Markit PMI in Strong Contraction

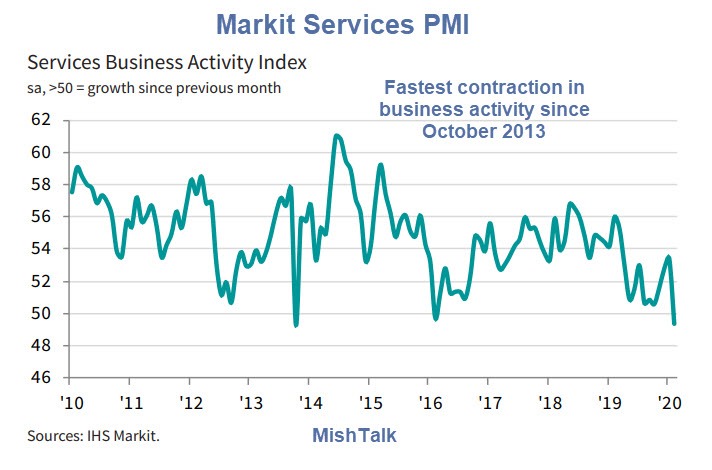

The IHS Markit U.S. Services PMI™ shows the fastest contraction in business activity since October 2013.

February data signalled the first contraction of U.S. service sector business activity for four years. The decrease in output stemmed from only a fractional rise in client demand and a further contraction in new business from abroad as customers held back from placing orders amid global economic uncertainty and the coronavirus outbreak. As a result, business confidence remained historically subdued and employment growth slipped to the weakest since last November.

Private sector output was weighed on by a contraction in business activity at service providers and a slower manufacturing expansion.

The IHS Markit Composite PMI Output Index registered 49.6 in February, notably down from 53.3 posted at the start of the year. The decrease in overall output was the first for over six years.

Composite PMI vs GDP

Chris Williamson, Chief Business Economist, Comments

- “The US service sector took a knock from the coronavirus outbreak and growing uncertainty about the economic and political outlooks in February. The fall in the headline index measuring business activity levels was the second largest seen since the global financial crisis over a decade ago, exceeded only by the brief slump in activity during the 2013 government shutdown.”

- “Combined with a weak manufacturing survey in February, the data are consistent with annualised GDP growth slipping from around 2% at the start of the year to just 0.7% midway through the first quarter.”

- “Business sectors such as travel and tourism are reporting weakened activity due to the virus outbreak, most notably in terms of foreign visitors and overseas sales. However, other sectors such as financial services and business services are reporting virus-related hits to demand, suggesting a more broad-based weakening of demand across the economy, exacerbating the supply-shock that is constraining manufacturing.”

- “Companies have meanwhile grown increasingly concerned about client spending and investment being curbed ahead of the presidential election. Political and economic uncertainty, the coronavirus outbreak and financial market turmoil all risk building into a cocktail of risk aversion that has severely heightened downside risks to the economy in coming months. Much will depend of course on the speed with which the virus can be contained and how quickly business can return to normal.”

ISM Non-Manufacturing Index

The February 2020 Non-Manufacturing ISM® Report On Business® not only show business expansion but growth in production, new orders, employment, deliveries, prices, backlog of orders, new export orders, and imports.

Word About Diffusion Indexes

I have discussed this before but it’s worth repeating.

Both the Markit PMI and ISM NMI are diffusion indexes. They both measure, or claim to, service sector and manufacturing sector output.

Diffusion indexes do not measure magnitude, only direction. For example, one company hiring a single worker will offset another company firing 300 because one is positive, the other negative.

ISM vs Markit

ISM concludes first-quarter GDP is growing at 3.0% vs 0.7% for Markit.

Setting GDP aside, the component numbers of ISM are not remotely believable.

On February 18 (for January), I commented on the Largest Shipping Decline Since 2009 and That’s Before Coronavirus.

Europe is a basket case. China is even worse, in lockdown mode.

Yet, ISM says new export orders are expanding much faster.

That these surveys are so wildly different with ISM numbers truly unbelievable suggests the ISM sample is either too small or is not remotely representative of the industries it measures, or both.

Mike “Mish” Shedlock

Perhaps export orders are increasing to replace goods that are no longer available from China. Purchasing departments know how to scramble. Their company’s production depends on them finding materials and getting them on time. These numbers don’t seem odd.

Once corona hits here, things will be different.

“Which One is Wrong?”

If you throw two dice and they don’t come up the same; expending effort to try deciphering which one of them is “wrong”; is unlikely to be the most productive use of scarce time and resources…..

Cute but it implies that you think a crash in global transportation is a roll of the dice.

Think about that crash and other known things, then report back.

Are those two reported numbers simply two different guys attempting to count the exact number of packages arriving on US shores?

If so, them differing means one, or both I suppose, is “wrong.” Otherwise, them differing just means they are different.

Supposedly they are measuring the same thing.

I asked Markit about this once. If I recall correctly, they said their sample size is much larger. I did not post that today because I might not remember accurately but I am about 90% confident that was the conversation.

Curiously, the Fed and the Fed models (GDPNow) both rely on ISM, not on Markit.

The ISM data may be distorted by “seasonal adjustments”.

Weather.

NOAA hasn’t come out with February’s numbers yet, but here in Mid Atlantic another mild month. Outside of a 3″ snowstorm in January, there has been NO snow. Area schools have closed only 1 day. Very unusual.

We get snowless winters every once in a while. Certainly not normal, but not unusual either.

A bit further south, we’re below average for the last month and a half

And it snowed in Baghdad recently. Definitely nothing unusual. /s