The New Residential Construction report for June isn’t all bad news, just mostly bad news. Permits lead the downside.

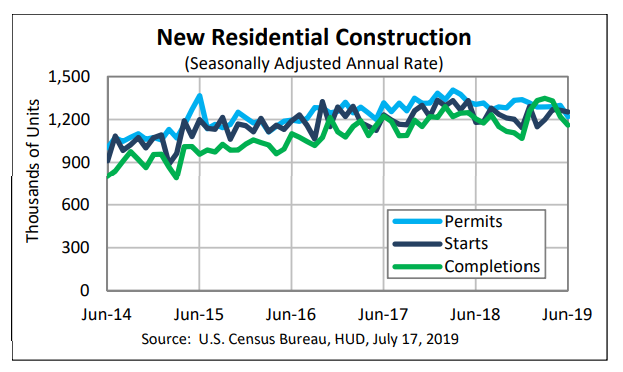

Building Permits

Privately‐owned housing units authorized by building permits in June were at a seasonally adjusted annual rate of 1,220,000. This is 6.1 percent below the revised May rate of 1,299,000 and is 6.6 percent below the June 2018 rate of 1,306,000. Single‐family authorizations in June were at a rate of 813,000; this is 0.4 percent above the revised May figure of 810,000. Authorizations of units in buildings with five units or more were at a rate of 360,000 in June.

Housing Starts

Privately‐owned housing starts in June were at a seasonally adjusted annual rate of 1,253,000. This is 0.9 percent below the revised May estimate of 1,265,000, but is 6.2 percent above the June 2018 rate of 1,180,000. Single‐family housing starts in June were at a rate of 847,000; this is 3.5 percent above the revised May figure of 818,000. The June rate for units in buildings with five units or more was 396,000.

Housing Completions

Privately‐owned housing completions in June were at a seasonally adjusted annual rate of 1,161,000. This is 4.8 percent below the revised May estimate of 1,220,000 and is 3.7 percent below the June 2018 rate of 1,205,000. Single‐family housing completions in June were at a rate of 870,000; this is 1.8 percent below the revised May rate of 886,000. The June rate for units in buildings with five units or more was 283,000.

Bond Yields

Bond yield declined across the board on the news.

- The 10-year yield fell 4.7 basis points to 2.073%.

- The 30-Year yield fell 4.3 basis points to 2.589%

- The 5-year yield fell 4.4 basis points to 1.840%

- The 3-month yield fell 2.5 basis points to 2.134%

Not All Bad

The housing report wasn’t entirely awful.

Single-family permits rose a fraction. Single-family starts rose 3.5% but from negative revisions.

Details, however, are not very encouraging.

Single Family Starts and Permits

Single-family starts are down 4.7% compared to a year ago.

Historically, single-family starts and permits are dismal.

Housing Slowly Rolling Over

The housing sector is slowly rolling over.

Despite lower interest rates, homes are not affordable and attitudes towards the ownership society have changed.

Mike “Mish” Shedlock

Looks like today we are at around the late-2006 to early-2007 point. The cascade, while surely not as overwhelming as last time, could happen faster this time as a lot of people will recall that they have seen this movie before and will want to skip right to the end. I live in LA and meet a lot of new people all the time. Nobody has any money in LA except those higher up in the entertainment industry or those whose income is in some way related to Real Estate appreciation. I don’t hear them being so vociferous these days.

Ever wanted to be able to tell the future? Just master the past. We knew for years that there was going to be a housing bubble, just as we knew there would be an echo bubble/boomlet/2nd bubble. Being smart is not so hard. 🙂

Its easy to predict something bad will happen. Its much harder to predict when

Looks like housing bubble 2.0 is rolling over

People are starting to figure out that ‘homeownership’ now means ‘bankownsyouership’.

Is that better or worse than ‘landlordownsyouership”?

The landlord can kick you out for not making rent, but the bank can take your down payment and equity if you don’t make payments. Either way you pay all your life, but if you rent you have cash instead of equity.

The people for whom ‘homeownership’ now means ‘bankownsyouership’ are the ones who can’t resist the temptation to continually borrow the equity from their home. That will always end with disaster.

I think we agree that having your home repossessed is worse than being evicted, but the vast majority of people have neither. For those people who don’t continually borrow the equity of their home, paying monthly for 30 years, with no increases, and then paying only maintenance and taxes (and having something they can sell) is still far better than paying for 30 years with rent rising every year.

If you move often, definitely rent. If you are at risk of not making payments, definitely rent. If you can’t resist the risk to continue to borrow the equity in your home, again, rent. If you don’t move more often then every 10 years or so, and you are thrifty and responsible, I’d still recommend buying.

Your last paragraph is the main problem for many people. As employment becomes less certain and life events necessitate moving (anything from job relocation to divorce to being fed up with where you are in general) ownership can be problematic.

Oh, and of course the Fed has strongly discouraged thrift with artificially low interest rates.

I think it’s the first paragraph that’s the problem. I think a huge number of people can’t resist borrowing the equity in their home to spend. They indeed do become debt slaves, with no hope of ever being debt free.