposed foreign takeovers of U.S. businesses and can recommend the president block such takeovers.

China Not Wanted

That last paragraph is telling. China accumulates US dollars as a result of China’s trade surplus with the US. It would like to invest in the US but can’t.

Meanwhile, the rest of the world is having second thoughts.

How Trump Is Repelling Foreign Investment

Foreign Affairs explains How Trump Is Repelling Foreign Investment

This year, net inward investment into the United States by multinational corporations—both foreign and American—has fallen almost to zero, an early indicator of the damage being done by the Trump administration’s trade conflicts and its arbitrary bullying of companies and governments. This shift of corporate investment away from the United States will decrease long-term U.S. income growth, reduce the number of well-paid jobs available, and reinforce the ongoing shift of global commerce away from United States. That shift will subject the entire world economy to greater instability.

Unlike speculative flows of capital or indicators of sentiment, these kinds of corporate investment decisions must be taken with 10-, 20-, or 30-year time horizons in mind, and once undertaken, they are difficult to reverse. As a result, if the relative attractiveness of investing in the United States compared with other countries—in terms of freedom from government interference, of dependable access to global markets for both inputs and sales, and of brands and hiring being helped, not hurt, by association with the United States—declines, so should direct investment in the United States.

The numbers are clear. To compare like for like, look at flows of foreign direct investment (FDI) into the United States in the first quarter of 2018, the latest for which data are available from the U.S. Bureau of Economic Analysis, and in the same quarter of 2017 and 2016. In the first quarter of 2016, the total net inflow was $146.5 billion. For the same quarter in 2017, it was $89.7 billion. In 2018, it was down to $51.3 billion. This decline was not driven by changes in Chinese investment, which flows both ways and so contributes little to changes in the net figure.

Self Harm

The decline is all the more worrying since many factors should have been pushing direct investment in the United States up this year. The massive fiscal stimulus passed by Congress should have increased FDI in three ways: by boosting spending, which increases U.S. growth prospects; by making the tax code more favorable to production in the United States; and by cutting the corporate tax rate. Even if one discounts the direct incentive effects for business investment in the legislation, the corporate tax changes certainly encouraged investment.

Consider how the tariffs on vehicles and auto parts under consideration by the Trump administration would feed into future investment decisions by some of the world’s largest multinationals: auto companies and their suppliers. If the United States imposes the threatened 25 percent tariffs and U.S. trading partners retaliate proportionately (as is likely), the move would have a major immediate effect on the U.S. economy. The tariffs would directly cost as many as 625,000 workers their jobs. But that would not be the end of it: shuttering factories also damages the wider communities of which they are a part, hurting other businesses that rely on autoworkers.

As antimarket governments have repeatedly shown, and as was the case with the U.S. auto industry in the 1960s and early 1970s, protection stifles innovation and results in worse products for consumers in the protected domestic industry. Going down that road will, in turn, hurt overall research and development in the United States, of which investment from automakers (including foreign ones) makes up a large part, and the United States’ reputation as a place to do business.

Flows of direct investment, especially of net FDI, into the United States are therefore worth watching as an early indicator of how far the global economy has moved toward a post-American era. The signs suggest that Trump’s approach to globalization is getting the world there faster than many realize.

As Trump Hardens Stance FDI Declines

Some of the ideas in the following article are similar to those presented above. Instead, I list new ideas from the article.

The Straits Times reports Foreign Investment Diverts from US as Trump Hardens Trade Stance.

Uncertainty from the administration’s negotiation strategies around trade agreements and tariffs are causing people to think about their investment decisions, said Rod Hunter, a partner at Baker McKenzie and former senior director of international economics at the National Security Council under President George W. Bush.

Part of the concern stems from Trump’s use of CFIUS, an inter-agency government panel that reviews foreign deals for national security risks, as a way to curb investment. The administration has backed bipartisan legislation to strengthen CFIUS that is making its way through Congress.

Trump is also using 232 investigations, sometimes called the “nuclear option” in trade laws, to counter cheap imports.”The 232 tariff cases have made many of our companies pause and wonder what the next two to three years hold,” said McLernon.

Federal Reserve Chairman Jerome Powell also has voiced concern on the trade climate’s impact on investment. In a Senate hearing Tuesday, he noted that tariffs are leading companies to delay capital spending decisions.

“We don’t see it in the numbers yet, but we’ve heard a rising chorus of concern which now begins to speak of actual capex plans being put on ice for the time being,” Powell said.

Ten-, Twenty-, Thirty-Year Decisions

Let’s return to a key idea:

Unlike speculative flows of capital or indicators of sentiment, these kinds of corporate investment decisions must be taken with 10-, 20-, or 30-year time horizons in mind, and once undertaken, they are difficult to reverse.

This is yet another reason that talk of “winning” these trade wars via the methods Trump uses is preposterous.

Mike “Mish” Shedlock

What about the US Multi=Nationals?

Are they investing DIRECTLY in the USA? Are they investing their borrowed funds on the cheap -ZRP into the productive Economy like manufacturing jobs with living wages or the R&D? NO! They are using that to buy back their own shares or issue the junk bonds!

How can you put a finger at the lack of ‘direct’ investment when our domestic Corps are playing hooky? HYPOCRISY! Foreign investment is pouring into the US mkts (indirectly!) just like the money from US Corps in their buy backs!

Is this NOT an open hypocrisy and an intellectual dishonesty on display?

Are real-estate purchases included in FDI numbers? I wonder whether the drop in FDI is primarily a phenomena of trends in real-estate rather than business decisions to build factories or invest in R&D.

The tax cuts were largely fake (most businesses were already paying effectively much lower taxes through loopholes or “offshore” accumulation of profits in “foreign” shell companies coughApplecoughGoogle*), and there are structural reasons why the US economy is very uncompetitive. The long-term cost of capital in the US economy must be considered as well, especially with government taking on so much debt that will eventually come home to roost. Remember that a factory isn’t built for the next few quarters, its built for the next few decades. And the next few decades, due to the outrageous levels of consumer and corporate debt that are present, as well as serious structural issues and inefficiency, promise to be relatively dark. No point in building production until politicians are solidly committed to, for example, an efficient public sector, an efficient healthcare system, etc.

From the somewhat dubious Foreign Affairs magazine: “…shuttering factories also damages the wider communities of which they are a part, hurting other businesses … .”

Don’t we know it! Long before President Trump came on the scene, under the administration of Barry and his predecessors, the US lost something like 50-60 Thousand factories. That must have hurt many communities! At least, according to Foreign Affairs.

Any objective analysis has to note that the US has been losing a trade war for decades. Sticking heads in the sand and pretending that US tariffs are bad while Chinese & European tariffs don’t matter is not a reasoned response.

Many will point out US tariffs are “high” too. Even if true in certain categories, I believe other countries are much more effective at non-tariff barriers. I remember an argument about mid-80s Japan to the effect they were helping us by effectively not allowing us into their domestic market because we couldn’t compete. I’m for free trade philosophically, but we’ve never really had it completely and no other country will protect our interests.

Our interests include acknowledging the many losers from pre-Trump trade policy. Trump is president in large part because there are so many losers. Others, many of them politically connected, have become fabulously wealthy. Saying the jobs will never come back does not address the concerns of the losers. Since they’re already destitute, they don’t care who else loses if those trade policies are changed. I think free trade will only work if most Americans don’t even think about trade because they already have so many opportunities for economic advancement.

How much of this lack of “Foreign Direct Investment” is real estate based?

We have had a decade of Chinese laundering dirty money in real estate both in America and Canada.

Everyone turned a bling eye in the Housing Bubble v2. Everyone was getting rich.

The housing bubble is now deflating. The tide is going out.

Actually there is very little to no evidence of Chinese participation in Canadian RE. “Chinese” are basically used as a scapegoat by the locals who speculate with abundantly available bank credit. Indo-Canadian speculators are prominent participants with their veritable empires of highly leveraged RE ownership.

Basically the entirety of Chinese foreign investment into Canada can be traced back to known investment outside the RE sector. So there’s very little probability of data leakage. The weak CAD$ also supports such as well.

Yep – little to no evidence. Let’s just take Vancouver for an example:

“foreign ownership grew to account for more than $45 billion dollars’ worth of Metro Vancouver residential property. Within Vancouver city limits, 7.6 per cent of all residential properties are now owned directly by individuals “whose principal residence is outside of Canada,” by the definition of the Canada Mortgage and Housing Corporation. Roughly one in ten Vancouver condos are owned by non-residents. And that’s just the owners we know about.

Transparency International reckons that perhaps half of Vancouver’s most expensive properties are owned by shell companies or trusts, with the nominal owners commonly listed as student, housewife, or homemaker. Roughly 99 per cent of the single detached houses within Vancouver’s city limits are now valued in excess of $1 million.

I believe a lot of those ‘numbers’ came from a very easily discreditable National Bank study that did some fancy extrapolations of the situation in the SFBay area, to Vancouver. The real numbers are closer to 5%, which is still higher than the rest of Canada (at approximately 3%). Most of the foreign owners being US citizens, not Chinese.

Of course, Americans can’t really be easily cast as villains in the housing bubble “Chinese”. So its the “Chinese” narrative that’s being cast.

Without a doubt, Trump makes matters worse even if cycles are at play, and I do believe you are correct about that

This is near the end of a business cycle. The last two years of all-time high foreign investment coincide perfectly with the 8 year cycle (using band-pass filters) peak in US markets. Foreign investors are really no different than investors in the US in that they borrowed enormous amounts of debt to leverage investments in the US. With a strengthening dollar due to repatriation and rising interest rates everywhere, those debts become more difficult to repay. So less money is available for investment ANYWHERE. The global Uh-Oh moment is getting closer. Trump, is no more to blame than Obama.