The flippers are back and the competition fierce as there are fewer and fewer foreclosed properties to bid on. Haven’t we been down this road before?

As the competition heats up, Lending to House Flippers Hits a 13-Year High.

- It is getting much harder to profit on house flipping today. Home prices are high, there are very few distressed or foreclosed properties available to buy cheaply, and the competition among investors is fierce.

- The good news is, mortgage rates are historically low for bank lending, and private lenders are eager to invest their cash somewhere other than the volatile stock and bond markets.

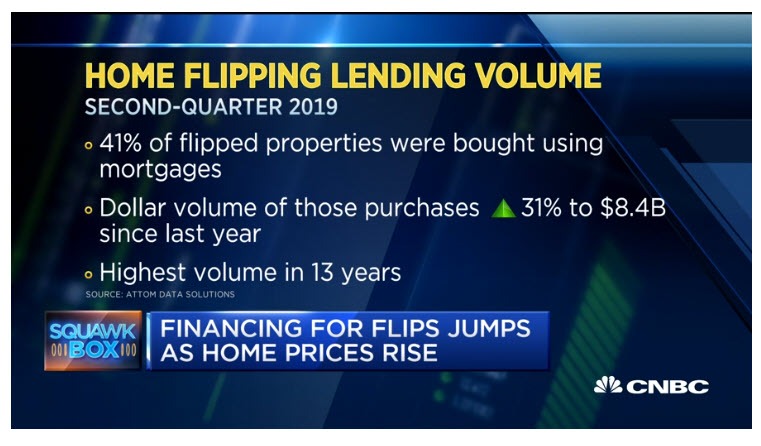

- The dollar volume of financed flip purchases in the second quarter of this year jumped 31% annually, from $6.4 billion to $8.4 billion, according to ATTOM Data Solutions.That is the highest level since the third quarter of 2006.

Smart to Use Leverage!?

Vipin Motwani an investor with Iron Gate Development in the Washington, D.C. area expects to flip about 15 homes this year.

“It’s always smarter to use a mortgage because you get leverage, you can do many more deals, right?” said Motwani. “Also the banks have become a little bit more easy in lending on this flip business. It used to be a lot tougher.”

Housing Bubble Reblown

The Fed has re-blown the housing bubble.

The Last Chance for a Good Price Was 7 Years Ago

Yet, it’s “always smarter to use leverage to get more deals.”

“Right?”

What can possibly go wrong?

Mike “Mish” Shedlock

My neighbors got into the house flipping business. They fixed up a local town house. Broke their backs for months and made no profit. They said it was a learning experience. Tried it again. Ended up selling the next house half done to another flipper. Not sure if they made money, but they decided to get out of the house flipping business.

The TV shows make it look so easy. Their costs are absurdly unreal. Unless they pay the laborers $2/hr and stole some of the materials, there’s no way they got a new kitchen and bathrooms with granite tops for $15k. And buyers willing to pay over their asking price on listing day. Lowes and HD get their advertising dollars worth on those shows.

My mother was a house flipper when I was growing up. She made a lot of money. Not because her renovations were a success. Every time she tried to improve the homes, the local denizens would steal everything. Rather she made money because real estate prices went way up. She bought homes gutted after MLK was shot, held them for a decade and sold them for 10x what she paid.

Buy and hold rental investments will always be the safest strategy this applies to things outside of real estate as well.

Imagine buying a mutual fund or other investment with a 9-10% purchasing charge, plus 1.1% (110bp) annual management fee.

Realtors charge 4-5% commission. Stamp tax / title transfer fee adds another 5%…. so that is a 9-10% purchase charge.

Annual property taxes run 110bp each and every year, double what a typical “actively managed fund” charges.

When housing prices were bubbling, people might not have noticed. When fixer uppers cost well into six figures, 9% upfront plus 110bp per year is a huge performance drag to overcome

…and you have to pay maintenance and utilities on top of that, which negates the “rent” part of living in a house

Another example of lenders seeking yield.

House flipping is a legitimate business, as long as you are taking a property in poor shape, making improvements, then selling for a higher price. I don’t think people have resorted to buying brand new condos again, doing nothing, and hoping to sell for a higher price in a couple months.

Legitimate but often immoral. The improvements made are often cosmetic and the unsuspecting homeowner will find some VERY nasty surprises later on. It sucks to have to rip out some nice “skin deep” work because it actually needed to be “very deep” work to get the problem solved correctly. Flipping in general also is something that really only works in an ascending market, barring the ability of someone to score very large discounts….and those “good ol” days appear to be over. The person or institution selling their junk house in 2019 knows what the flipper intends to do with it, and prices said junk accordingly these days, leaving very little room for profit.

With the Fed pushing $ into the system, things like this will occur.

Also, the policies are punishing savings and making it impossible to find returns. Buy a CD and get 2% and then have 30% taken in taxes. You’ll never get ahead doing that, so why bother?

Just wait for MMT. It can still get crazier!

I’ve completely analyzed this and have determined that nothing could possibly go wrong with this. Continue flipping. Until the music stops.

Agree with Mish about how this movie ended the last time…

The difference between 2008 and now is property taxes. A lot MORE municipalities have become dependent on stamp taxes (the tax on transferring property title, they have different names in different states) and on increases in annual property taxes.

I doubt the tax windfall of house flipping will last as long as the perennial spending initiatives that it currently funds.

When 2008 happens again to house flippers, I wonder how many municipalities will be exposed as insolvent?