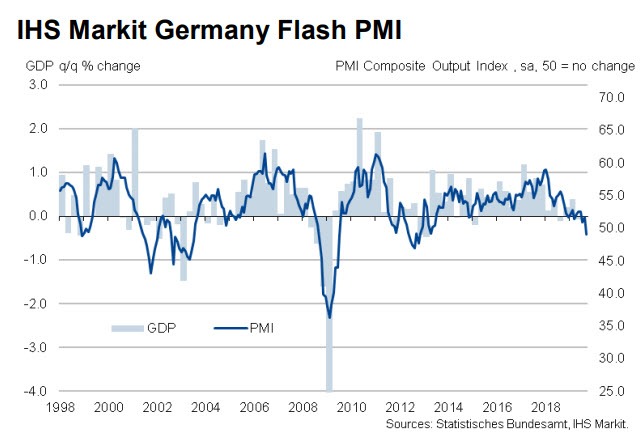

Markit reports German Composite PMI sinks to lowest since October 2012.

Key Findings

▪ Flash Germany PMI Composite Output Index at 49.1 an 83-month low.

▪ Flash Germany Services PMI Activity Index at 52.5 a 9-month low.

▪ Flash Germany Manufacturing PMI at 41.4 a 123-month low.

▪ Flash Germany Manufacturing Output Index at 42 an 86-month low.

Comments from Phil Smith, Markit Principal Economist

- “The manufacturing numbers are simply awful. All the uncertainty around trade wars, the outlook for the car industry and Brexit are paralyzing order books, with September seeing the worst performance from the sector since the depths of the financial crisis in 2009.”

- “With job creation across Germany stalling, the domestic-oriented service sector has lost one of its main pillars of growth. A first fall in services new business for over four-and-a-half years provides evidence that demand across Germany is already starting to deteriorate.”

Eurozone His Stall Point

Markit reports Eurozone Close to Stalling in September as Factory Downturn Deepens.

Key Findings

- Flash Eurozone PMI Composite Output Index at 50.4 a 75-month low.

- Flash Eurozone Services PMI Activity Index at 52.0 an 8-month low.

- Flash Eurozone Manufacturing PMI Output Index at 46.0 an 81-month low.

- Flash Eurozone Manufacturing PMI at 45.6 an 83-month low.

Comments from Chris Williamson, Markit Chief Business Economist

- “The eurozone economy is close to stalling as a deepening manufacturing downturn shows further signs of spreading to the services sector.

- “The survey data indicate that GDP looks set to rise by just 0.1% in the third quarter, with momentum weakening as the quarter closed.

- “The goods-producing sector is going from bad to worse, suffering its steepest downturn since 2012, but a further worrying trend is the broadening-out of the malaise to the service sector, where the rate of growth has now slowed to one of the weakest since 2014.

- “The details of the survey suggest the risks are tilted towards the economy contracting in coming months. Most vividly, new orders for goods and services are already falling at the fastest rate since mid-2013, suggesting firms will increasingly look to reduce output unless demand revives.

- “Furthermore, hiring is being scaled back due to the order book slowdown, with jobs growth now down to the lowest since the start of 2015. A worsening labour market adds to the risk that households could trim their spending.

- “The overall picture of an economy on the cusp of sliding into decline is underscored by a further deterioration in firms’ pricing power, with average prices charged for goods and services barely rising in September.

- “With survey data like these, pressure will grow on the ECB to add to its recent stimulus package.”

Mish Comments

- This is not 2012 or 2104 where stepping on more QE would help.

- The US is not immune to a slowdown in Europe and China, just as China was not immune to a global slowdown in 3007.

Decoupling Theory

Some readers may recall that I correctly rebutted the widespread notion in 2007 that China would decouple from the global economy.

Other readers may note that I failed to recognize that QE in 2012-2014 would help.

They are both correct.

Mish Policy

I have a simple policy: Admit mistakes before someone forcibly admits them for you.

If you are looking for perfection, you won’t find it here, or for that matter anywhere else.

Admissions aside, the notion that a third of the global economy will decouple from two thirds of it is silly.

The US is no more immune from a slowdown in China and the Eurozone today than China was immune from a slowdown in the US and the Eurozone in 2007.

US Will Not Decouple

Decoupling theory is silly. The US will not decouple.

Either the Eurozone and Chinese economies pick up, or the US slides with them.

Place your bets.

Mike “Mish” Shedlock

Everything is down except inflation.

The inflationary depression is here.

Net net, GDP growth will be slightly positive on average but that growth will be really slow and not evenly distributed. Cash businesses will thrive, entities that rely on ever growing debt (including G7 governments) will contract.

The US government will struggle to issue debt to fund its existing promises. It will increasingly resort to all sorts of tricks to keep social security / medicare going in principle but less and less in reality. Means testing against the rich (this is a form of default, even if it sounds politically “just”) on social security started a decade ago and will increase. Medicare will have bigger and bigger co-pays for the middle class (the rich already pay more, this will spread). Medicare will stiff payment on more doctors, and will take even longer to pay what little they do pay. More procedures will be labeled not medically necessary, and will not be covered. More middle class persons will see their social security withheld to pay extra medicare “dues” (this already happens to the rich, it will spread).

Like the later years of WW2, the US government will struggle to issue enough debt to keep the party going. They will find tricks and tactics (see previous paragraph) but it will be a multi-decade struggle. Big new spending programs might be promised, but they won’t actually happen.

The giant G7 debt binge that characterized the baby boomer generation is about to go in reverse, and there is absolutely nothing the politicians can do about it.

Business that is self funding (doesn’t require more and more debt) will thrive.

Even businesses that are cash rich are using debt to buyback stock. At some point the system will collapse under debt.

Debt exhaustion.

We’re close – or at – the point when entities will no longer want to take on more debt. Lowering rates and credit standards has kicked the can (and possibly a bit further). Now / nearing the point where servicing existing debt will preclude taking on new debt.

Just waiting for the delinquencies / defaults to rise sharply … which will cut off the credit tap … recession then unfolds.

The sad point is that end of cycle can kicking (giving credit to anyone who’ll take it) is of the worst quality. Will make upcoming slowdown harsher.

central banks cannot do fiscal stimulus

It is up to Congress in the US

It is up to governments in the EU – but there are rules

The Chinese govt could do so more easily

Mish wrote: “but there are rules The Chinese govt could do so more easily”

I think the most important news article of last week was the op-ed Minxin Pei wrote, the beginning of the end of China’s one party rule ( title paraphased).

Mish referenced it indirectly in a tweet from Danille Dimartino. And perhaps more importantly, it was featured in Chinese media — I saw it in the South China Morning Post.

The Chinese people are talking about it, even if it is behind closed doors away from the surveillance state.

The Chinese government is thinking too. The PLA could have stepped in and squashed the protests in Hong Kong in an hour… but Beijing knows that the idea of free market zones is far more important than just Hong Kong. Its also Shang Hai, its Tainjin, its the economic growth engine that is keeping Beijing in power.

Hong Kong’s independence can be crushed easily, but doing so would end China’s economic “miracle” by triggering a massive brain drain. Lots of people in China have already implemented a “plan B” to leave — witness the Chinese money laundering that inflated real estate prices in Vancouver to SanFran to London. Hong Kong ex-pats are looking at TaiPei too.

I would not be so sure that China has any more flexibility than other bloated governments. Beijing needs its tax base to keep the big government baby fed.

Imagine a country, free of suffocating, destructive, crony capitalist central bank ruling…..well, you don’t have to imagine, it exists. Iceland.

2016 +6,6 % GDP

2017 +4,6 % GDP

2018 +4,6 % GDP

2019 +2,3 % GDP Q1+Q2 counted

Government debt to GDP: 37,50%

Private debt to GDP: yeah….high, but coming down in an amazing rate.

They managed to actually reverse the mess rogue bankers made.

Why o why does this country fare so well? Because bankers went to jail for the crimes they committed.

Considering joining the EU.

Being homogeneous and independently minded helps.

Someone should fell them what joining the EU actually means.

…and yet the ISK is losing value against the big CB’s manipulated currencies…. just like NOK, SEK….and yes… RUB( hardly any debt nor insane social liabilities, unlike ours)…Nothing makes sense anymore…I am afraid..

Iceland has its own currency, hence they have the ability to lower devalue their currency against USD/EUR/RUB/etc.

That’s what DE/NL/FR/ES/I/etc can no longer do.

hard times https://www.youtube.com/watch?v=9py4aMK3aIU

I’m betting on the US decoupling. Re-shoring has a big negative impact on China and a positive impact on the US. Europe has a lot of structural problems and awful policies.

The US can decouple IF we avoid the policies of the left. I guess that is a big IF!!

Decade long (pretend)permanent never ending “recovery” and it only cost 15 trillion.Obama took office the deficit was 10 tril,when Trump leaves office it’ll be 25 and change,that’s 15 tril in 12 years with nothing to show for it (less than nothing).Bezos and the Google twins ,Blankfein and Dimon made out like bandits,everyone else……….not so much!

Dollar, Gold, Utilities, REITs, US Long-term bonds.

Most economic analysts, like Mish seem to take eternal growth for granted, blaming Brexits, trade and other wars for the present slowdown while the latter are merely symptons or consequences of a already unhealthy, unsustainable, debt driven economic situation artificially sustained with even more and even cheaper debt, a dire situation that can no longer be interrupted without causing economic and social disaster… so lets make debt a bit cheaper still….If this isn t a textbook example of a vicious circle, there will never be another one…..Of course this massive festering ulcer is bound to burst at one point ….it will be awfull….economically, socially…

Such “ulcers” always keep weakening the host by sucking up ever more resources which could otherwise be directed productively; until the host can (nor will) no longer defend neither itself, nor the ulcer, from sacking from the outside.

Negative interest rates will be the death of the West; the last time I looked, the US economy was a part of that and is headed in the same direction. Decoupling is a fantasy, at best.

Central banks were the death of the West. Dying just takes a while for creatures as big as entire regions of the world. Exactly whether some central bank happens to arbitrarily set interest rates at +X or -X at any given time, is just a technicality. They’re setting it wrong regardless. I do, however, recognize the constant lowering over the past decades, is a sign the final death throes are getting closer than they were prior.

“Mish Comments

This is not 2012 or 2104 where stepping on more QE would help.

The US is not immune to a slowdown in Europe and China, just as China was not immune to a global slowdown in 3007.”

Wow, Mish, going way out there on your predictions! So specific on the dates too. (Are you secretly a time traveler?) 😉

Q3 and Q4 will tell us how things really are. I’m especially interested in the German slowdown, since really the EU revolves around Germany.

If the recent South-Korean export data is an indicator, that might make for some interesting developments.

I believe “Realist” constantly predicts low growth.

He is beating most of us on growth predictions but he has been hedging his comments recently. A smart move

It could mean 1-2% GDP like we saw from 2010 until 2014. Another rate cut all but guarantees just slow growth rather than a full blown recession. One prediction I’ve not heard anywhere is slow growth is a possibility.

The pattern ever since the crisis has be the same, one step forward, one step back https://fred.stlouisfed.org/graph/?g=oXaw. The is no reason not to believe that one the 2018 stimulus fades that gdp won’t step back. Interestingly though this will happen as there a global slowdown which could have additional effects. I don’t think cuts are going to do a thing at this level.

I guess Fred graphs don’t pass though, sorry. I would delete the post if I could