Black Knight reports forbearances rise following three weeks of declines.

Key Details

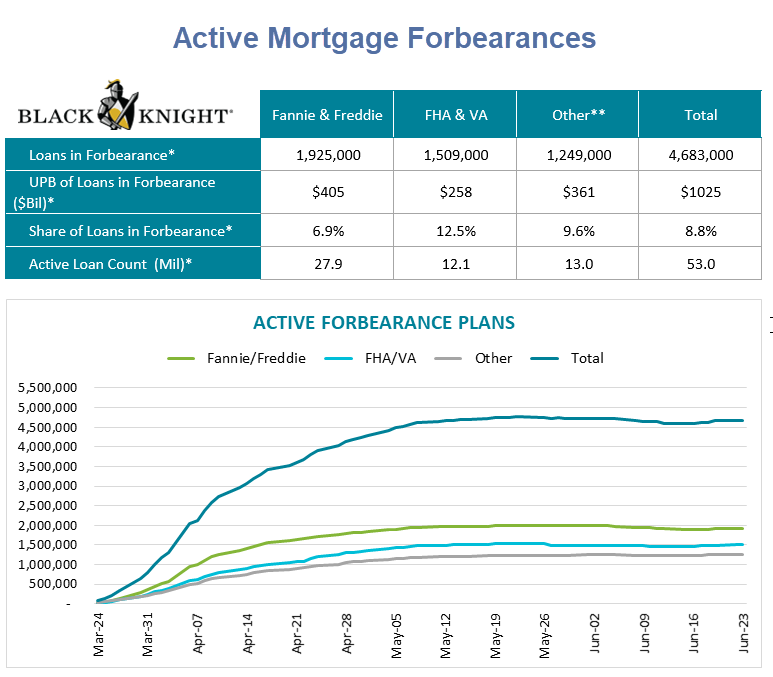

- Overall, the number of active forbearance plans is up 79K from last week – erasing roughly half of the improvement seen since the peak of May 22 – with rises seen over each of the past five business days.

- As of June 23, 4.68 million homeowners are in forbearance plans, representing 8.8% of all active mortgages, up from 8.7% last week. Together, they represent just over $1 trillion in unpaid principal ($1,025B).

- Some 6.9% of all GSE-backed loans and 12.5% of all FHA/VA loans are currently in forbearance plans. Another 9.6% of loans in private label securities or banks’ portfolios are also in forbearance.

- Volumes were up across the board from the week prior with the largest increase among FHA/VA loans (+42K), with smaller increases seen in GSE (+25k) and non-agency (+12k) loans.

- At today’s level, mortgage servicers may need to advance up to $3.5 billion/month to holders of government-backed mortgage securities on COVID-19-related forbearances. That’s on top of up to $1.4 billion in T&I payments they must make on behalf of borrowers.

No Progress

Since the beginning of May, the number of active mortgage forbearance plans has ranged between 4.5 million and 5 million.

The unpaid balance now tops $1 trillion.

It will become harder and harder to pay that back. I suspect most will eventually roll past due amounts into a new loan. But first, people will have to make a number of on-time full monthly payments.

These loans are not reported to credit agencies as delinquencies, but it is not possible to refinance loans in forbearance until a number of current payments are made.

Disastrous Unemployment Claims

The jobs picture is not making thing any easier.

Initial claims rose by 1.48 million this week, but continued claims at 19.52 million tell the real story.

20 million people out of work for 8 straight weeks tells the real story.

For details, please see Impossible to Sugarcoat the Disastrous Unemployment Claims

IMF Assessment

Even the perennially late IMF is beginning to catch on.

It’s a Crisis Like No Other: IMF Downgrades US GDP to -8.0%

Mish

celebztrend“=””>https://celebztrend.com/“>celebztrend

viralcelebz“=””>http://viralcelebz.com/“>viralcelebz

celebztrendz“=””>http://elster-eis.com/“>celebztrendz

Zone Diary – Content Worth Gold in Small Categories Zones

Read Trending high-quality content written by different authors, owners of top blogs in popular Categories for Millions of Users.

Best website for space tech and reviews. Check the website

Very useful post. This is my first time i visit here. I found so many interesting stuff in your blog especially its discussion. Really its great article. Keep it up.

“=””>https://petlyhub.com/mary-cosby-net-worth-2/“> PET LOVERS

” target=”_blank” rel=”nofollow”>https://petlyhub.com/mary-cosby-net-worth-2/%22>

Very useful post. This is my first time i visit here. I found so many interesting stuff in your blog especially its discussion. Really its great article. Keep it up.

“=””>https://petlyhub.com/mary-cosby-net-worth-2/“> PET LOVERS

” target=”_blank” rel=”nofollow”>https://petlyhub.com/mary-cosby-net-worth-2/%22>

Best Website to Buy Emergency USB https://www.myemergencyusb.co.uk

Everyone loves what you guys are usually up too. This kind of clever work

and reporting! Keep up the terrific works guys

To focuse”=””>https://focuseuk.com/“>Focuse UK

Focuse” target=”_blank” rel=”nofollow”>https://focuseuk.com/%22>Focuse

Best website for space, tech and reviews.

Hi!

This is very well written and it’s so intresting.

This is so awesome.

But you should also see this…

This site provides free serial/activation codes and license keys.

Really amazing articles“=””>https://amirarticles.com/“>articles to explain the importance of tech“=””>https://amirarticles.com/tech/“>tech in our life.

These new discoveries can help everything in every field, even they are connected to the healthfield.”=””>https://amirarticles.com/health/“>healthfield.

Great job“=””>https://amirarticles.com/real-jobs/“>job by Author. Thanks for sharing

tech” target=”_blank” rel=”nofollow”>https://amirarticles.com/tech/%22>tech

healthfield” target=”_blank” rel=”nofollow”>https://amirarticles.com/health/%22>healthfield

job” target=”_blank” rel=”nofollow”>https://amirarticles.com/real-jobs/%22>job

Well said.

Find in-depth content on the below links.

https//hrhelpboard.com/performance-management/job-analysis.htm

https//hrhelpboard.com/performance-management/performance-management-system.htm

Check My new article.

Nice and impressive.

to know more about anime please check here.

Very Nice and well written.

It was really interesting and helpful.

To explore”=””>https://exploretheideas.com/“>Explore The Ideas

Explore” target=”_blank” rel=”nofollow”>https://exploretheideas.com/%22>Explore

Impressive article.

True https://www.discountsgravity.com/youtube-tv-promo-code

Forbearance is free money, as Kevin explains (https://www.youtube.com/watch?v=VhJEoOqENWQ). The idea is that you have the option of not paying your mortgage for a year and instead pay it at the end of the loan’s duration, which is often decades away. In the meantime, you can invest the money that you saved by not making mortgage payments. It makes financial sense for a very large percentage of the population to request forbearance. For once, a law was passed that financially benefits the little guy. Watcha gonna do? Feel guilty for taking advantage because only Bezos and Blankfein are deserving of bailouts and handouts?

“The idea is that you have the option of not paying your mortgage for a year and instead pay it at the end of the loan’s duration, which is often decades away.”

…

Well, that is nice … if lender agrees to THOSE terms.

Terms I see currently are lump sum as soon as payments restarted … or payback of forbearance in short term (1 to 2 years).

As Kevin says, the lender must agree to those terms because it’s the law. They don’t want you to know the law, and they have no interest in giving you a deal that is more favorable to you, so you have to talk them into it.

studyfinds.org:

NEW YORK — The coronavirus pandemic has been devastating for the United States economy. A new study finds the crisis could soon cause a big shakeup in the real estate market. As homeowners struggle to pay their bills, researchers say many Americans are thinking about putting up the “For Sale” sign.

A survey of 2,000 American homeowners found that 52 percent are constantly concerned about making their mortgage payment on time. Forty-seven percent of the poll say they’re considering selling their home because they can’t afford their mortgage anymore.

Researchers say 35 percent of U.S. homeowners admit they’ve missed a mortgage payment during the pandemic. The same amount of respondents said they worry about losing their home because of the financial situation COVID-19 has put them in.

The poll, commissioned by the National Association of Realtors, also found that eight in 10 homeowners say the COVID-19 pandemic has caused an unexpected financial problem in their lives.

problem is it is weeks late. Nonetheless a good chart – where is it from?

I just put it together in Excel, from the data on page 4 of the weekly DOL bulletin.

“The number of mortgage loans in forbearance plans rose by 79,000 this past week. This was the first jump in three weeks.”

…

Just as Day follows Night

Delinquencies / Defaults ramp when stimulus fades.

When PPP and $600 extra week end look for Delinquencies to leave the launch pad … in a hurry.

“These loans are not reported to credit agencies as delinquencies,”

…

Yes … BUT also one reason why credit tightening now.

Lenders can’t determine which borrower applicants are in forbearance … or not. If you do not know borrower’s credit history completely, scrutiny will be ratcheted up on what you can know.

Most banks also report payments being made to the credit agencies. The lack of payments will get factored into credit scores, although I don’t think the hit will be as large.

As the relative creditworthiness of the homeless improves.

…Black Knight reports another breathtaking increase in mortgage delinquencies in its “first look” at May loan performance data. The rate, which soared by 90 percent in April, grew another 20.4 percent, to 7.76 percent of all active mortgages. This puts the rate, which had been declining continually to near all-time lows before the impact of the COVID-19 pandemic, up by 130.8 points from May 2019. This is the highest delinquency rate since late 2011….

Does anyone know how these numbers compare to the number of mortgage delinquencies during the financial crisis? Also, how does this compare to the number of renters who have fallen behind on their monthly rent? If we are to believe that a large number of US households have no significant emergency funds then falling more than one month behind on mortgage payments and rents will be a disaster for those impacted and a significant drag on the recovery. The latest news about the increase in COVID cases and renewed lockdowns does not bode well.

We specialize in web development services, in which we highlight the corporate responsive sites, portals, blogs, e-commerces/virtual stores, Landing Pages, Newsletter, web systems, among other creative and programming solutions for web.