Let’s have a fact check on the NAR’s improving affordability claims.

The National Association of Realtors reports Existing-Home Sales Rise 3.2 Percent in May.

“More Americans are on the move, with home sales rising to the highest level since December. This is great news for the housing market and the economy,” said NAR Chief Economist Dr. Lawrence Yun. “Improving affordability is helping drive this momentum. Even with mortgage rates ticking up compared to earlier in the year, they remain lower than a year ago and are essentially at the long-term historical average. Income gains are also outpacing home price growth by a small margin in most parts of the country.”

Affordability Nonsense

“The new record-high May home price reflects solid fundamentals for homeowners and ongoing supply constraints,” Yun said.

So we have record high prices and rising interest rates and Yun yaps about improving affordability.

But that’s what Yun’s measure says “The Housing Affordability Index registered at 105.6, up from 97.5 a year ago.”

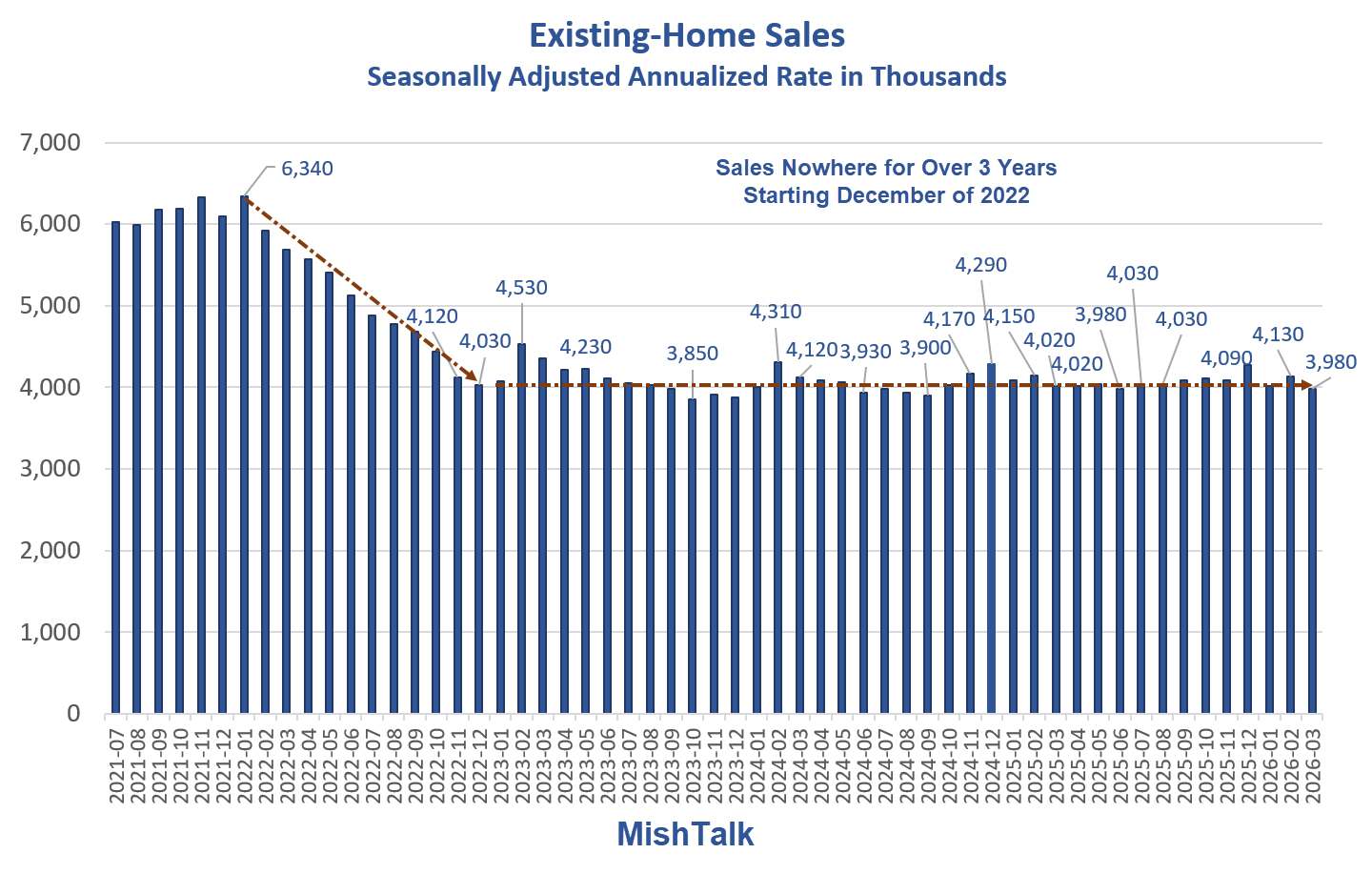

Existing-Home Sales Month-Over-Month

Changes have been essentially trendless for years.

Key March 2026 Statistics

- Sales Month-Over-Month: 3.2% increase in existing-home sales month-over-month.

- Sales Year-Over-Year: 3.2% increase in existing-home sales year-over-year to a seasonally adjusted annual rate of 4.17 million.

- Inventory Units: 1.55 million units: Total housing inventory, up 3.3% from April and up 0.6% from May 2025.

- Inventory Supply: 4.5-month supply of unsold inventory, no change from last month and down slightly from 4.6 months one year ago.

- Median existing-home price:$429,300: Median existing-home price for all housing type.

- 1.3% increase from one year ago ($423,700)—the 35th consecutive month of year-over-year price increases.

- Market Time: 29 days median time on market for properties, down from 32 days last month, up from 27 days in May 2025

Existing-Home Sales Year-Over-Year

Existing Home Sales Supply

The NAR does not seasonally adjust much of its data as evidenced by the above chart.

Nonetheless, we can see rising supply over time. But rising supply has not helped sales.

Existing-Home Sales vs Mortgage Rates

There are sometime jumps in sales when rates drop. However, there has not been any lasting traction.

Sales have basically gone nowhere even as rates fell from 7.62 percent to 6.05 percent.

But rates have risen again. The current Mortgage News Daily rate is 6.68 percent.

MND is more accurate than the Freddie Mac data in my chart because it includes points and fees. I use Freddie Mac data because I have a download from the St. Louis Fed.

The only conclusion is home prices are still too high, mortgage rates are too high, or both.

Synopsis

- Real Income falling

- Home prices rising

- Mortgage rates rising

- Yun claims affordability is improving

Related Posts

May 26, 2026: Consumer Credit Stress Is Comparable to the Great Recession

Auto delinquencies are at a new record and credit cards are near record high.

May 28, 2026: Inflation Expectations Surge in Two Distinct Consumer Confidence Surveys

57% of consumers say high prices are eroding their personal finances.

May 28, 2026: PCE Inflation Spikes Again, Year-Over-Year Highest Since May 2023

Year-over-year PCE inflation jumped to 3.8 percent. The Fed wants 2.0 percent.

June 2, 2026: Trump’s Economic Director Claims Real Incomes Are Going Up

Let’s do a fact check on the administration’s claim.

I gave up on the official statistics many years ago. Having lived in California for decades and having kept an eagle eye on so many pockets for so many years, I came up with my own weird but reliable “housing market barometer”. I simply go onto Redfin (you must be logged in, that matters for some reason) and type in “Clairemont Mesa East”. If there are 17 or fewer properties on the map, then the entire Southern part of America is in a clear seller’s market. If there are 27 or more listings, the entire South is in a buyer’s market (or favoring the buyers more). This measuring stick has worked like a charm for me since Covid and even earlier. Of course, certain pockets and enclaves will always buck the larger trend. Right now, my housing barometer says there is a clear buyer’s market in (Western/Southern) United States (I personally don’t care about the MW and NE, where most suburban homes “skyrocket” from 185K to 230K and everyone pounds their chests).

70% of the 30 listings in Clairemont Mesa East” are condos. Not sure that’s a good barometer of the overall market.

I understand, yet somehow it has been a fantastic indicator for me.

In my little chunk of ca. i watch for sell signs and how long they stay up. Seen the same 5 for about 5 months. Who would want to buy in the hill with fire ins being what it is.

Green shoots!

Ha ha, reminded me of times of bullshit past

The mortgage rate chart clearly shows consolidation behavior before another upward move. If rates move above 6.94 in the next 2 months, chances are the consolidation is over. The trend line drawn would be convincingly broken along with the completion of a complex 3 segment (ABCxABC, double zigzag-zigzag-double zigzag) Elliott wave correction.

I have never been able to see any reliable technical patterns playing out on interest rates. Even with equities, the very best pattern works like 70% of the time. With rates, they seem to be a coin flip at best. Look at how the 30 year note is can’t stay above 5% for long, completely fake (manipulated) moves.

No not meaningful, it’s ALL Trumps fault 🙄

meanwhile North Korea built 10,000 new homes in Pyongyang—more than either Los Angeles or Chicago

https://archive.md/3GvIf

Do they allow the peasantry inside them, or is it like LA?

North Korea’s economy definitely on the rise due to expanded trade with Russia and China (including sending soldiers to fight in Ukraine). WSJ article a few days ago on it, life in Pyongyang from an economic standpoint is undeniably getting much better. Rural areas not so much though.

It’s both. Rates are high and prices are high. Too much money sloshing around from Covid still. Will take till 2030 at least for that to work through the system. If home prices go sideways for 4 more years and inflation runs at 3-4% that would be an effective 15+% drop in prices.

Mish, on another note, curious what you think about the effect of the SpaceX and now OpenAI IPO announcement. Both are for staggering amounts of money (hundreds of billions to 1 trillion) that we’ve never seen before. Unlike the sideline cash myth, these IPOs if they happen at those prices will suck insane amounts of money from somewhere (treasuries, bonds, other stocks, gold, cryptos, real estate?, savings accounts? etc). Do you think it will be evenly distributed or do you think one or more asset classes will take a major dive as people pile into these in hopes of riches (personally I think both aren’t worth much)?

Space based data centers? $22.7 trillion in potential market?

No obvious path to profitability.

Sure thing!!

Those IPO’s are classic bubble top events because of the extreme valuations, extreme size of the companies, and extreme investor enthusiasm.