Compared to the unrevised April number, starts decline 19.7 percent.

Housing Starts Lowest Since May of 2020

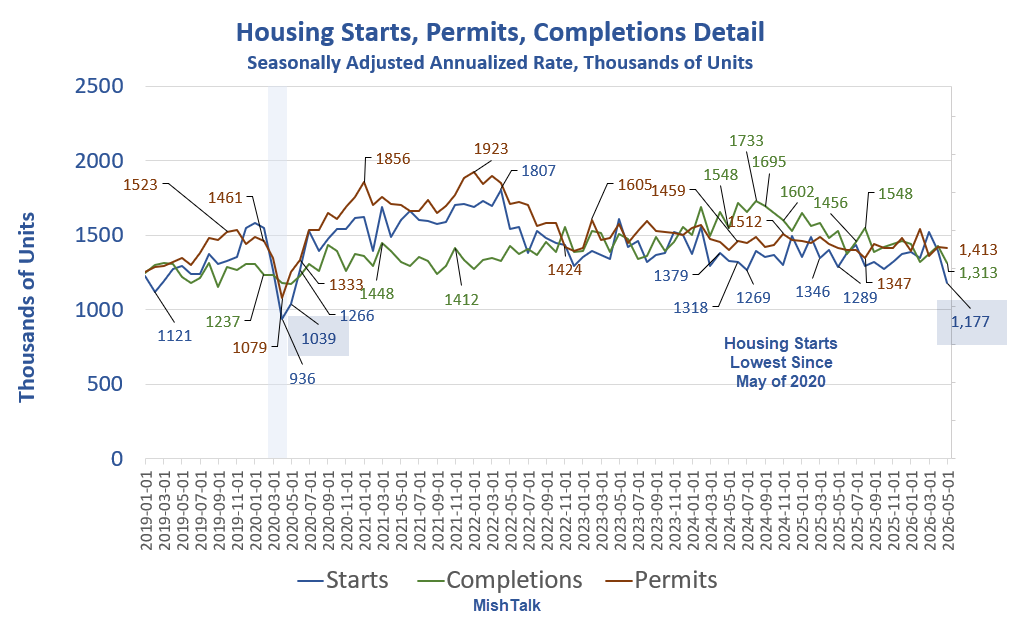

The monthly New Residential Construction report for May 2026 shows a construction disaster.

Housing Starts

- Housing Starts Privately-owned housing starts in May were at a seasonally adjusted annual rate of 1,177,000.

- This is 15.4 percent (±9.8 percent) below the revised April estimate of 1,392,000 and is 8.7 percent (±8.2 percent) below the May 2025 rate of 1,289,000.

- Single-family housing starts in May were at a rate of 882,000; this is 1.9 percent (±10.8 percent) below the revised April figure of 899,000. The May rate for units in buildings with five units or more was 284,000.

Building Permits

- Privately-owned housing units authorized by building permits in May were at a seasonally adjusted annual rate of 1,413,000.

- This is 0.7 percent below the revised April rate of 1,423,000 and is 0.2 percent below the May 2025 rate of 1,416,000.

- Single-family authorizations in May were at a rate of 886,000; this is 0.6 percent above the revised April figure of 881,000. Authorizations of units in buildings with five units or more were at a rate of 474,000 in May.

Housing Completions

- Privately-owned housing completions in May were at a seasonally adjusted annual rate of 1,313,000.

- This is 8.1 percent (±12.3 percent)* below the revised April estimate of 1,429,000 and is 14.2 percent (±11.8 percent) below the May 2025 rate of 1,530,000.

- Single-family housing completions in May were at a rate of 872,000; this is 1.6 percent (±12.8 percent)* below the revised April rate of 886,000. The May rate for units in buildings with five units or more was 426,000.

Housing Starts Single Family vs Multi-Family

Single Family vs Multi-Family Details SA in Thousands

- Total: 1,177

- Single Family: 882

- Multi-Family: 295

The total is the lowest since May of 2020 in the Covid pandemic.

Housing Units Under Construction

Units Under Construction Details

- Total: 1,266

- Multi-Family: 679

- Single-Family: 587

Despite the big decline, there is still a large number of units under construction. But who can afford to buy?

On the surface, this will put price pressure on units as they complete. But many of these are pre-sold, I believe to buyers who will regret buying.

Mortgage Rates

The average 30-year mortgage rate is 6.58 percent, up from 5.99 percent in February according to Mortgage News Daily.

This is not good for either buyers or sellers.

Trump’s tariffs on steel, lumber, and appliances do not help either.

Related Posts

January 30, 2026: Dear Zoomers, Trump Says He “Wants to Drive Up Housing Prices”

Somehow, I doubt Gen Z will like this message.

May 26, 2026: Consumer Credit Stress Is Comparable to the Great Recession

Auto delinquencies are at a new record and credit cards are near record high.

May 31, 2026: Housing Stagnation for Over Three Years in New and Existing Home Sales

New and existing-home sales collapsed in 2022 and have gone nowhere since.

Without a state by state breakout of that number, does not really tell us much, to be honest.

Hosing starts set a new consolidation low from the post Covid peak. That’s the most important piece of data.

If you want to drop prices, you drain reserves. The c. 500b drop in reserves pricked the precious metals market last year.

If you want to reduce nominal interest rates in the long-term market, you drive the banks out of the savings business. Paradoxically, this increases the real rate of interest.

The 1966 Interest Rate Adjustment Act is the paradigm. And it increased bank profits.

I guess Cuba will be the next distraction from the MOU coverup

Good. As housing construction drops, so will material inputs. And producers of those inputs will be forced to compete and cut prices. Eventually, prices will normalize to purchasing power. It’s just going to take a long time.

update on Iran.

I got my call from Iran today. things are getting interesting. I had dismissed a post from a commentator here a few days ago about dissent in Iran between the headliners and moderates but I may have been mistaken.

the followers of the late Supreme Leader are pissed that a deal is in the making and they are taking to the streets to protest. no physical clashes yet but that may happen. You are making deals with the Supreme Leaders blood is there view on the situation.

the speaker of the parliament is for the peace deal, was a prior leader in the IRGC, and is very powerful inside Iran. My friends in Iran expect that he may lead a coup to take control of the government. what that exactly means is unclear.

its a long way till Friday I guess is what im trying to say.

Odd, since Iran clearly won. The US has waived all sanctions against Iran immediately (though temporarily). Iran is already successfully sending tankers through the US blockade (which is temporarily dropped pending successful negotiations.) The oil money will be rolling in. The unfreezing of some Iranian assets immediately, and discussions on a 300 billion reparation fund begins. They still get to control the strait. And nothing has been committed on ballistic missiles or nuclear enrichment. Though this can all still blow up.

it wasn’t what I was expecting when I picked up the phone.

but she said there has been street clashes, not gun battles but throwing objects and fists.

besides that concern if Iran will get the promised money, who in iran will benefit if it happens and what I am hearing in America about the deal.

which is next to nothing. all I know is the 14 points but I told them the fact Trump isnt bragging about the details tells me what I need to know.

no one expects Israel to abide by the plan.

That $300 billion is really closer to $500 billion.

As I’ve stated many times before, the mortgage cost *could* be manageable for most people but what’s not manageable are the ongoing expenses for insurance, maintenance/repair, utilities and other costs that don’t ever go away even when the mortgage is paid off. My niece just had her HVAC go haywire, the house is 10 years old and I told her that HVAC units seem to break every 10 years so put it on your calendar. It’s going to be an expensive replacement no doubt.

I am due for a new HVAC and water heater soon myself, the 10 year mark approaches.

Throw in soaring food costs, soaring healthcare costs, soaring energy (gas/diesel), and the tariff nonsense on top of it all and it’s not sustainable.

Then you got something else…

Do worry, Trump & Walrus will find a way to make things even worse.™

My son just replaced his 14 year old Trane that died. The cheapest replacement was $11,000. One guy was asking $17,000+. Apparently fedgov requires a new coolant which requires a new compressor that is only made in China, and they’re slow-rolling them to the US.

I would not doubt it. Though it seems the techs never want to fix one. Oh never is so much more efficient oh your current ac is to big / or to small for the house.

Its prob easier and more profitable to install a new one. .

How big was his AC unit?

I needed a 4 ton and went with a Daiken Fit seer 17 (the min level to qualify for federal rebate). Got it installed for 8K here in south Florida. It’s a Japanese brand but has a full 10 year warranty and has a good rep. Been very happy with it so far for humidity control.

Of course it’s a heat pump model which is fine in Florida but might not be in colder climates.

Daikin is the world’s largest A/C manufacturer. They own Amana and Goodman.

Housing went down during the GFC because Bernanke held the means-of-payment money supply constant for 4 contiguous years, i.e., total checkable deposits which drove legal reserves down for 29 contiguous months.

But the kicker has gone completely unknown. The transactions velocity of money fell sharply because the ratio of time deposits to demand deposits hit an all-time high. I.e., banks don’t lend deposits. Deposits are the result of lending. Bank held savings have a zero payment’s velocity. See Dr. Philip George’s The Riddle of Money Finally Solved.

That and the FDIC raised transaction deposit insurance to unlimited. That caused disintermediation of the nonbanks.

My anecodotal view of prices at the home center, the “who can afford to buy” might just as easily be stated “who can afford to build”. Now combine the statement. If it’s expensive to build and the risk falls to the builder to its ultimate sale into the “who can afford to buy” crowd, only an insane optimist would be aggressively building.

I now make discretionary choices on what to repair/maintain on my home. Imagine the contractor building homes into this market of higher input costs, higher property taxes, homeowners insurance, mortgate rates and every other living expense…when those that can afford homes are unlikely to come off their 2.5% mortgage they financed 5 years ago and the rest can’t afford to buy.

This situation was all manufactured by the Fed’s artificially low rates and Congress throwing everything at this market for 17 years after the GFC to recapitalize banks and forestall deflation. We needed the clearing of malinvestment and instead we got another decade of it along with the debt. Sad.

Sadder still–they are out of palatable political options so they’ll try to print and spend to prevent any meaningful downturn that could cure the excess.

I continue to be amazed that the top 10-20% carry the economy while the rest of the citizenry puts up with declining standards of living. All while supporting their plutocratic overlords that screw them over in plain sight.

I know ignorance is a powerful force, but the current state of affairs in the US is amazingly unstable

The complicity of a large number of Americans via the designed involvement of the 401k/IRA is the reason it hasn’t turned into an outright revolt. If 56% of Americans own stock and stocks have risen 15+% annually 17 straight years (the math, not the linear nature of the returns), it means many folks not only feel rich but they are rich relative to inflation. I’ve seen it in my peer group. I haven’t been invested to any degree since the GFC and they have…they are all wealthy and they were, like me, just average joe ditch diggers.

If jobs go away before they can access those funds via non-penalized distributions you might see a bit more concern but, if not, a lot of folks have been enriched along with the highest tier.

The USA was always a place where an effort was made to just keep 51% of the proles happy enough to vote with the rich to keep the other 49% down. See Mississippi.

Found on internet:

Societies collapse and empires fall when they no longer have the necessary military/police might to maintain control. If the standard of living for the say 50% of Americans fell to world poverty levels, but the the top 10%, especially the top 1%, maintained their living standards, then the society would continue to churn along with the oligarchs formulating ever more improbable narratives to keep the underfed multitudes disunited, misinformed, and under control. If the “barbarians” never managed to match the effectiveness of Rome’s legions, then the patricians would still be in power to this day, keeping the plebeians in line with evermore variations on the bread and circuses routine.

Of course military might requires an effective economy, but the means to maintain military prowess will be the very last thing that the oligarchs will let lapse.

Of course, the barbarians never managed to match the effectiveness of the Roman legions. They joined them and became officers of the Roman army and did what every top Roman general did: threw a coup and became emperors. When the barbarian general of the Roman army Flavius Odoacer did that, historians called it the “fall” of Rome. But I digress.

Which is why the top 1% keep pushing for robot dogs and robot soldiers. Those never throw a coup and will keep the masses at bay.

I don’t recall any barbarians actually becoming emperors. Rather, the Gothic generals became the powers behind the throne.

The Mockingbird media’s control is broad and uniform. The truth is only available on the fringes, if there.

Wonder how much housing would cost (for real) without the ability to leverage it for 30 years? Same with college educations, car loans, etc?

More “winning”.

O goodie.