Please consider the Fed’s Z1 report on Recent Developments in Household Net Worth and Domestic Nonfinancial Debt.

Hooray for Bubbles!

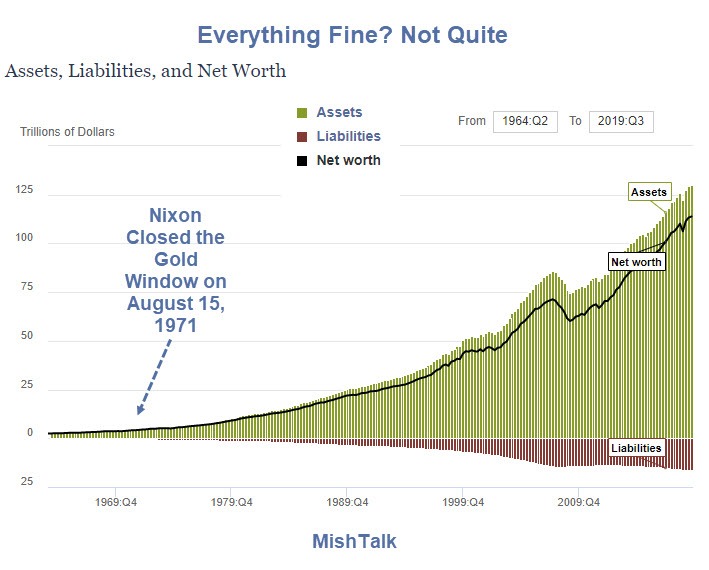

“The net worth of households and nonprofits rose to $113.8 trillion during the third quarter of 2019. The value of directly and indirectly held corporate equities decreased $0.3 trillion and the value of real estate increased $0.2 trillion.”

The Fed offers an Interactive Chart on Wealth.

Assets vs Liabilities

- Assets: $130 Trillion

- Liabilities: 16.4 Trillion

- Net Worth $113.8 Trillion

Aggregates Mislead

Median Net Worth

The average net worth is $347,800. The average net worth of those 18 and older is $448,031.

The median net worth of those 18 and older is about $100,000.

The median net worth is skewed by the biggest stock market bubble in history. It’s also skewed by a housing bubble.

Unlike Elizabeth Warren, I am not proposing wealth redistribution schemes.

Rather I am pointing out problems with the rosy-looking picture.

What the Chart Does Not Say

The chart paints a rosy picture. Liabilities are low. Hooray.

But what the chart does not say is where the wealth is and where the liabilities are.

The assets are concentrated in the hands of the top 10%. The liabilities are concentrated in the bottom 90%.

Bubble Blowing Tactics

Most of the country isn’t prepared for retirement. And many who think they are prepared do so only because of inflated asset prices, unlikely to last.

This is a result of bubble-blowing tactics ongoing for decades. Escalation took off when Nixon closed the Gold Window in 1971.

For discussion, please see Nixon Shock, the Reserve Currency Curse, and a Pending Currency Crisis.

Nixon Shock coupled with irresponsible Fed policies are to blame for widely reported “wealth gaps”.

Meanwhile, if you do not feel wealthy, then most likely it’s because you aren’t.

Addendum

ZeroHedge just provided this pertinent picture.

Mike “Mish” Shedlock

These calculations are basically meaningless. US treasuries are counted as assets but they aren’t listed as liabilities. Thats a ~10 trillion dollar overstatement of wealth held by the top x%. They also value streams of income like SS at nothing. An annual SS payment of $16,000 has no value in terms of wealth, but an annuity that payed $16,000 a year would have a market value in the hundreds of thousands of dollars. The US tax and transfer scheme directly reduces the measured wealth of the lower economic classes and inflates that at the top, followed by cries for even more redistribution.

Wealth calculations in the modern world are bizarre. They forget the value of people, themselves. Much horror has be loosed on the world because of this oversight. But that’s another story.

Let’s run some quick numbers.

The US: 300,000,000+ people. If you low-ball (I say, but YMMV) them all at a million bucks a pop, you get wealth of roughly 300,000,000,000,000. So, that 300+ trill in control of somewhere in the 100+ trill range? Sounds OK.

Take a slightly smaller sample: You. Do you feel like you’re worth 3 times the stuff you own? More? Less? What?

So, is that 100+ trillion out of line?

Let’s ignore those who just fuss about the world being an 80-20 world. They, unlike enlightened statesmen, will always be among us. As the article linked by@Latkes points out, much fuss isn’t about 80-20 or 90-10-ness, it’s about those guys who are a little more 80 than “me”. That’s unfair, I splutter!

Assets depend on their ability to command a stream of income. A shift in technology or demographics can mean formerly valuable estates and capital goods lose their value. Plant the most valuable building in London, Shanghai, or Manhattan in the middle of the Congo, and it’s value will be nought. Former castles in France can be had for next to nothing. Land used to be the basis of capital, because it produced food. Desert was never valuable.

Current valuations are predicated on expected future income growth. If it is not realized, all kinds of people will be forced to sell, many will go bankrupt as the “wealth” evaporates. If there is enough social chaos, the ownership of capital may “redistribute itself”.

Asset valuations imply a prediction about the future. Predictions fail.

I’ve made that same point half a dozen times. Any series of data which increases by a percentage every time period should be shown on a logarithmic scale to have any meaning.

Ah, would that your point would sink in.

But, “have any meaning” —> “not be misleading”. Yep, such graphs have a lot of meaning. It’s just that you don’t want the meaning polluting your mind. 🙂

So you reckon Americans would somehow have managed to rack up $16 trillion in liabilities at $33/oz for Gold? As in, half a trillion ounces of liabilities, despite there only existing between a percent or two as much actual Gold in the entire world?

And ditto “asset values” redeemable for about a thousand times as much Gold as is in existence?

Yes. 🙂 Sure, the numbers would be different. That is to say, the amplifier knob would only go to “11” instead of “11,000”. But how would people be stopped from borrowing and loaning? Government decree?

Two rules apply when considering personal debt:

You can’t “educate” these tendencies out of people. Therefore, the system must be built around these flaws – by making lenders eat their losses. Period! End of story!

Maybe true for most people. I dunno. Neither 1 nor 2 are true for me, personally, so … I do wonder what percentage of people 1 and 2 each cover.

So far, the votes are even. Both are true for you. Neither for me.

Anyone else want to cast a vote for themselves?

In another metric, debt is historically LOW.

https://fred.stlouisfed.org/series/TDSP

This is going to stir the pot

Any generation in its infancy wont hold much wealth. Millenials are lucky. Their grandparents were returning from fighting WWII at their age.

Millennials are certainly not “lucky”. They’re coming of age in a mature ponzi scheme, a rotten place to be.

If anything, in the new gig economy, one needs to make their money while young and attractive, since prolonged employment is becoming a thing of the past pretty much everywhere outside of government.

These things go in cycles. The 1920s were the same ponzi scheme before a decade of depression.

They are living longer.

AND to all of the above it is not like they are somehow separated from Gen X and the babyboomers, all the boomers wealth will go to them eventually, do remember that the boomers were the kids of the generation that got RAPED in the depression like my family, grandfather raised in the lap of luxury till 1930 when the bankers came and gave my great grandmother minutes to load what personal items in the car she could and leave, when her father had built a small regional trading empire of general stores and lumber yards in the Puget Sound area. They drove as far as they could on what money they had, made it to Medford Oregon where my mother was born in 1935. Now I am supposed to feel bad because some 22 year old is pissed about not owning everything he ever will right now today? I know they are attention deprived and very poorly educated but someone needs to tell them how inheritence works, you have to wait for us old bastards to die to get your hands on it.

Who is living longer? Boomers may be, although not by much. We X’ers and future generations are actually living shorter lives. Remember, US life expectancy has been falling since 2014. Obesity is offsetting medical advances, but more importantly suicides and overdoses are driving numbers down.

Herkie, what wealth will they inherit? Most Boomers I know have assets that will tumble when this debt bomb finally blows, if not disappear altogether. My parents are long-retired early Boomers that did well, but if they manage to live another 20 years I expect to receive little or nothing from them. How much will their stock portfolio be worth when this debt bomb finally explodes? Also remember that people are rapidly perfecting the art of separating the elderly from their money with assisted living costs. My aunt’s facility cost more than $10K a month until she died several years ago, and that was in semi-rural Ohio!

“Also remember that people are rapidly perfecting the art of separating the elderly from their money with assisted living costs. ”

Well said!

Like a bunch of nicely suited ruffians waiting outside the casino door, ready to pounce on the winners who are making their final exit. Must grab chips before chips get passed to the kids!

That sucks for them. Boo Hoo.

Still glad Nixon closed the gold window to foreign governments and central banks. Prefer he’d just opened the window to Americans and balanced the budget, but Congress wouldn’t have passed it even if Nixon wanted to.

The bad thing Nixon did about the same time as closing the gold window was imposing wage and price controls. Although most of the controls were lifted by early ’74, politics kept the price controls on (domestically-produced) oil until Reagan. Ford could have lifted them by vetoing a bill to make changes just before the controls expired, but didn’t because the changes were negotiated with Congress by his own energy czar, Frank Zarb.

Nixon forced Arthur Burns to commit to a policy of low interest rates before Nixon nominated him to head the Fed in Nov. 1969. Low interest rates put pressure on the $US vs. gold, the German mark and Japanese yen and eventually forced Nixon to close the gold window.

Census Bureau on Gini Index (Income inequality. Higher number worse):

The Gini index for the United

States from the 2018 ACS (0.485)

was significantly higher than the

2017 ACS estimate (0.482).

Less than 1%. How much does it bobble between other year-pairs? Or between estimates and final values, should these two numbers be such a pair.

Assets are concentrated in the hands of the top 0.1% and the top 10% are getting angry and moving politically to the left.

I read that article a couple weeks ago and I thought it made some very good points. It explains the appeal of Sanders and Warren to the educated and/or affluent but not quite rich. Student loan forgiveness, by definition, is not for working class or poor people that didn’t attend college. It’s a “new left” when college educated people are the beneficiaries of redistribution.

House is paid, no car payments. I work to pay taxes and various insurances. No kidding.

I’m taking the alternate approach: levering up for the Great Devaluation.

Do you mean leveraging?

What exactly?

Wouldn’t leveraging up make more sense if you expected big inflation? Is that what you are expecting? What will be devalued?

I think what he means is buying as much as possible on credit and then not paying it off when then shit hits the fan, like everyone else deep in debt.

That would be a terrible plan. By not paying debt, you would lose the collateral too, most likely with everything you invested in it.

Unless your collateral is worthless, which is unlikely. Only banks can do that.

I think you’re missing the point – the clue is in ‘the great devaluation’. His strategy is to buy real goods with debt and when devaluation comes his debt will be vastly reduced and easy to pay off. Obviously, timing is critical.

No I get that. I just think it’s unlikely to happen like that. A Great deflation will precede any great devaluation. That will wipe him out.

Yes- what TheLege said.

The political winds are blowing for both fiscal and monetary policy to err on the side of too easy. And with the advent of QE, there’s no limit to how easy central banks can get.

We won’t get fiscal austerity or sound money unless there’s a serious inflation problem.

The extreme level of asset inflation we are witnessing is a matter of Fed POLICY and an absolute necessity, given the nature of our debt-based, fiat monetary system.

These over-valued assets provide the collateral that permits the additional borrowing required to keep the “system” going.

Obviously, this cannot go on indefinitely and we are getting close to the end-point, but we should expect asset prices to continue to hyper-inflate until that day comes.