Wilshire Consulting’s time horizon is 10 years, GMO’s is 7 years, and Hussman’s is 12 years.

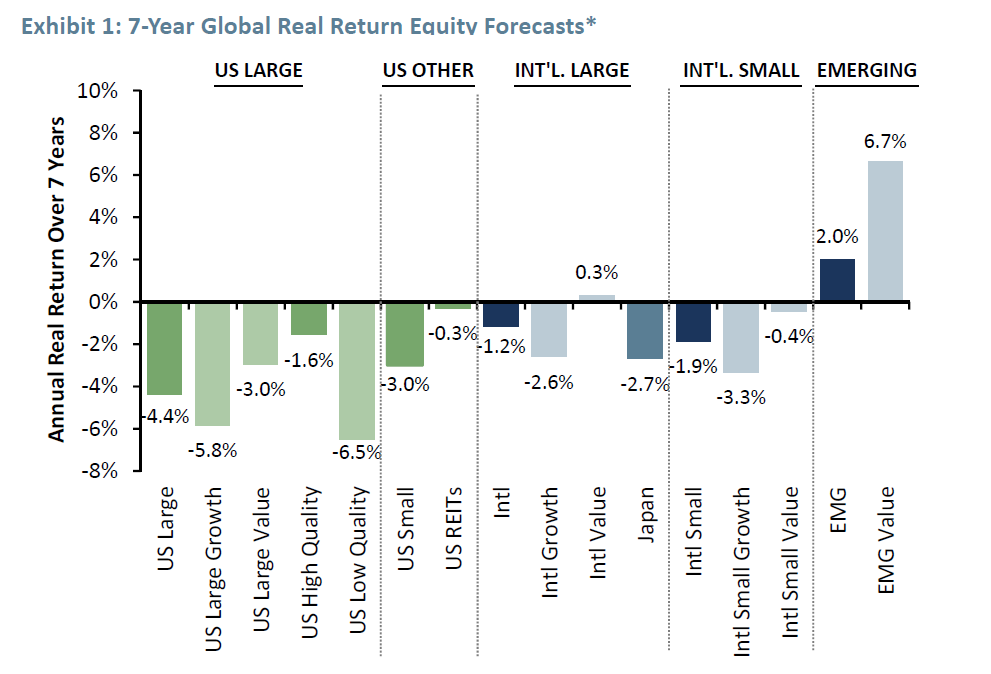

The Feature image is from GMO’s Third-Quarter Report as of 10/31/2017.

The report, which I highly recommend reading states, “*The chart represents local, real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance.”

Pension Funds’ Dilemma

The Wall Street Journal notes a pension dilemma and asks: What to Buy When Nothing Is Cheap?

The largest U.S. public pension fund debated in December whether to sell more than $50 billion in stocks as global markets raced higher. But in the end, the board of the California Public Employees’ Retirement System decided it was fine to hold more.

No matter which move Calpers made, it faced challenges. Scaling back Calpers’ equity investment would have reduced the fund’s projected 7% return at a time when the fund has just 68% of the assets needed to pay for future benefits. That would have meant higher contribution costs for local governments across California.

How much risk to take is a question facing all investors as they enter 2018. “Everything is overvalued,” said Wilshire Consulting President Andrew Junkin, who advises public pension funds. “There’s no magic option out there.”

Over the next decade Wilshire Consulting is predicting a 6.25% compound return for U.S. equities and 3.5% return for core bonds. International equities have a projected compounded return of 6.45%. Most pensions’ return targets remain at 7% to 8%.

Survival Tactics for a Hypervalued Market

Wilshire Consulting is a blazing optimist compared to GMO and Hussman.

In his most recent article, John Hussman discusses Survival Tactics for a Hypervalued Market.

One must distinguish between a boulder resting safely at a permanently high plateau, and a boulder teetering at the edge of a cliff, thanks to temporary and unreliable support. Refrain from imagining that extreme valuations are equivalent to “justified” or “durable” valuations. A century of evidence suggests that something very different is going on.

The summary of our present outlook is this: we view market valuations as obscene, with negative expected S&P 500 total returns over the coming 10-12 year period, and a probable interim loss on the order of -65% over the completion of the current market cycle. Still, in the absence of further deterioration and dispersion in market internals, our immediate market outlook is actually rather neutral. Remember also that a material retreat in valuations, coupled with an early improvement in market internals, is likely to produce favorable investment opportunities far sooner than 10-12 years from now.

Like the 1929 and 2000 market peaks, Wall Street is pushing a great deal of loose analysis intended to “justify” current valuations, imagining that just because prices have reached a certain level, they must actually belong there. Arguments like “valuations are justified given the level of interest rates,” or “given the recent tax cuts,” or “given a growing economy with low inflation” sound reasonable enough, but as we’ve detailed at length in recent months, they don’t hold up to the scrutiny of careful discounted cash flow analysis.

Don’t discount discounted cash flows

A share of stock is ultimately nothing but a claim on a very, very long-term stream of cash flows that will be delivered into the hands of investors over time. Investment, properly defined, is concerned with the price one pays for that very, very long-term stream of future cash flows, and the returns that can be expected as a result of that tradeoff. On this front, the Iron Law is that the higher the price an investor pays for given stream of expected future cash flows, the lower the return the investor can expect over time. Conversely, the lower the price an investor pays for a given stream of expected future cash flows, the higher the return the investor can expect over time.

What we observe at present may be distressing, but we think it’s also accurate. In order for the S&P 500 to be priced for a 10% expected long-term annual return, the Index would presently need to trade at roughly 884; less than one-third of present levels. An 8% expected long-term return would correspond to a level of roughly 1281 on the S&P 500. Indeed, the Index reached this range of prospective returns even by the completion of the most recent market cycle, and the valuation level associated with an 8% expected return exceeds the actual value of the S&P 500 at nearly every point in history except the period surrounding the 1929 peak and the extremes of recent years. The only reason the S&P 500 has posted even 5.2% average annual total returns since the 2000 peak is that the recent extreme has restored the most offensive valuations in U.S. market history. We expect all of that total return to be erased over the completion of this market cycle.

The bottom line is that we fully expect a market retreat on the order of 50-65% over the completion of the current cycle. That’s a different statement than saying that it must occur immediately.

By the completion of this market cycle, there will likely be no talk of the “cost” of getting out too early. The 2000-2002 collapse wiped out the entire total return of the S&P 500 – in excess of T-bill returns – all the way back to May 1996. The 2007-2009 collapse wiped out the entire excess total return of the S&P 500 all the way back to June 1995. We correctly anticipated the extent of both collapses. I can’t emphasize strongly enough how much of our challenges in the recent half-cycle traced to our bearish response to “overvalued, overbought, overbullish” syndromes- which we’ve since subordinated to our measures of market internals, with no exceptions.

Frankly, I expect that the completion of the current cycle will wipe out the entire excess total return of the S&P 500 all the way back to roughly October 1997. That outcome would not even require our most reliable measures of valuation to revisit their historical norms. If you know how our measures of valuation and market action helped us to navigate prior complete market cycles, you know that it would be a mistake to underestimate the full-cycle risks investors currently face, regardless of whether or not those risks are realized immediately.

See No Evil, Hear No Evil

Hussman goes into detailed analysis with numerous charts supporting his position.

Most won’t bother hearing Hussman’s message because it’s pretty much been the same message for several years.

No Escape

People like to believe they will be the ones to “get out on time”. Mathematically it’s impossible for all but a tiny percentage to escape.

For every seller, there is a buyer. Someone has to hold every stock and every bond 100% of the time.

A major repricing event is coming, more likely a series of them over the next 5-7 years.

Pension plans will be devastated.

Mike “Mish” Shedlock

I confess I do not have access to sufficient data. The only principles I would follow are these: No one voluntarily loans money at rates below the visible inflation rate; The Fed claims to be able to set interest rates, and in order to do so must offer loans (money) to borrowers at a rate low enough to maintain that lower interest rate (you cannot “talk down’ interest rates). Controlling interest rates at below the rate of visible inflation requires flooding the market with new money. If there’s another way to do it, I’m all ears.

@Clovisdad If central banks have flooded the markets with liquidity, why are repo fails at highs not seen since 2008? Why have loans been flat for the most part? Why the 2015-2016 junk bond blowup? The stock market, compared to international repo and credit markets, is very tiny. Just because the stock market is ripping to new highs doesn’t mean that the market is flooded with liquidity, it just means the market is flooded with idiots who think there’s gonna be a bigger idiot.

Also, pretty much since the 80’s, the amount of deficits has had ZERO effect on the value of the dollar. Whether or not the fed allows for cheap financing of federal debt doesn’t seem to have any effect whatsoever on the dollar. Yall are forgetting that the USD isn’t just a sovereign currency, it’s also an INTERNATIONAL RESERVE CURRENCY. Currently, the amount of assets priced in USD completely dwarfs the federal deficit (we’re talking quadrillions of dollars). The federal deficit is a drop in the bucket.

Faith and emotions are all that matter here, for the most part. The stock market can always continue to get more hideously overvalued, and people can still pretend that all these USD denominated debts can be paid with a physical money supply 1/10000 the size (at the largest) of all these debts. However, all it takes is people to question that and everything blows up. What the fed does has the same effect as the rain dances of old — absolutely nothing.

I do not believe we can project the form of the adjustment, nor its depth. The crisis would have the capacity to destabilize governments, as well as markets. The current intellectual skill set remains bound by the Keynesian fantasy, which even Keynes acknowledges has no solution at the end of his debt creation.

What we do know is that central banks have flooded their markets with liquidity, and that has inflated all asset prices (and provided billions to the carry trade). We also suspect central banks cannot stop this practice because their treasuries cannot afford to service the massive debts which have been created in a period of rising interest rates. Therefore, it seems we should expect some form of uncontrolled decline in the value of currencies thus distorted.

its pretty certain than when the market turns down it will be global liquidity draining out, so that valuations will be ignored. (don’t try to catch a falling knife) there is no guarantee that having gold denominated in dollars will do any good. The Fed is going to hike rates until something snaps, and when it does, you don’t want to be in this market. Rate hikes are done to sell bonds against a backdrop of falling currency value. Short the dollar will be the global trade. Global interests have no respect for America, “I will get you and your little dog too(Trump)” The first thing is to pump and dump our stock market. Then they destroy our reserve currency, and finally drop our credit rating.They have the means to get inside our markets, our white house, our media. They are going to have a field day, the Russian election meddling was childs play.

Like Bam_Man, I can’t decide whether the stock market is overvalued, or it just accurately reflects a continually devaluing currency. Right now, I’m trying to play it both ways, but it’s a tough road.

The equity and bond markets are both a tinder box waiting for a flame to set it ablaze. Once a squeeze ensues, it will quickly gain momentum. The problem is I have no idea when it will happen or what will trigger it. It may happen tomorrow or in 10 years, but it will happen eventually and the carnage will be catastrophic.

One common fallacy here is that speculative psychology is driving this market. That is not true. Global central banks have printed trillions and in the stock market without borders money moves more easily than bitcoin. Looking at US GDP and figuring out market returns is like assuming that the contribution of China to the American consumer really doesn’t matter. Ignore the truth at your own risk. Some day the money will stop.

Hussman apparently does not see #2 occurring during the upcoming 10-12 year period. I think it is entirely possible, if not likely.

2) It is correctly anticipating a major currency de-valuation that will likely result in a hyper-inflation.

1) It is obscenely over-valued, or

I have said many times over the past few years that the stock market is doing either one of two things:

“Investment, properly defined, is concerned with the price one pays for that very, very long-term stream of future cash flows, and the returns that can be expected as a result of that tradeoff.” Nice idea, in 1955. The banks are now deregulated. Our comparisons should be from 1925, not 1955.

Q: Mish, why do you prefer a 5-7 year reset scenario, rather than a quickie 2-3 year?

A: That’s a good question. It has to do with whether or not zombie corporations continue to get funded. The primary thing Bernanke did in 2009 was revive the corporate bond market. Even viable companies could not get funding. That’s what led to the big woosh. If the corporate bond market goes in the crapper, another big flush is more likely.

By the way, notice the sentences starting on a new line line. To get one, press enter, and your comment will be posted. Then find the three dots at the top right of your comment. Click on them and edit.

Mish

Hussman is pulling out “Harry Dent” like doom predictions! Impressive!

Wilshire says everything’s overvalued but then projects a 6.25 percent annual return. Funny.

Hussman’s ‘Survival Tactics for a Hypervalued Market’ didn’t include a single bit of tactical advice.

Mish, why do you prefer a 5-7 year reset scenario, rather than a quickie 2-3 years?