The number of negative-yield euro-denominated junk bonds reached fourteen, up from zero at the beginning of the year as the ECB prepares still more stimulus.

- Ardagh Packaging Finance plc /Ardagh Holdings USA Inc.

- Altice Luxembourg SA

- Altice France SA

- Axalta Coating Systems LLC

- Constellium NV

- Arena Luxembourg Finance Sarl

- EC Finance Plc

- Nexi Capital SpA

- Nokia Corp.

- LSF10 Wolverine Investments SCA

- Smurfit Kappa Acquisitions ULC

- OI European Group BV

- Becton Dickinson Euro Finance Sarl

- WMG Acquisition Corp.

Illogical Situation

It is illogical for any bond to trade with a negative yield.

Think of it this way: Negative-yield bonds imply it is better to have 99 cents ten years from now than a dollar today.

Yet, there are now 14 junk-rated companies with negative-yield bonds.

Zombification

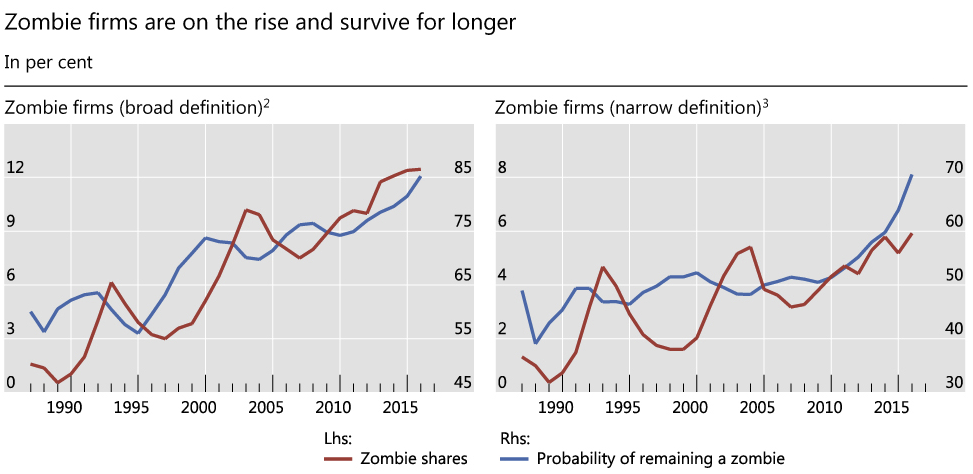

The lead image is from the September 2018 BIS Quarterly review on the Rise of Zombie Firms: Causes and Consequences

The rising number of so-called zombie firms, defined as firms that are unable to cover debt servicing costs from current profits over an extended period, has attracted increasing attention in both academic and policy circles. Using firm-level data on listed firms in 14 advanced economies, we document a ratcheting-up in the prevalence of zombies since the late 1980s. Our analysis suggests that this increase is linked to reduced financial pressure, which in turn seems to reflect in part the effects of lower interest rates. We further find that zombies weigh on economic performance because they are less productive and because their presence lowers investment in and employment at more productive firms.

Yield-Suppression Mistake

This kind of nonsense can only happen with outright central bank intervention suppressing yields.

It’s also extremely counterproductive.

These corporate zombies only stay in business because of cheap rates. That are not productive companies or they would not be on the verge of collapse.

Fundamental Strength of Capitalism

A fundamental strength of capitalism is that failed companies go out of business making way for new ideas and better models.

Yet, here we are. The Fed, ECB, Bank of China, etc., all strive to keep failed companies alive. Zombification is on the rise.

Case for Gold

Due to collective and seriously misguided group-think, central banks are all doing the wrong thing.

The worst part of this story is that a recession has not even hit.

What will these group-think central bankers do then?

This is the case for gold.

Mike “Mish” Shedlock

Mish likes gold, which I like, my avg price is $400/oz, and have recently bought Ag via SLV, and should outperform cash since there are storage costs for holding cash, same as in holding precious metals, and the price of Ag/Au should rise since they tend to do well during deflation. Permanent Portfolio lives. Not to mention that with a new Fed gold bug nominee, “gold is money”. Once people realize money is largely neutral (Fed has not that much power) the curtain is drawn exposing the Wizard of Oz as an old man.

The negative yielding debt isn’t helping zombie companies. They’re still paying the coupon rate. And it may make them worse off since it would cost them more to retire the debt.

Maybe they could refinance.

Doesn’t work the same as a mortgage. They would have to purchase the bonds at above par. I.e. Pay $105 for every $100 they borrowed.

Equity risk is also very real and heightened in these corporate bonds. Not as if that risk has been dodged, in fact increased. You’ll be first in line to receive nothing if site.

Let me ask this: what’s the difference between depositing your money in a bank and paying them a monthly fee to protect it and a negative yield bond? Either way you end up with less money at the end.

FDIC insurance, maybe?

That is the only valid argument for lending at negative rates. In practice, mainly applicable in low security areas and eras, where property rights are poorly protected, theft is rampant, and storage fees at reliable “vaults” are hence very high. (Extra credit for figuring out what that implies about the current West………)

A variation on this, is/was Chinese mining Bitcoin at a known and predictable nominal loss, simply to get at least some of their wealth out of the country.

“Mish – do you know of any serious economist, hedge fund manager, banker, CFO or similar financial professional who has a valid theoretical argument for negative rates? “

Does Trump count?

My obviously silly question serves a purpose, that being bias.

But I do not support rate cuts even though I believe them to be good for my one of my key holdings: gold.

Outside of central bankers, gov’t officials, etc, I have not seen a cease for negative rates.

There is no such case. I do not think it will happen in the US. I could be wrong

If you want a ‘theoretical reason’ (for which there’s likely plenty) Ray Dalio has oft said that “the transfer mechanism [ for the Fed stimulating the economy thru lower rates] nears elimination as rates decline”. (Not his exact verb – but that’s his point.)

Ok, ok, here’s Dalio: “As famed Bridgewater associates founder Ray Dalio puts it, the transfer mechanism breaks down and it becomes like “pushing on a string.””

Some shaman claiming the transfer function of water from the sky approaches zero unless he is paid three virgins to dance a raindance, is hardly a meterological argument for raindancing….

Thanks, Mish. That’s what I feared.

Nobody is making a case for negative rates. Central banks aren’t trying to make yields negative. It’s just a consequence of their buying an enormous amount of bonds.

Negative rates promote zombies by artificially lowering the WACC below what would otherwise be an insufficient ROIC.

Now, onto the bigger US picture. ANYONE w/ eyes open during tech bubble (“Dot.com bubble”) recalls how it was over the top and Greenspan should have at least raised margin requirments to rein in the obvious bubble. (He famously, falsely claimed he had no tools. For which I asked the KC Fed Head why they didn’t and he sucked up to the (false party line). Real estate the same way before GFC. My point is that participants in the bubble MISTAKENLY LOVE THE PUNCH BOWL – BUT LEARN TO HAVE IT EAT THEIR LUNCH WHEN THE BUBBLE BURSTS. Just b/e you like another drink does not mean you should.

THEREFORE, Trump’s Fed Nominee Shelton’s (obvious pandering like Barr did for is job) in “Shelton seemed to be a fan of hard money during the Obama years – accusing the Fed of printing money to finance deficits – but today is calling for rate cuts to “ensure maximum access to capital.” is absolutely assinine, and should disqualify her from nomination. Speaking of “financing deficits”, Trump’s $1 Trillion in new debt deficit every 15 months (mostly for the top ~10% beneficiaries) likewise should contradict her incompetent statements.

Like the other bubbles – FOR WHICH DEBT IS NOW IN ONE – be careful what you wish for. With Interest Expense alone now eclipsing total Defense spending if we pop out of a debt bubble into much higher rates monetary policy will dictate fiscal policy – and we’ll be toast from now until Social Security & Medicare bust as well. (Enjoy that delayed day while you can!)

Mish – do you know of any serious economist, hedge fund manager, banker, CFO or similar financial professional who has a valid theoretical argument for negative rates? I’d love to hear a serious counter argument to what seems insanity. I realize you have issued unanswered challenges. But everything I read says NIRP is nuts. Isn’t there at least non central banker who supports this concept.

Economically, there simply is no valid argument.

Non-economics, weirdo cults; like Keynesianism, monetarism and who knows what; can make up pretty much any argument they want, as they aren’t bound by the strictures of a properly formed, coherent theory. For them, simple curve fitting is more than sufficient “proof.”

It only make sense if Central Banks are desperate to push money into the economy. They aren’t buying as an investment.No one else would buy negative yielding debt.

“there are now 14 junk-rated companies with negative-yield bonds.”

There are now 14 [more] reasons why Draghi / Lagarde are out of credit and out of credibility

Capitalism without bankruptcy is like Christianity without hell.