Comparisons Gone Haywire

Seasonally adjusted annualized (SAAR), New Home Surged to a 13-Year High With the Midwest Leading the Way.

By Region Month-Over Month Percentages

- US: +13.9%

- Northeast: -23.1%

- Midwest: +58.8%

- South: +13.0%

- West: +7.8%

By Region Year-Over Year Percentages

- US: +36.3%

- Northeast: +25.0%

- Midwest: +81.4%

- South: +27.6%

- West: +40.8%

Covid-Skewed Numbers

Due to Covid-19, 2020 is not a normal year.

Strange things happen when you make seasonal adjustments and even year-over-year unadjusted comparisons in such setups.

Unadjusted Numbers

On an unadjusted basis there were 78,000 newly homes sold during July vs 75,000 in June.

Those 78,000 new home sales in July alone were reported as 901,000.

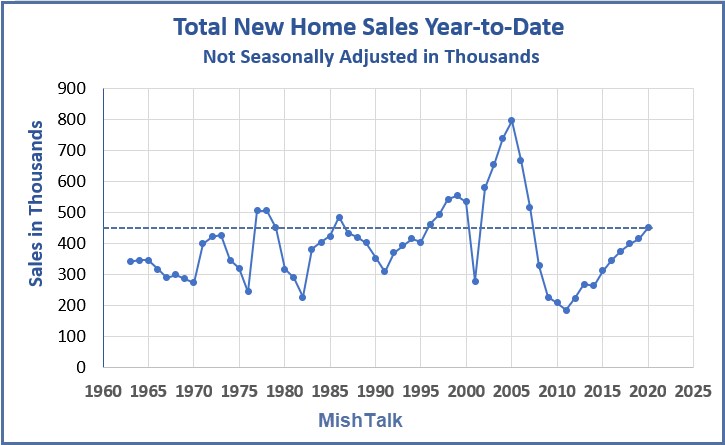

However, the year-to-date total for seven months is only 450,000.

What’s the Valid Comparison?

I downloaded the unadjusted new home sales data from Fred (the St. Louis Fed data repository) and totaled up the year-to-date numbers since 1963.

Year-to-date, there were 450,000 new homes sold. Last year, there were 415,000 homes sold through July.

The year-over-year gain is a more realistic 35,000 / 415,000 = 8.4% not 36.3%.

For those with money and a job, Covid helped. The Fed slashed interest rates and mortgage rates followed.

But problems brew beneath the surface.

Mortgage Lenders Ask New Question: Do You Intend to Pay?

Serious defaults are at a decade high and lenders are now have new forms.

For discussion, please see Mortgage Lenders Ask New Question: Do You Intend to Pay?

Mish

George Orwell’s vision of newspeak has come to pass. Everything now are lies and distortions.

“On an unadjusted basis there were 78,000 newly homes sold during July vs 75,000 in June.”

…

There is also something subtle to consider. The report covers 4 sections of the country. Sales are quoted “in the thousands”. If raw number ends in 499 or less … it is rounded DOWN to whole thousands. Conversely, a raw number ending in 501 or greater … it rounded UP to whole thousands.

It’s all about playing the game, by their rules. You have to do that or you will never be successful (unless you break the law but that’s another tale). What are the “rules”? They are not far off from the Life board game, and it’s a heavy burden for young folks. But around the age of 18 you are responsible for picking a field to be educated in that’s in demand (“get a good job”) or having what it takes to be a successful entrepreneur. After the learning curve that is your 20’s, you should be fiscally responsible in your 30’s and 40’s and have fruitful investments (stocks, bonds, real estate). When you’re in this “club”, there are far more options provided by the Gov to bail you out, than their are if you’re a burger flipper and your only options are welfare related. And if you persevere and remain in this club, you’ll have more enjoyment in your later years.

These days, you will probably need to re-educate yourself at some point in your career, to keep yourself in demand. Or leave to a smaller pond to be a bigger fish.

And at the end of the day, I don’t know what happened in America but they seemed to have had it figured out back in the 80’s. Journey said “some will win, some will lose” and John Cougar Mellencamp said “There’s winners, and there’s losers”. It sucks but you may bust your hump for 20 or 30 years, only to have your job field, city, or health collapse and suddenly it’s game over. But it’s certainly a far better alternative than living in most countries in this world.

America has issues as any country does, but you better bet your butt that I won’t trade the ability to hit a freeway and drive across the country, and see all the beautiful sights, for anything else in this world.

Home sales are overstated just like everything else in America.

… where all The Children are above average…

That’s Lake Woebegone, a very small slice of America.

I think there will be a big change in the real estate market this year, a year full of volatility due to the great influence from Covid 19. https://ps5releasedate.com

As an investment property owner in suburban minneapolis, I’m holding out.

Supply is very low and lack of building materials isn’t ending soon.

I wouldn’t expect residential real estate to be static price-wise in an environment when stock indexes are making new highs every week. So it might be inflation expectations…in addition to low rates, that are supporting housing right

now.

But if the equity market bubble pops, housing will probably tank….as will metals and most other assets. (jmho.) I still like owning houses…..it’s just a matter of how much leverage is acceptable….right now the less the better, in my view.

But within reasonable limits, it seems like a good time to buy and hold tangible assets. If it is possible to light up the fires of inflation, is there anything more likely to ever do it than pumping $6T into the economy in less that 6 months?

I have read you for many years Mish, and always favored your general POV. Do you think runaway inflation is even possible these days? I wonder.

Good grief! Runaway inflation? Do you actually read Mish’s blog?!

I know, I know. LOL.

I’ve been calling for a deflationary event for years myself……but that was before the $6T.

Deflation on tap.

The $7 trillion balance sheet means nothing re inflation (outside of expectations). $$s are “birthed” thru the banking system with fractional lending. Most of QE just piles up as excess reserves.

I would argue that the current bailouts (from the Treasury and the SBA) have pushed consumption forward to some degree…which seems to have been the real intention, regardless of any other stated narrative.

Obviously the amounts involved are small in relation to the Fed balance sheet, ( and I get that banks loan money into existence) but 20 billion injected in EIDL loans and 310 billion in PPP money seems fundamentally different to me than the kind of QE we’ve had for the past 12 years.

I personally got an injection of nearly 250K into my business…and although I will have to pay most of that back…and it was helpful at a time when my practice was hurting…..and I’m glad I could get the funds…..it temporarily has made my balance sheet cash rich….

And your point about expectations is well considered. An expectation of inflation tends to create inflation.

I don’t fail to comprehend that there are extraordinary economic forces that point to massive deflation over the coming years….but that’s after all the asset bubbles pop, right?

I know Mish defined inflation in terms of credit expansion…which makes good sense…he’s been right for a long time. But my guess that right now certain tells like the spike in gold and silver prices…..that is not likely to be people buying gold to hedge for DEFLATION…so maybe expectations have fundamentally changed.

I appreciate the responses to my question….all views are of interest to me on this…I’m not saying I have it figured out. I’m just curious.

The Massive Debt Overhang … hangs over everything.

All levels of government / household / business at record level of debt. It needs to be serviced (at the expense of current / forward consumption). Growth was achievable – despite debt levels – by the downtrend in interest rates the past 40 years. Lower rates allowed rollover / refi which freed up $$s for consumption. At the zero bound that game about over.

Until debt dealt with via pay down / write down / write off there will be sustainable inflation.

I’m not sure of their thinking that attempts to solve the problem of too much debt … with more debt??

Once current inflationary impulse of fiscal stimulus + forbearance / moratorium wanes … inflation downtrend will continue.

You could spend years studying money, currency, banking, credit, finance, debt, inflation and their broad history spanning millennia, and still come away confused where we are heading and how fast, because you then need to focus on understanding today’s very opaque global Eurodollar banking system, which actually creates the global reserve currency that is somewhat connected to the US dollar. To understand where the US dollar is heading, you have to try to understand where the Eurodollar is heading, and the Eurodollar is not controlled by the Federal Reserve, it is controlled by private multi-national banks. Therefore, you will not find a historically similar inflation/deflation scenario to extrapolate from, because today’s Eurodollar system only began to become the driving engine of international reserve currencies starting in the 1970s. As a result, you cannot estimate future inflation/deflation in the United States in isolation of what is occurring in the rest of the world. But, in the meantime, you can probably rest assured that the US dollar will remain on relatively strong footing, because it is the seed currency of the Eurodollar system, and that system is going nowhere, because nothing currently exists to replace it. Good luck on your studies.

Yes, you have noticed a very counter-intuitive concept at work — money is now debt, created by banks, loaned into existence, and it’s now global, and largely unregulated by any one central bank. A good bet is that’s unstable and prone to wild inflationary-deflationary rides, depending on your definition of inflation and deflation, whether that be CPI, asset markets, real estate, wages, etc. , and the time period you are looking at. It is all quite exciting to watch and bet on.

Is it ever honest to participate in a rigged game?

2020’s Best Real-Estate Markets https://wallethub.com/edu/best-real-estate-markets/14889/

A report from Realtor.com. “The nation’s surging home prices don’t seem to care about the recession the country is mired in. It has all led some to wonder: Are some markets getting too hot? Could we be entering the dreaded bubble territory once again? ‘Some markets are overvalued,’ says Javier Vivas, realtor.com’s director of economic research. ‘Growth of prices in a recession is pointing in that direction. Some markets are seeing increased risks of price corrections.’” https://www.realtor.com/news/trends/home-prices-shooting-up-is-housing-market-overheating/