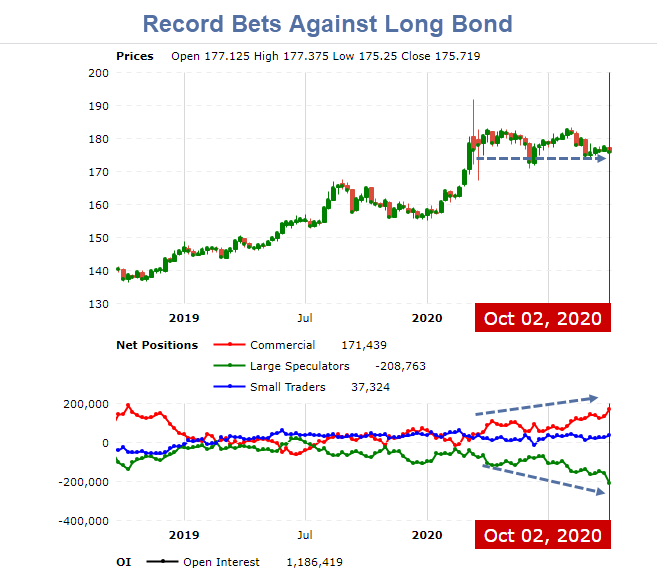

Record Short Position

The Commodity Futures Trading Commission (CFTC) COT report shows Record Bets Against the 30-Year Treasury Bond.

The amount of speculators’ bearish, or short, positions in 30-year Treasury futures exceeded bullish, or long, positions by 230,312 contracts on Oct. 6, a record, according to the CFTC’s latest Commitments of Traders data.

The 30-year yield, which moves inversely to prices, has rallied to a four-month high since August, when Federal Reserve Chair Jerome Powell announced that the central bank would allow periods of higher inflation in order to average its target 2% rate.

Bets on lower bond prices have also been fueled by expectations that the nascent U.S. economic recovery will continue, as investors await an additional round of fiscal stimulus from lawmakers and breakthroughs in the search for a vaccine against COVID-19.

30-Year Long Bond Yield

March 6 Long Bond Position

Treasury Bears Pile On

The 30-year long bond yield is about where it was on March 6.

Yet speculators keep piling on with record bets.

Short Squeeze Coming

Any bit of sustained economic weakness will cause the long bond yield to drop blowing the long bond shorts out of the water.

Mish

Mal-investment (“impacts resource allocation”), stems from the fact that adding indiscriminate and infinite money products (QE-Forever), decreases the real-rate of interest and has a negative economic multiplier. Whereas the activation and discharge of $15 trillion of finite and real-investment targeted savings products (near money substitutes), increases the real-rate of interest, produces higher and firmer nominal rates, and has a positive economic multiplier.

It is much more desirable to promote prosperity by inducing a smooth and continuous flow of monetary savings into real investment (activating frozen savings), than to rely, as we have done c. 1965 (relying on one of its “administered rates”), on a vast expansion of Reserve and commercial bank credit with accompanying inflation to stimulate production (i.e., stagflation).

For the next year or two, as the wreckoning hits, bond shorts will certainly get hurt as Fed buys Treasuries to fund fiscal stimulus. But down the road, thinking next 6-8 years, I think you will see first significant inflation in 4 decades

Are we sure we’ve got 6-8 years left in this social environment? I found Mish and others long ago because I used to focus solely on economic analysis, but lately it seems that social unrest takes precedence. With the Fed printing to the moon, fiscal reality can probably be delayed longer than a social reality where Americans hate each other.

“The pandemic will eventually go away, but the debt will remain. It’s been my view that over-indebtedness ebbs economic growth. Debt is a double-edged sword: It’s increasing current spending in exchange for a decline in future spending unless it generates an income stream to repay principal and interest”. lacy Hunt, august 14, 2020. We van hang this Randy Newman song from 1977 on those words. https://www.youtube.com/watch?v=8bfyS-S-IJs

NBC News correspondent Kelly O’ Donnell posted the waiver that attendees to Trump’s forthcoming events have to agree to. It absolves Trump’s campaign of responsibility if you get Covid at them, a likelihood given that the president and many of his aides were recently diagnosed and are not out of the woods. https://imgur.com/a/thXf7EG

Shorting the long bond has been a popular form of financial suicide for years. It amounts to fighting the Fed…..seldom a wise thing to do.

Technically the 20+ year US treasuries are ready to launch higher anytime soon:

If I understand it correctly, the short sellers are signalling higher mortgage rates (higher yields).

Since the inmates are in charge of the asylum, on a 30-year time scale, it would be wise to short the dollar.

Aren’t many of them short against long positions in physical bonds?

Elliott Wave technical analysis. On the 30 year US bond price chart between August and December 2019 was a clear triangle, which means the pattern off the October 2018 low had one more upward move. That move was a strong rally into the March 2020 highs. Since then a larger triangle has formed during COVID, so the price rally off the October 2018 lows has another major move that should challenge all-time highs.