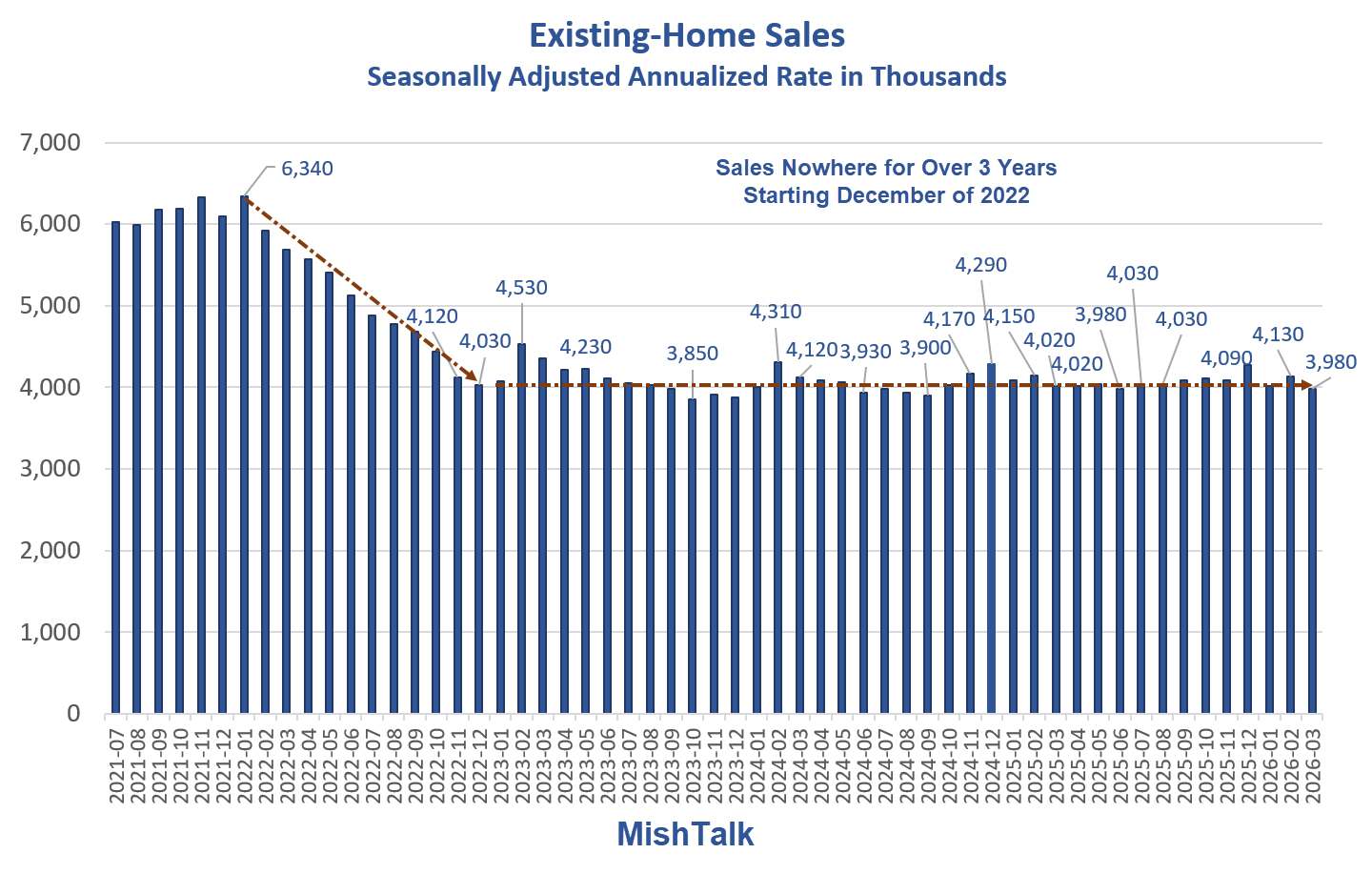

Sales drop 3.6 percent in March, have gone nowhere for over 3 years.

The National Association of Realtors reports Existing-Home Sales Decline 3.6 Percent in March.

According to NAR Chief Economist Dr. Lawrence Yun, “March home sales remained sluggish and below last year’s pace. Lower consumer confidence and softer job growth continue to hold back buyers.”

“Because inventory remains limited, the median home price rose to a new record high for the month of March,” Yun added. “That price growth has helped the typical homeowner accumulate $128,100 in housing wealth over the past six years.”

Accumulated Wealth Myth

No one has accumulated any wealth over this other than landlords who raised rent more than their expenses have gone up, and those who refinanced mortgages at a much lower rate.

Everyone else lost wealth due to rising property taxes, homeowner’s insurance, and HOA fees.

The wealth impact of rising home prices has been negative for many, if not most homeowners, especially those who purchased late in the game and did not refinance lower.

Existing-Home Sales Month-Over-Month

Key March 2026 Statistics

- Sales Month-Over-Month: 3.6% decrease in existing-home sales month-over-month to a seasonally adjusted annual rate of 3.98 million.

- Sales Year-Over-Year: 1.0% decrease in sales year-over-year.

- Inventory Units: 1.36 million units: Total housing inventory2, up 3.0% from February and 2.3% from March 2025.

- Inventory Supply: 4.1-month supply of unsold inventory, up from 3.8 months last month and up from 4.0 months one year ago.

- Median existing-home price: $408,800: Median existing-home price3 for all housing types, up 1.4% from one year ago ($403,100)—the 33rd consecutive month of year-over-year price increases.

- Market Time: 41 days: Median time on market for properties, down from 47 days last month and up from 36 days in March 2025.

Existing-Home Sales Year-Over-Year

It took many years for year-over-year sales to turn positive.

Sales went negative again in 2025, and have now stabilized at a low rate near 4 million, seasonally adjusted, annualized.

Existing Home Sales Supply

The NAR does not seasonally adjust much of its data as evidenced by the above chart.

Nonetheless, we can see rising supply over time. But rising supply has not helped sales.

Existing-Home Sales vs Mortgage Rates

There are sometime jumps in sales when rates drop. However, there has not been any lasting traction.

Sales have basically gone nowhere even as rates fell from 7.62 percent to 6.05 percent.

But rates have risen again. The current Mortgage News Daily rate is 6.41 percent.

MND is more accurate than the Freddie Mac data in my chart because it includes points and fees. I use Freddie Mac data because I have a download from the St. Louis Fed.

The MND rate bottomed at 5.99 percent on February 24, spiked to 6.62 percent on March 26, and is now 6.41 percent.

Not even that dip below 6 percent did much for sales.

The only conclusion is home prices are still too high, mortgage rates are too high, or both.

Jobs and inflation from the war in Iran are also huge concerns.

Related Posts

On March 30, 2026, I cautioned Powell Warns the Markets and Trump that His Patience with Inflation Has Limits

Powell’s speech was to Harvard students but read between the lines.

Powell’s warning was aimed straight at Trump.

On April 10, 2026, I noted Consumer Sentiment Drops to Record Low in April, Consumers Blame the War

The war and resultant inflation is what forced capitulation by Trump.

This bubble is so incredibly long in the tooth. Boomer lock-in effect or not, inventory should have surged much more by now. The government clearly has numerous thumbs on the scale.

The nomenclature you use in this post is a little loose/confusing, Mish.

Wealth is a stock variable. Housing payments/taxes are flow variables.

So most homeowners have accumulated more wealth over the past several years because home prices have dipped very little (if any) over most of the US during this period. Granted these homeowners don’t have more cash/wealth in their checking accounts (unless they sold and downsized) but they do have more wealth.

You mention “wealth impact” in one statement. Maybe there are some people who feel a lower disposable income effect with higher housing insurance and property taxes on a ‘fixed’ income. And they don’t feel comfortable increasing other purchases from their increased ‘paper wealth’ of their homes.

But they could – if they chose to – because their wealth is higher currently.

How could they do that? Other than a reverse mortgage (for the retired crowd) or moving to a lower cost home there is no way to tap that paper wealth (HELOCs are loans).

Incidentally moving is very expensive. You may trigger capital gains if your home appreciation is 250K (500 for a couple) and paying 4-6% of your home value to a real estate agent and then potentially another 10-15K for movers can eat 100+K of that paper wealth in a heart beat.

First, in your scenario, for someone to trigger capital gains on a housing sale, they have accumulated a lot of housing wealth. And that was my point – Mish seems to be saying housing wealth is decreasing, and I don’t see it for most.

But there are LOTS of way to transform that paper housing wealth into current spending dollars if you so choose:

Reverse mortgage

HELOC

Downsizing (and pocketing the cash difference)

Feeling comfortable cashing out some stock market gains since your housing wealth is now higher

Spending more/saving less of your Social Security or cash accounts since housing wealth is now higher

Drawing down your ‘nest egg’ since you can leave your higher housing wealth to your children that way…

These are all examples of the “wealth effect” and are real to many people, especially those in the upper part of the K-shaped economy

I think (obviously only Mish can confirm if this is his thinking too) what Mish was alluding to is that the paper gains are being subtly eroded by taxes/insurance/maintenance/utilities/HOA fees etc.

By this I mean if your taxes/insurance/maintenance/utilities/HOA fees add up to 30K a year and you remain in your home for 10 years you paid out 300K. If the appreciation on your home in those 10 years is also 300K you netted 0 gain (paid 300K to net 300K).

Gains are often misleading. We purchased a house in East TN five years ago. Value increased about $199K in those five years but we did about $90K in upgrades and maintenance, selling and moving would cost about $50K so actual gains would be much lower. We have a mortgage a 2.92% so selling is out of the question barring an emergency.

If home prices haven’t dropped since 2022 where you live, they’re not going to drop.

Most areas of the country never saw an actual drop in home prices. At best they leveled off in 2022, then continued going back up ever since then.

A few areas in particular (Northeast U.S., Wisconsin) have seen double digit price increases the last few years. Illinois was late to the post-2022 madness, but prices there have gone up quite a bit the last couple years.

Oh, and Trump said the quiet part out loud a month ago that “they” won’t let house prices go down, and he’s right. “They” will do whatever it takes to keep stocks and home prices elevated, even if it means printing money up and handing it out like candy like they did from 2020-2022. Why? The system will implode if asset prices aren’t kept inflated.

The people who think we’re going to have a “deflationary collapse” because of the Iran war are completely delusional. Not going to happen with a fiat U.S. dollar that they can create at will.

I disagree. There will be a collapse and you can bookmark this and ridicule me if I’m wrong. The only thing I’m not sure of is the timeline but let’s get real on one thing….

The real estate “burden” of property taxes, insurance, maintenance and now utilities cannot and will not be sustained. In many states (YT video below), utilities are now more expensive than mortgages!

https://www.youtube.com/watch?v=B7YgiUBUNlk

The only way this can be sustained is if wages explode and that’s not been happening based on the latest pay labor report.

This is a large part of the reason why I’m leaving the US. Even though I’m considered “rich” with millions in the bank, I’ve done the math and there is no way I can survive till death at 80 much less 90 or 100. I haven’t even talked about the rising costs of medical costs, health insurance and other expenses.

Of course the “poor” get SNAP, social security, disability or whatever other social program to get by, we won’t qualify for any of that I guess until we’re dead broke but why live here like peasants when we can live like kings elsewhere?

Got exit strategy?

Where do you currently live? I live in the Hartford, Connecticut metro area and it is the hottest housing market in the country right now. Extreme shortage of rental units and houses for sale. Rents have gone wacky high here. So yeah, I’m kind of biased because of where I live.

But I see similar things in many other northern states. The housing market is locked up because people don’t want to give up their 3% mortgages, so it’s resulting in home prices continuing to go up despite mortgage rates being over 6%.

Australia and Europe prices have also gone wacky since 2022 despite the high interest rates. Demand is outstripping supply.

So yes, I will take you up on your bet. Average home prices in the U.S. will continue to go up from $425,000 where they are now. They will cross $500,000 and continue to infinity like every western country has since 2008.

The catch to astronomical house prices? A loaf of bread will eventually cost $20 as they continue to debase the currency.

At the moment I am in Texas but move from here to Europe or Asia depending on where money takes me. I may be headed to Australia next month and then SE Asia but that depends on fuel availability and where this Iran crisis takes us….I may settle for South America.

I am bookmarking this in my calendar for a year from today. I don’t think it will take that long for prices to go down but we need to set dates.

I’m not at all surprised you live in a state that had an actual housing bust in 2022. But Louisiana (also a bust state) has seen upward price increases over the last year. Not all of Florida is a bust, as there are plenty of wealthy Northerners still moving down there.

I looked up Chicago, where Mish is from. Chicago had a pullback in prices in 2022. Prices bottomed out in January of 2023 at $260,000 for an existing single family home (per Redfin data). Today, the average price is $340,000, an increase of 30% in 3 years. There obviously are plenty of people willing to pay ever increasing prices there. The alternative is to go homeless.

Out of curiosity, where are you getting your data from for all of these various locales? Is it free?

Redfin.com, under the “buy” tab there’s a “U.S. housing market” tab. On that page, enter a town (or county, or whole state) and it will show you sales and prices per month going back 5 years. It’s based on sold listings in the MLS.

Wolf over on Wolfstreet posts prices since 2003 for all the major metro areas. His graphs are well worth looking at to see which areas had the biggest runs ups and busts in the 07 crises and now since Covid in 2020.

people being unwilling to move isn’t the problem. build more.

The NE is the only place bucking the larger downward trend…due to investors and Boomers camping on their properties far longer than other generations did. With the stagnant population we have, that Boomer phenomenon will wear off.

Agree with you 100%.

The non-mortgage burdens are skyrocketing. My mortgage is a very reasonable 1000/month (3% rate and low balance) but my escrow (taxes + insurance) add another 2K to that for a total cost of just over 3K a month. Even when I finish paying off the mortgage I won’t be able to get rid of that 2K a month (and rising yearly) carrying cost.

A whole bunch of this is tied to public pensions at all levels (city/state/federal) that can’t ever be gotten rid of until bankruptcy laws change. There just no way people should be collecting 100+K a year pension from early 50s to end of life.

Not true at all. Income to price ratio is a metric which has never not reverted, and income growth isn’t going to cut it so prices are going to have to do the heavy lifting. To believe otherwise is to believe in “new paradigms”/”permanently high plateaus” and I for one don’t believe in either (yet). Absurdly low inventory is what’s keeping cardboard and wood shelters unusually valuable, but that cannot last forever in a country that isn’t growing and that generally encourages new construction. The government is doing a fantastic job of delaying the inevitable, but the market will run away from them eventually. Prices are already down noticeably in most of the South, despite the shenanigans.

I say this every time, but, it’s that the prices are to F’ing high still! And I say this everytime as well. I wish you would take these charts back to say, 2018. This would show a “normal” market, the outrageous numbers during Covid when Mortgage Rates were outrageously low and both the number of transactions skyrocketed along with price,and finally this “post covid” lull.

My estimates (Im a realtor in the west Houston area) show that it will take approx 2 more years,without any price appreciation, to return to “normal” prices. Of course this doesn’t mean that a buyer should wait. If you need a home, you need a home and have to find one that meets your budgetary and other needs (location,size,schools,etc). But, I don’t expect prices to move much for the next few years, and, if prices don’t move (unless it’s downward), then the number of transactions is not going to change meaningfully.

All of those local government entities who appear on property tax bill line items, including their pensions, cheerlead ever-increasing “real estate values”. “World-class public school districts”

In my area they are shutting down 8 schools but I guarantee you that they won’t be reducing the property tax rates, they’ll just use that money to pad pensions.

I think it will be more like 2030 before the Covid money finishes sloshing through the economy and settles entirely in the hands of the 1%.

Some markets are already close to the long term trend line but most are not.

Democrrats dumping covid money, 3% interest on houses and 20 million illegals has locked up the housing market for 4 years already–no one knows the solution to this market yet.

But I thought Donald Trump was elected to fix all that so what happened? Are you saying Trump is a total failure?

Trump did build that wall, didn’t he?

If only poor people had immigrated instead of millions with great jobs and able to afford a $400k mortgage!

adding supply of lower priced homes. this isn’t hard to see, but for people hung up on politics first, they’ll never admit it.

There are solutions but the Boomers will never allow them to be enacted.

Yeah im seeing lots of for sale signs hanging around for months in my part of ca.

who can afford fire ins. Guess we might find it would been cheaper to address carbon emissions back during the carter adim.

Spec builders by me have closed up shop (Trump policies have actually been having an impact on availability of illegal labor, so “winning”?)Remaining McMan’s on the market $2.5-3.5M sitting now for months, well past when they would have sold at the 2025 peakSome renovations happening — renovation market was dead for a decade as folks just bought NEW, these are people that would have traded up but threw in towel when prices crossed $2.5MPrices cuts across all sectors since Don Tzu’s initiative

Summary: Real Estate going down

“Summary: Real Estate going down”

I disagree. The real estate market isn’t the stock market where you can have a diverse, fluctuating portfolio and most folks can lose 20% and just try harder. The real estate market is tens of millions of middle class folks hanging on by their fingernails and can’t afford any loss. So the real estate market will just lock up (as it has) with the only sales being by people selling their dead Mom’s house, or someone forced to move for work. And with insurance, taxes, and general maintenance going higher, it is a boat anchor on the entire economy. Since people aren’t moving, the labor market is locking up too.

You must have been away for 2008-2013

I absolutely was. But there was a significant difference between then and now. Remember anything about a banking collapse and sub prime mortgages? Details matter.

Yes, subprime and strippers buying multiple properties to flip in FL and Vegas, remember it well.

This run-up, issuing $2.0 million mortgages on a $2.5 million house happening every day — or was. What could possibly go wrong? We’ll find out if the economy tanks. I know many, many people who are over extended — they are going to smoked if the economy hits the skids.

I agree completely with everything you said. The middle class people you speak of bought when prices were far lower and they are carrying 3% mortgages. So even though their insurance and taxes have gone way up, they are still able to afford the bills relative to new entrants paying nosebleed prices at 6.3% interest rates.

People downvoted you because they want and/or think prices “need” to fall. Sorry, but prices are going to be very sticky without massive foreclosures like in the 2008 bust. Don’t see that happening.

I got tired of reading Wolf Richter’s doom and gloom real estate posts since 2022/2023 and he doesn’t allow alternative viewpoints. He keeps on telling his readers what they want to hear despite the data showing otherwise, which he twists to adhere to his narrative.

Home buyers are waiting for the “off season” to make an offer. Families with school age children avoid moving during the middle of the school year, and have a narrow window of time to complete a deal before school starts in the fall. This creates a seller’s market in the spring summer and a buyer’s market once school re-opens

Schools is practically over now. It takes 30 to 60 days to close on a house so anyone wanting to move needs to start the process now. The fact sales are down is a bad indicator that housing is in trouble.

The fact that inflation will only go up and keep interest rates high will be the nails in the housing coffin.

you know nothing but post with such confidence. remarkable stupidity.

And you have such poor confidence that your reply is remarkably pedestrian and childish. How are those gas prices working out for ya? Lol!

My first mortgage 30+ years ago was at 10.25%, my second mortgage was at 8.0% and then my third was at 5.75%. So mortgage rates in the 6 to 6.5% range don’t seem horrendously high to me in a long term context. What is horrendously high to me are home prices. I don’t think I could afford to buy today the house I live in. Zillow thinks my house is worth far more than I can believe, but I have no plans to sell, so what that means to me in reality is that my insurance has increased dramatically because my insurance company says that my house is worth so much money and needs to be covered at that amount.

Insurance only cares about the replacement cost, not what you could sell for.

The fact your insurance is up dramatically is because costs of raw materials and labor is up dramatically (I am assuming you aren’t in a fire zone in Cali or a hurricane zone in S/E US states that caused an extra bump in prices).

My son’s A/C just went out. The best quote for a new replacement is $9,400. This for a 2000 sq. ft 3×2. The hardware itself, inside and out, was only $2200 according to the manufacturers website.Two guys will get the job done in about 4 hours. That might add another $600 to the costs.

One company wanted $15k! It’s f*ing sheet metal, a condenser and a couple of fans people!

All new systems have to meet the new environmental standards (effective 2025)….prices doubled as result.

In January 2025, the Environmental Protection Agency (EPA) will enforce new regulations designed to reduce the environmental impact of air conditioning units. Specifically, the EPA is targeting refrigerants with a high Global Warming Potential (GWP). As part of this effort, all newly manufactured HVAC systems will need to use refrigerants with a much lower GWP, such as R-454B or R-32.

We used to live without AC. We can again, soon enough

In a few years only data center will be able to afford A/C.

I’m thinking the new hottest real estate location in the future will be any place that has no data centers within a 200 mile radius.

I warned people about electric rates, some laughed at that and now they are crying.

As long as the Oligarchs make money, people will be happy.

I think more people will as energy costs continue to rise.

Not in Florida.

Amen

I need a new AC unit on my 2nd floor (old one just got a temporary weld repair that’s holding for now on an 11 year old unit). 2nd floor is about 2300 sq ft. The small (ie father/son type thing) A/C company I use wants to put in a 5 ton unit 2 stage unit over the existing 1 stage 4 ton and upgrade the duct work and move the location in the attic to a new location. They quoted me 30K (not a typo) for all the work.

The 2 stage 5 ton unit cost is ~7K (I went online to see the price of what he quoted) with a 10 year warranty (transferable to new home owner which it never was before in Florida so I thank DeSantis for that). All the rest is essentially labor and some duct work.

Obviously I’m getting some other opinions and quotes. I want a 2 stage unit to reduce humidity but am fine with 4 ton and just some slight adjustments to the duct work in a few rooms with poor air flow. That duct labor should be done by 20/hr unskilled guys with just the AC guy overseeing.

Costs are indeed insane.

“Costs are indeed insane.”

But “illegals” cost the country money. Lol. I hope you get the irony of being an advocate for mass deportations and now being stuck with huge labor costs.

This is just the start of your labor troubles. I don’t write “demographic death spiral” here for kicks, I write it so people understand what is coming in the future, you just got a snapshot. Multiply your woes by 10x for plumbing, electrical, carpentry, landscaping, etc.

When the pain gets real, it will click in your brain.

Good luck finding guys to put together ducting (correctly) in attics in FL heat for $20/hour. Many of those hard-working guys have migrated south within the last year. Or moved to CA where they can get that much for minimum wage for running a cash register in an air-conditioned fast food restaurant.

those fast food jobs are getting automated away.

In a few weeks there will be plenty of high school kid labor for these types of jobs. My daughter makes 16/hr as a lifeguard standing in the Florida sun all day. I’m sure for 20/hr you can get a couple high school kids to lay duct work in an attic for a couple of days. Even if it’s 25/hr its still vastly cheaper than 100+ hr rates.

Sounds like an easy solution to your A/C problem. Put out a Craigslist ad and have some high schoolers put in your ductwork.

Easy, peasy, problem solved; it’s the American way

The taco economy continues to “boom.”