Trump’s tariffs have done nothing to reduce the trade deficit.

Please consider the International Trade in Goods and Services report for May 2026, released today.

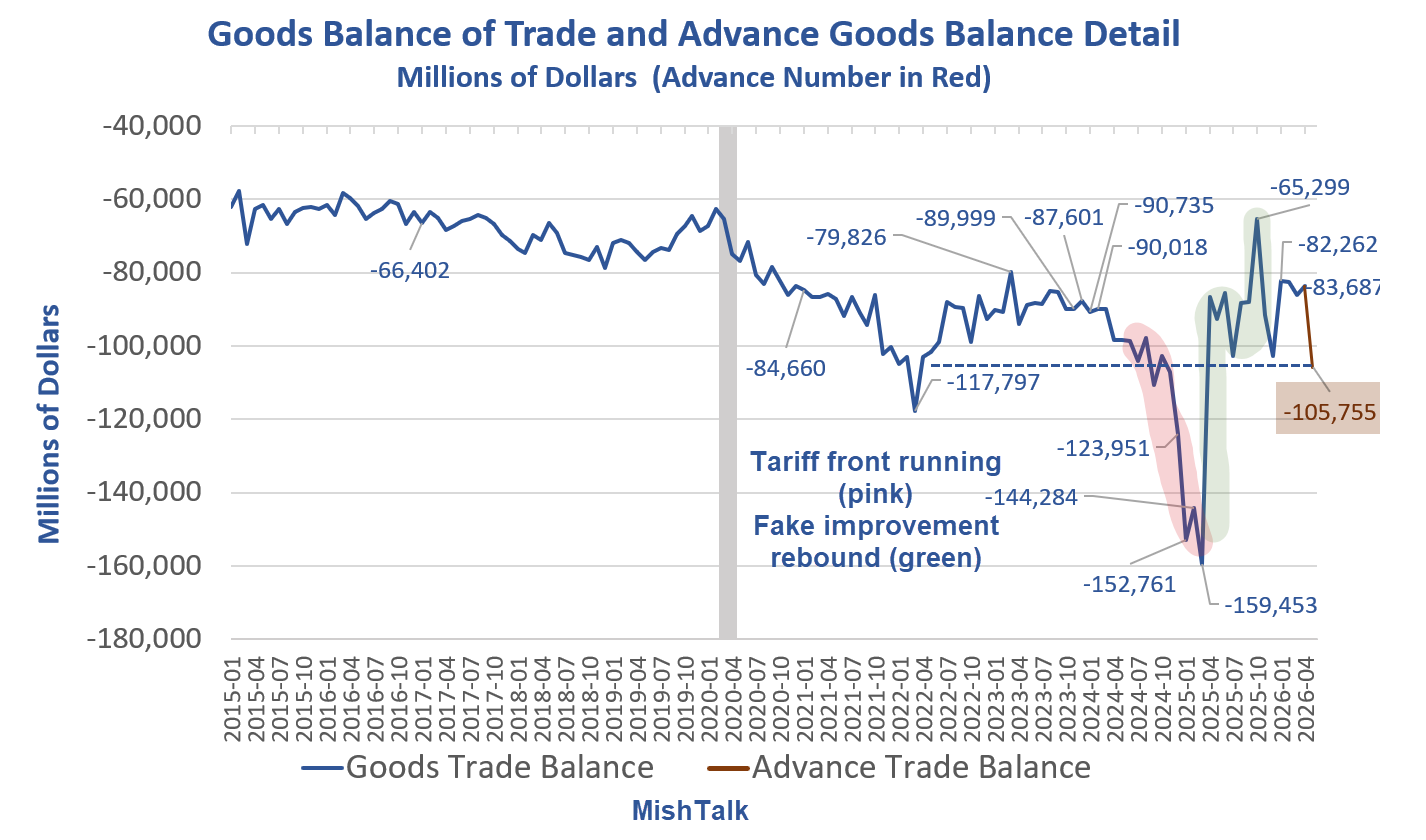

- May exports were $317.7 billion, $10.5 billion less than April exports. May imports were $395.3 billion $12.5 billion more than April imports.

- The May increase in the goods and services deficit reflected an increase in the goods deficit of $23.6 billion to $106.5 billion and an increase in the services surplus of $0.6 billion to $28.9 billion.

The lead chart shows the advance numbers for goods only. Here’s the goods and services chart.

Balance of Trade Goods and Services

Note: The St. Louis Fed data repository did not update May numbers yet. I pulled April and May rounded numbers on the above chart from the Census Department.

Trade Synopsis

- Trump massively distorted trade number for a year.

- There was huge tariff front running in advance of tariffs then an artificial and very misleading improvement in trade imbalances.

- The deficit is now right back where it started from.

Conclusion

Short of causing a recession and thus reducing demand, tariffs will do nothing to improve trade imbalances, as called in advance on this blog.

Tariffs will not restore manufacturing jobs either, also undoubtedly proven, and again called in advance on this blog.

Fundamental Problem

The fundamental problem that tariffs (nor anything else) can fix is lack of a gold standard to enforce fiscal discipline.

When Nixon removed the gold redemption window in 1971, it allowed government expansion of debt at will, creating a reserve currency curse.

US consumers because the world’s consumers of last resort. Initially, Germany took advantage, but now it’s China flooding the world with subsidized exports.

The US is continually forced to choose between recession to slow demand or huge trade and fiscal deficits.

All the talk of the Yuan replacing the dollar as a the major reserve currency is nonsense because that would require six conditions, none of which China meets.

At the top of the list, the reserve currency holder must be willing to run trade deficits, a condition that China will not let happen.

Very few understand the fundamental problem and why tariffs cannot and will not fix these imbalances.

On August 14, 2025, I commented US Debt Now Grows by $1 Trillion Every 150 Days

US national debt just topped $37 trillion and is growing fast.

Looking at recent history, by decade, the U.S. added $1 trillion to the Debt:

- Every 24 months in the 2000s, on average

- Every 11 months in the 2010s, on average

- Every 5 months in the 2020s, on average

Since August 14, debt rose from $37 trillion to $38.5 trillion.

If you think Trump’s tariffs are going to pay down that debt or do much to reduce deficit spending, you are more than a bit crazy.

Nearly a year has passed. I need to update the numbers.

Nixon Shock

I have been writing about the fundamental problem for nearly two decades. Here’s a synopsis from September 2019.

Please consider Nixon Shock, the Reserve Currency Curse, and a Pending Currency Crisis

In 1971 President Nixon appointed the then Democrat John Connally as Treasury Secretary. That’s when things started rolling.

Our Currency But Your Problem

Shortly after taking the Treasury post, Connally famously told a group of European finance ministers worried about the export of American inflation that the dollar “is our currency, but your problem.”

By 1971, US money supply had increased by 10%. In May 1971, West Germany left the Bretton Woods system, unwilling to revalue the Deutsche Mark. Switzerland also started redeeming dollars for gold.

On August 5, 1971, the United States Congress released a report recommending devaluation of the dollar to protect the dollar against “foreign price-gougers“.

On August 9, 1971, as the dollar dropped in value against European currencies, Switzerland left the Bretton Woods system.

On August 15, 1971 Nixon directed Connally to suspend, with certain exceptions, the convertibility of the dollar into gold or other reserve assets, ordering the gold window to be closed such that foreign governments could no longer exchange their dollars for gold. He also issued Executive Order 11615, imposing a 90-day freeze on wages and prices in order to counter inflation. This was the first time the U.S. government had enacted wage and price controls since World War II.

The American public believed the government was rescuing them from price gougers and from a foreign-caused exchange crisis. Politically, Nixon’s actions were a great success. The Dow rose 33 points the next day, its biggest daily gain ever at that point, and the New York Times editorial read, “We unhesitatingly applaud the boldness with which the President has moved.”

So Much for Temporary

The move was not temporary. There have not been any restraints on deficit spending since.

Wars became easy to finance. Deficits? No problem.

In 2011, Paul Volcker, who replaced William Miller as Fed Chair in 1979, expressed regret over the abandonment of Bretton Woods.

“Nobody’s in charge,” said Paul Volcker.

Nobody’s In Charge

Indeed!

There are zero controls on increasing deficits, massive government spending, housing bubbles, or stock market bubbles.

Inflation does not count any of the bubbles.

Credit exploded, deficits exploded, and so did trade imbalances.

We are headed for a currency crisis, timing uncertain, the same thing I have been saying for a long time.

Death of Dollar Silliness

Consider my October 25, 2017 take called Gold-Backed Petro-Yuan Silliness.

A massive amount of hype is spreading regarding China’s alleged ambitions to dethrone the dollar. The story this time involves China’s plan is to price oil in yuan using a gold-backed futures contract. Even if that were true, the impact would be zero. CNBC is now in on the hype: China has grand ambitions to dethrone the dollar. It may make a powerful move this year.

Repeat after me: It’s meaningless what currency oil is quoted in. Once you understand the inherent truth in that statement, you immediately laugh at headlines like that presented on CNBC.

Nothing has fundamentally changed regarding the yuan replacing the dollar as a major reserve currency.

Forget the Yuan

In 2018, I commented Forget the Yuan: King Dollar is Here to Stay

It’s important to understand that we are talking about the dollar’s role in trade, not the value of the dollar itself.

I have discussed the role of the yuan and petrodollar myth multiple times as well.

For my latest take, please see What Does CFR’s Brad Setser Say About Petrodollar Myth and Reality?

Setser: There is enough real data for me to refute the modern financial fairy tale that there is a big float of petrodollars sustains the dollar system.* This is fun to believe, but not really based in reality.

Manufacturing Percent of US Jobs

Related Posts

September 26, 2019: Trump’s Unwinnable Trade War: Gold Explains Why

One of my readers proposed that problems US balance of trade issues started with NAFTA. Wrong!

July 6, 2026: Trump’s Tariffs Did Not Bring Back Manufacturing Jobs. What Will?

On average, tariffs are a jobs killer. They protect one industry while costing others.

Tariffs won’t fix the problem, petrodollars never matters, and the yuan is not about to replace the dollar as the world’s reserve currency.

I have been on the right side of yuan, petrodollar, tariff, and gold debate since 2006.

You know this as well as anybody Mish. The trade deficit is exactly the twin of the budget deficit. As the budget deficit gets worse so will the trade deficit. By definition.

Not exactly twins but definitely related

This is far worse than expected. Why? Because the US has been exporting huge amounts of refined products, LNG, fertilizers, helium and crude oil at high prices for several months.

Farmers in particular should be freaking out because for the fourth time, sales of soybeans announced by Trump have failed to materialize in actual shipments.

The only country in the world that both needs food in large quantities and can afford to pay market prices for it is China. All the rest? The US taxpayer has to pay for it and then the United States did the work of Jesus and fed the hungry of the world our AG surplus for free. It worked. From JFK to 2025. Trump has managed to totally fuck up both.

No surprise as taconomics is totally consistent on the downside except for the top 10-20%.

There are very good, honest videos that bring home what it would take to bring US manufacturing back…a lot.

For example, Dan Collins: Tariffs and the Future of US Manufacturing:

https://www.youtube.com/watch?v=7ngccqS9ydA

That is if there is political will, such as one characteristic of China…

And the US and Iran and trading blows again.

The art of the deal.

Pretty much everything in this blog boils down to “no shit.” The United States is an advanced capitalistic economy; meaning that our economy will continue to reinvent itself based upon a highest and best use based upon a combination of workforce supply, available innovative productivity investment, and the flow of available capital. All of these factors put together dictate where the highest return on invested capital goes. Where that capital goes, goes the economy. No President or business leader will change the course our economy takes in the end short of ending our version of free market capitalism all together.

We do not have “free market capitalism”. We have crony capitalism. Profits are siphoned off to insiders, losses and development costs are socialized.

Path of least resistance politically, for both parties. Interested groups play for concentrated benefits, dispersing the costs into the future and across the populace. I have certainly benefited from parts of this. So I’ve been at the table, but I’m not sure when I may find myself on the menu.

Speaking of fiscal discipline (or lack thereof), did I hear that Hegsdeath is calling for a $2T “defense” budget? If that so Trump’s outrageous $1.5 T request looks less outrageous?

We’ll need it, to conquer the new NATO enemy. Bibi’s got our backs.

That’s the age-old strategy, ask for $1.5 trillion which is a big increase, raise the request to $2 trillion, then settle for $1.5 trillion then the politicians can tell their constituents that they cut the defense budget by $500 billion, a big fat lie that news outlets never challenge.

More losing from our loser president. More to come.

He has nothing to lose, unlike we the people.

I suspect the timing will be 2032 unless the clown gets impeached or dies.

“Everything Trump touches goes to shit”

Expect fun things after 2028. If the Democrats win, they inherit a barn fire and will be blamed for four years by the Republicans for everything Trump turned to shit. If the Republicans win they also inherit a barn fire and will blame Obama.

Either way, the Republicans will win 2032

By that time the course will become inevitable. Before 2032 there won’t be enough effort to do anything about it.

But I really think it’s much sooner.

The E-$ did more damage than Nixon. It was the change in the trading desk’s operating procedure, from 24 months to 24 hours, and the monetization of time deposits, that caused the Great Inflation.

Money grew at less than a 2 percent rate in the decade ending in 1964. In the nine subsequent years money supply grew at a rate in excess of 6.5 percent…

The problems stemed from using the wrong criteria (interest rates, rather than member bank legal reserves) in formulating & executing monetary policy. Net changes in Reserve Bank credit (since the Accord) were determined by the policy actions of the Federal Reserve. But William McChesney Martin, Jr. changed from using a “net free” or “net borrowed” reserve approach to the Federal Funds “Bracket Racket” c. 1965. Note: the Continental Illinois bank bailout provides a spectacular example of this practice.

The effect of tying open market policy to a fed funds bracket was to supply additional (& excessive) legal reserves to the banking system when loan demand increased. Since the member banks had no excess reserves of significance, the banks had to acquire additional reserves to support the expansion of deposits, resulting from their loan expansion.

If they used the Fed Funds bracket (which was typical), the rate was bid up & the Fed responded by putting though buy orders, reserves were increased, & soon a multiple volume of money was created on the basis of any given increase in legal reserves. This combined with the rapidly increasing transaction velocity of demand deposits resulted in a further upward pressure on prices. This is the process by which the Fed financed the rampant real-estate speculation that characterized the 70’s, et. al.

All that technical fiddling about is what econometrists seem to like to talk about. What we need is sound money, i.e. a system in which all the instruments are convertible into gold at the option of the holder. A paper note should be regarded as something that entitles you to demand money, not as money itself. The educators have been confusing the issue (apparently at the behest of the central bank) for quite a few generations now.

Sure, just like in 1893. Just like in 1907, 1929. Along the way,it took JP Morgan to privately put together a couple of consortiums to rescue the collapsing system, including a gold-based one in the 1890s. I suppose Elon or Trump’s other pal CZ would take on the burden.

I don’t know a lot about 1893. I did know about J.P. Morgan rescuing the system in 1907. In the absence of government interference, the market would eventually have developed mechanisms to ameliorate the huge swings that had developed in the 19th century as modern industry was developing. Governments can be relied on to stuff things up.

You can hardly deny that the crisis of 1929 was the result of the activities of the Fed, specifically in over-egging the money supply during the 1920s. I do understand that this was done in order to avoid the normal dislocations that would have followed the end of World War One. Government stupidity drags in everyone. Private stupidity can do a lot of harm if it is general, as in the “Madness of Crowds.” I don’t think anyone has worked out what to do about that yet.

See Alan Greenspan: “Can the U.S. Return to a Gold Standard” WSJ, Sept. 1, 1981.

All the pressure was on the top of the bracket during the Great Inflation.

Banks don’t lend deposits. The 5 successive rate hikes in Reg. Q ceilings for the commercial bankers exclusively made inflation inevitable. An increase in bank CDs adds nothing to gdp.

The math is obvious. China plays chess; Trump plays checkers.

He’s can’t play checkers. He’s too dumb to read the directions

Chicken checkers… he shits on the board and struts around like he won.

The Orange Shitgibbon said that we’d be winning so much, we’d be tired of winning.

If this is “winning”, the question is whether we can survive any more of this kind of “winning”.

The WE he spoke of was the uber wealthy, and they’ve got all kinds of stuff that used to belong to the WE the dipshits thought he meant.