Anne Kunz and Holger Zschäpitz co-authored an excellent article for Welt (in German) called the Interest Rate Business Model is Dead.

Here are some excerpts via Google translate with many of my own modifications. For example, the title itself is my translation, not Google’s.

Google has the title as “Business Model With the Interest is Dead“.

I made an educated guess that Google’s title isn’t quite right.

I picked up the article from this Tweet.

Translation errors below may be Google’s or mine. I took a fair amount of liberty, adding some words, deleting others, or changing the word order so the result makes sense to me.

Apologies to the authors for any of my errors.

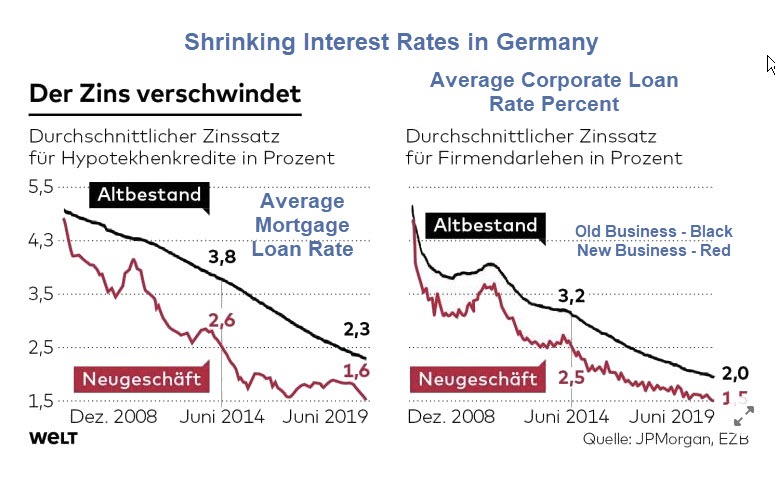

Interest Rate Business Model is Dead

The cash cow bank lending model is dead, buried by the European Central Bank (ECB).

The coup de grace came at the recent meeting. As ECB President Mario Draghi squeezed the negative interest rate for banks even deeper.

The ECB will restart its bond purchase program in November. This time, without a time limit. Thus, the monetary authorities have permanently chained the long-term interest rate at a low level and cut the profit opportunities of the financial sector to a level that isn’t sustainable. For a long time, institutions have made good money from the difference between long-term and short-term interest rates.That time is now over.

In 2016, Commerzbank employed more than 50,000 people. CEO Martin Zielke wants to close one-fifth of the 1,000 branches and even wants to part with an important source of income including his Polish subsidiary MBank. The workforce should be reduced to around 38,000 by the end of 2020.

The sale of Mbank is a desperate attempt at salvation.

In terms of stock market value, Deutsche Bank and Commerzbank are now loosely hanged even by more regionally active institutions from Norway and Sweden. [That is a direct translation that reads wrong but I do not know how to fix it].

Even the once proud Landesbanken is a restructuring case. This is a dangerous development.

“With the allowance, the ECB has relieved the German banks in the short term by around 500 million euros. At the same time, banks will be burdened considerably by the continuation of the low interest rates for an indefinite period, “says Peter Barkow, financial expert at Barkow Consulting. “Especially the German banks are very much dependent on income from the long-term investment of customer deposits at higher interest rates, called maturity transformation. This strategy only works very limited, “warns the expert. [The allowance refers to the ECB not charging banks a portion of the negative interest on excess reserves]

However, the corresponding earnings impact on the banks will only be delayed. “Many German banks have to find new sources of income in the medium term. In the short term, a further reduction in costs will probably be necessary, “says Barkow.

For more than a hundred years, banks lived on long-term lending or investing in securities their clients entrusted to them in the short term .

Historically, banks made money out of time. If time no longer has a price, because there is no more interest, nothing can be earned. Ten-year Bunds yielded around 1.5 percentage points more than two-year issues in historical terms. Currently, the difference is just under 0.2 percentage points.

In the multi-billion loan portfolios, the institutions are losing a lot of money due to ECB policy. Accordingly, the shares of Deutsche Bank and Commerzbank have fallen in sync with the interest rate differential. How dramatic the situation is for the banks, the analysts of JP Morgan have written down.

In a 120-page analysis, JP Morgan analysts calculated what effects the ECB policy will have on the banks. They used Japan as an example. Japan has had negative interest rates for some time now and there institutions have been unable to earn anything for two decades with time. The JP Morgan analysts’ conclusion: Interest margins could continue to shrink and continue to weigh on the earnings side.

“The negative interest rate policy of the ECB is ruining the financial system and is a socio-political poison,” says Frank Kohler, CEO of Sparda-Bank Berlin. The financial system is absurd if we have to explain to the children that money has a negative value – and thus debt is good, because you may not have to repay everything.

Socio-Political Poison

Bingo.

Thanks to Anne Kunz and Holger Zschäpitz for an excellent article and apologies again for any translation errors I may have made.

Mike “Mish” Shedlock

Borrowing short to lend long is part of the problem. It defrauds both the depositor and the borrower while destabilizing the banking system.

For example, If I — as a depositor — make a three-month deposit, and the bank lends this to a company for 12 months, the bank has defrauded me of the higher interest (for foregoing to use my capital for 12 months) and the company (borrower) by the bank claiming it has capital available for 12 months, when in fact it’s only available for three.

Earning money from taking a spread between the price offered to the depositor and the price offered to the company/borrower is fine — all companies make money from taking a spread. Lying to the company — by claiming the company has capital available for longer than it really has — and lying to the depositor — by lending out his capital for longer than he has agreed to — is not fine.

This is a good German doco on the subject (English version) https://www.youtube.com/watch?v=t6m49vNjEGs

Negative rates are just another form of default. It is just a more brazen way of borrowing without repayment.

Instead of defaulting after you borrow, now you default before you borrow.

The main consequence will be a scramble for alternative stores of wealth.

Are low/negative interest rates mostly caused by demographic changes?

With an ageing population and huge amounts of money being funneled into retirement funds, where can that money go? Most of it has to go into bonds as that is the law. The result is that bond prices go up and returns on those bonds fall. That is the price to pay when you have forced buyers in the system.

Also, as the number of workers falls, the opportunity to invest and make money falls as well, so demand for money for productive investment is falling.

Lastly, a central bank trying desperately to stop the banking system from having any casualties at all. I am sure that the ECB is buying bonds at top dollar in order to keep some banks in the EU from failing, so bond prices rise even more.

Seems to me like a triple whammy. Forced buyers for certain types of debt, misplaced CB intervention and falling opportunities for investment are bringing about these absurd rates. I am pretty sure that sooner or later something bad will happen, though I suspect it may take some time.

I know that I can survive a recession. I’ve done that many times. I’m not sure that I can survive negative interest rates. Better the devil you know.

Banks, insurance companies, the entire financial sector will become one large morass of speculation. Capital will be consumed and accounting profits will disappear when the heroin is removed.

The similarities between the ongoing financial crisis and the one following the French Revolution are eerie despite the predictability of it all. We have slo-mo technology here in the Modern Age, and things can take a long time to play out, but despite that difference in pace, the Euro is now essentially the Assignat.

The faster things begin to move, the closer we will be to The End. That’s another lesson the Assignat Economy taught us all. They will have to keep pumping harder and quicker to keep the economic ship from sinking.

Historians will note the curious lack of panic (can you say “slow growth”?) as all asset class yields approached zero presaging the monetary crises of the 2020’s.

Who was it who said ““If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around them will deprive the people of all property until their children wake up homeless on the continent their Fathers conquered.” The fact that it wasn’t Thomas Jefferson who said it doesn’t mean that it isn’t true. That’s exactly what has happened in my lifetime.

Better go re-read your history books there@Carl_R … the US didn’t have a national currency until after the Civil War (briefly) and that was extremely controversial at the time — necessary to pay war debts but controversial. A national currency didn’t happen until the Federal Reserve was created in 1913… roughly 137 years after the country was founded.

The majority of the founding fathers were extremely distrustful of a national bank, and repeatedly resisted efforts to create a permanent one. The First and Second banks of the United States were authorized by Congress with strict lifespans, and neither authorization was renewed.

Sound money isn’t about private banks or politically controlled banks. Its about making proper loans and its about paying debts.

When politicians decided that debt didn’t need to be repaid, that loans must be issued to politically favored entities… the Federal Reserve system went the same way as failed private banks before them.

Sorry Carl_R… you failed banking history

Huh? How did I “fail banking history” when I didn’t discuss banking history, or at least, not history prior to 1976, since which we’ve see a cycle of inflation and deflation? Rather, I simply gave a quote that has been falsely attributed to Jefferson, but which was consistent with his thoughts, and asked who actually said it, and then compared it with the current cycle. The first time the quote appeared was in 1937, long after Jefferson’s time, so proper attribution would probably be to someone of that time period. As Abraham Lincoln said, “The problem with quotes on the Internet is that it is hard to verify their authenticity.” 😉

Banks maintain fractional reserves of what they lend, meaning they have far more lent out than they actually ever had on hand. In the old days, they just printed their own money in the form of bank notes. In one way or another, this has been going on since the De Medicis in the 16th century.

The real “founding father” of the USA was Alexander Hamilton. He’s the guy who brought everyone together and worked out the deals necessary to end the Articles of Confederation and create the US Constitution. Hamilton was a banker. He understood banks created money, and whomever controls the banks becomes rich. He wanted to be that guy.

Hamilton was a federalist. Jefferson was his arch-nemesis as an anti-federalist. While the quote presented did not come from Jefferson, it fell in line with his thoughts. But Jefferson’s solution was to have Congress just print fiat money directly and hand it out. Not a great idea either.

Thinking ahead, can any real fix be created by the same people running the show now?

The answer is probably no as its outside of their ability to imagine.

So, who will be able to fix the mess? Who is in the wings with the right ideas?

We can say the old guard are unlikely to relinquish any control of the system without either complete meltdown or being forced out. Only complete collapse will discredit them enough and give fresh ideas a chance. Until then those in the wings are best waiting. Let the blame lie where it belongs.

Collapse it is with all the suffering that goes with it. Unfortunately it could lead fo a stronger ECB and EU in the interim.

Big governments depend on big debt markets. The central bankers really didn’t think through the long term consequences of wrecking the debt markets.

No government has ever gone to war with its own tax base and “won”. They never will.

Think Vietnam, except its an economic war. The government will win every major battle, but still lose the war. Quagmire applies to economic wars too.

The failure of QE and ZIRP are a good example. Did you see the awesome power, the shock and awe, the glory of the King’s mighty word? They unquestionably won the battle, but they now find themselves even further behind in the war.

The Central Banks think they can:

Spend it now, you bad bad savers.

Borrow and spend or we will beat your cash out of you.

How about the doom loop of creating institutions that grow more powerful, and closer to their ultimate target, through crises?

That’s what the ECB and EU are. Answer to all crises is more integration that makes the ECB, EU more powerful. Like big sucking black holes that will crush all into one.

ECB will always encourage crises as will the EU until people shout STOP. through the ballot box or by direct action.

“A system of capitalism presumes sound money, not fiat money manipulated by a central bank. Capitalism cherishes voluntary contracts and interest rates that are determined by savings, not credit creation by a central bank.”

― Ron Paul

It is challenging when your bank asks you to keep no more than €10m in your current account at zero because they are getting wacked by the ECB to the tune of 40bp. I hate investing excess funds at -22bp … legally I could stick to my guns and insist on zero as outlined in the original account agreemen, but they’d just terminate the relationship and I’d have to re-negotiate at new terms that could go severely negative the way the ECB is running the show. I’m torn because the banks have screwed us on fees for years, but a dead bank does nobody any good.

One of the most interesting ramifications of negative interest rates is that the “proper” PE is historically about 1/(i+2) since stocks normally return a couple percent more than bonds. If the interest rate goes to -2%, then the PE goes to 1/(-2+2)=infinity. Similarly real estate prices can go to infinity as well. Why? Because if your return is negative holding cash, any positive return is better.

So what’s the problem? It’s easy to make money with negative rates. Just keep borrowing infinitely. Just keep borrowing one negative rate loan to repay another. Since you only have to pay back less than you borrowed with each loan, you just keep making more money the more loans you take out. Nothing could be easier.

The new business model is borrowing money.

Because there are no loans with negative rates. Read my reply to your previous post.

Even if you could borrow money with a negative rate, there is no guarantee that the rates will stay negative, and I guarantee your rate will float with prime. Things can flip the other way in a hurry, and then, can you pay it back?

I don’t see what the problem is. With positive interest rates banks made money arbitraging the different rates of short and long term debt. Why can’t they do the same thing with negative interest rates? As long as there are differences between different maturities of debt you can still make money arbitraging those differences regardless of whether the rates are positive or negative. Instead of borrowing short and lending long maybe you borrow long and lend short?

Heck, if a bank can borrow money with a negative rate then they can just keep borrowing infinitely since they always have to pay back less than they borrowed. Seems like a foolproof way to make money.

There are 2 interest rates. Coupon and yield to maturity. The coupon rate is what you agree to pay in interest every month on the amount you borrow, That is not negative. The yield to maturity is the annual interest you receive if you purchase the loan and this is what is frequently negative. It’s negative because the cost of the debt went up. I.e. you paid $110 for a $100 loan that pays 1% interest for 8 years. The only reason negative yielding debt exists is because central banks will pay the $110 because they don’t care if they lose money. They just want to push $110 into the economy.

If you take out a loan, you’ll pay the coupon rate which will be positive.

Are you saying there is no such thing as a bond with a negative coupon rate?

It should be added to this, these days even bonds issued in the primary markets sport negative yields to maturity already at issuance. Moreover, interest rates in European money markets (interbank lending markets) are negative as well, which is why some Danish banks were recently able to offer negative rate mortgage bonds.

For some reason the editing function doesn’t work- “mortgage bonds” should read “mortgage loans”.

Bank balance sheets – therefore, banks themselves – will shrink.

Bank lending is based off deposits. Would YOU give your money to a bank that will CHARGE you a fee? Also, European banks do not have US style FDIC protection.

Pay banks to hold your money + risk of bail-in? No thank you.

Money will flow off the continent.

Banks don’t need your deposits if they can borrow money themselves with a negative coupon rate. They can just make money off of borrowing money since they never have to pay back more than they borrowed.

Huh?

Banks operate with balance sheets. Assets (loans) – liabilities (deposits) = capital

The function of a bank is to attract deposit and lend them out (fractional lending) and pocket the spread.

Whatever you are suggesting is not banking … and how is that good for people … and why would politicians allow to exist?

Negative interest rates are clearly a bad thing and drive mal-investments. That said, I don’t see why banks can’t just make money hand over fist by changing their business models to just borrow money with negative coupon rates. You just keep repaying one negative interest loan with another negative interest loan, and so on and so on… It’s better than a perpetual motion machine. Since the bank never has to pay back the full amount of the loan, they can just use the next negative rate loan to pay off the previous negative rate loan balance and pocket the difference.

This will take us all to hell in the end, but a bank can certainly make a tidy fortune while the negative rates last.

I am not sure that these rates are available to anyone. If they were, I would borrow money at a negative interest rate immediately, as much as I could on the proviso that I could either fix the rate, or repay if rates changed, or I could get a swap to insure my position.

I suspect that in reality, banks and individuals dont get the ability to take both sides of the trade. It is this inability to borrow at a negative rate that allows governments to force rates negative. I think that banks are in the same fix, they cannot borrow at negative rates, only lend at negative rates. Without this interest rate apartheid, rates could not be negative at all.

Anyone remember the Lisbon Treaty enacted December 1, 2009? It fixed the flaws in the ECU founding treaty and has led, thus far, to negative interest rates, Lying Juncker and “Whatever it takes” Draghi, both now staring down the barrel of a Halloween Brexit.

Germany really didn’t care so long as her export engine and de facto monetary control remained intact. Now, she cares.

Doesn’t care enough.

When you see effigacies burning then we know she gets it.

Was invested in community banking for over 30 years and have gotten out. I just don’t see a future for banks lending at low rates. For smaller banks, the regulations and expenses don’t make any sense. The smaller banks will go away and you’ll have more mega banks – all too big to fail. These banks will be able to take huge risks at taxpayer expense and always have a bailout backstop.

Responsible people that save and want to retire are screwed. No way to get there with rates approaching zero without significant risks – and no bailout for you!

Zero interest rates (low or negative) are hurting economies and productive people.

Those “closest” to the cheap and easy money will become richer and richer. Assets prices will continue to become more insane. The middle class will be further priced out.

The wealth gap will continue to get wider and wider.

Democrats will demand bigger and bigger government with more and more regulations and higher and higher taxes to fix it.

G7 governments (all of them, not just the USA) will struggle to fund existing promises. They will use all sorts of trickery and legal word play to default on as many promises as they can. They will compel pensions and the like to buy sovereign debt at cheap rates. And in spite of this, it will be a multi-decade struggle to keep the party going.

I’m not saying the politicians won’t make grandeouse promises. I’m not saying there won’t be all sorts of proposals to create the department of spending money ever faster…. I am saying that all the politicians will face the reality that they cannot fully fund their existing promises.

The Dems will need to decide if they want to dismantle social security and medicare. They will be cutting benefits to the rich and middle class whether they like it or not. The only question is by how much.

Both parties will need to think carefully if they want to close military bases in their home districts, or do they want to be a LOT more selective about which wars the country gets into. Overseas military bases (those in somebody else’s district!) will close to keep the party back home going.

Fantastic article. And these Germans are correct, it’s poison to society, especially local communities that have a branch that still has humans working in it. All those jobs seem to disappear, those communities become more sterile and economically weaker because of these incompetent, yet destructive central bankers. I wish I could use a whole bunch of bad words here….but you already know about those words.

And again, like my comments in other articles, it really surprises me that the Germans are letting this happen. Is it the grand project of the EU which is above all? Are all Germans now castrated and afraid to speak their minds or is the discussion not public enough yet?

“it really surprises me that the Germans are letting this happen.”

….

I’m sure the rank and file Germans are pissed. But the narrative is controlled by the top 5% (aka those with large equity portfolios) and they will cheer as stocks go up.

Central Banksters will employ what I call the Rumsfeld Defense. No matter how bad situation appears, things would have been worse if ANY other option taken.

Germany is as trapped in the low rate high public debt and economic deflation as high debtor countries in EU. They cannot raise rates without EU falling to pieces.Then there is the view that low rates and central bank purchases will create the mutualised political fiscal and unified issuance outcome sought by some for EU, Germany (leadership) as creditor stands to gain position in EU in this scenario. All EU countries have sold out, it is on the verge though.

At a wider level, we see what ? The older middle and upper class are reaping from asset price increases supported by low rates and new debt taken on by younger generation, who will be dependent on rates staying low to keep money flow and payment. Many are closed out of the market. They will demand or accept mmt to reset. This is generational conflict where traditional model of community, hierarchy and outlook are being destroyed, where values are being destroyed. They are right, it is poison.

Germans have given away their control to a pooled sovereignty that only cares about preserving and growing itself and its control – EU, ECB.

These parasites will kill the hosts.

Germany was routinely outvoted at the ECB Council at the time this madcap policy was conceived.

Some years ago (1965) My family visited relations in Germany. Whilst there one of my cousins showed off his brand new Mercedes. He’d been on a waiting list for four years, saved religiously and had paid for the car in cash. First you save then you spend. I cannot imagine the Germans tolerating this situation for long.

Yes sir, that’s how I’ve always knew the Germans, Dutch to be. Very down to earth, extremely prudent and big savers. Somehow I still cannot believe our ‘leaders’ sold our souls to ‘the Project’. Because it’s all connected.

The post-Bretton Woods debt-based, fiat monetary system has already far exceeded its shelf life. Unfortunately, abominations such as negative interest rates are now required to keep it from imploding into a deflationary black hole.

Why deflationary and not Weimar or Zimbabwe type hyperinflation?

No demand?

Debt-deflationary super-crash happens first. How it is dealt with from a policy perspective determines whether or not the hyper-inflation follows.

Deflationary black holes are good things. As well as necessary things, after over a century of runaway inflation have distorted everything.

and thanks for your blog Mish👍!!!

early retired in august. do not trust the swiss pension system or any for that matter. took everything out in lump sum. and not paying back the mortgage.

Well, you got to put it somewhere.

Are you kidding? This is time to lever to the hilt and buy a Chateau or Burg with a moat. Possession is nine-tenths of the problem.

Central Bank Decision Making Tree

It has been very clear for a very long time that at the tippy top of the Tree rests “what will make the stock market go up?” Wealth effect reigns supreme. No matter what impact rate cutting / QE has on real economy.

However, since the policy will eventually lead to a shrinking pool of real funding, it is destined to fail even with respect to this objective.

Pater, any chance that the NIRP state of affairs in Europe is the cause of the Emergency Repo measures? I can see not wanting to accept NI bonds as collateral, if one had better options, but would this ever be the case in US money markets? And solvency of their banks sees irrelevant since the JCB has kept their Zombies stumbling in spot for a couple of decades. I’m curious to know what you think the counterparty trust problem stems from.