57% of consumers say high prices are eroding their personal finances.

Record Low Consumer Sentiment

The University of Michigan Consumer Sentiment Index fell to a record low in May.

Sentiment is now just below the previous historical trough seen in June 2022. The cost of living continues to be a first-order concern, with 57% of consumers spontaneously mentioning that high prices were eroding their personal finances, up from 50% last month. Lower-income consumers and those without college degrees posted particularly strong sentiment declines; these groups are more sensitive to increases in the cost of gas and other essentials. Independents and Republicans saw decreases in sentiment, with both groups reaching their lowest readings of the current presidential administration. Meanwhile, sentiment of Democrats was little changed from last month. Critically, consumers appear worried that inflation will increase and proliferate beyond fuel prices, even in the long run.

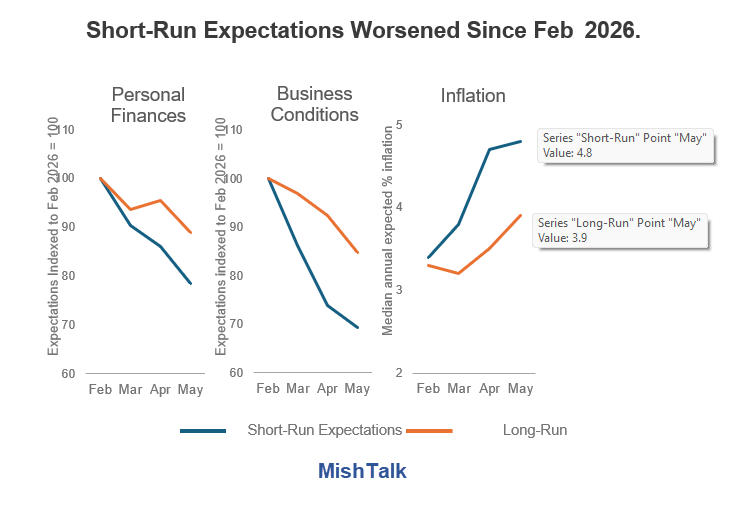

Year-ahead inflation expectations inched up from 4.7% last month to 4.8% this month. The current reading substantially exceeds the 3.4% reading seen in February 2026 prior to the start of the Iran conflict, along with all 2024 readings. Long-run inflation expectations climbed from 3.5% in April to 3.9% in May, notably higher than the 2.8% to 3.2% range seen in 2024. This month’s increase in long-run expectations reflects sizable jumps among independents and Republicans. For the latter group, long-run inflation expectations are currently more than double their February 2025 reading on a monthly basis.

US Consumer Confidence Edged Downward in May

Not to be confused with the University of Michigan survey, the Conference Board reports US Consumer Confidence Edged Downward in May

Conference Board Inflation Expectations

The Median Inflation Expectation is over five percent.

The Average Inflation Expectation is over six percent.

Spending Expectations

- Two-thirds of consumers cited cutting back on spending overall due to rising prices, as of May

- Most who are cutting back bought fewer items and delayed expensive purchases

- Many who said they are delaying purchases of items they want rather than need, plan to buy them in the next six months

- Consumers planned to economize on clothing and footwear, hobby items, and games/toys

Inflation Expectations Don’t Matter

How can they matter?

If you do think they matter, then answer this simple Q&A.

Consumer Inflation Expectations Q&A

- If you think the price of rent will jump next year, will you rent two houses now to beat the rush?

- If you think the price of rent will fall next year, will you hold off renting until rent falls?

- If you think the price of medical care will jump next year, will you have two operations now to beat the rush?

- If you think the price of medical care will fall next year, will you hold off on a needed operation?

- If you think the price of a vacation will jump next year, will you have two vacations this year and none the next?

- If you think the price of a vacation will drop next year, will you have no vacations this year and two the next?

- Will you stop eating? Eat more?

- If you car breaks down will you fix it twice? Wait until next year?

OK, maybe you wait for a sale to buy a coat. But you probably don’t by two. And if your coat rips, and you need one, you may not wait at all.

You can’t do much about electricity bills, home insurance, auto insurance, or gasoline.

Up and down the line there is not a damn thing you can do about 90 percent of what you buy. Rent alone is 35 percent of the CPI.

Fed Study Agrees

No study should be needed to prove the logic of what I just stated. However we do have a study, and it’s by the Fed.

Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?)

Please consider Why Do We Think That Inflation Expectations Matter for Inflation? (And Should We?) by the Federal Reserve.

Mainstream economics is replete with ideas that “everyone knows” to be true, but that are actually arrant nonsense.

The direct evidence for an expected inflation channel was never very strong. Most empirical tests concerned themselves with the proposition that there was no permanent Phillips curve tradeoff, in the sense that the coefficients on lagged inflation in an inflation equation summed to one.

Finally, even if one is willing to entertain the idea that in some vague, mushy sense concern over costs and demand by individual firms facing fixed prices leads to a dependence of aggregate inflation on expected inflation, we are still left with the conclusion that short-run expectations should be the ones that are most important.

One might also be uneasy about policymakers’ relying too heavily on the assumption that inflation’s long-run trend will remain stable going forward so long as measured long-run inflation expectations do. Even if every one of my preceding arguments is judged by the reader to be completely unconvincing, it nevertheless remains the case that we have nothing better than circumstantial evidence for a relationship between long-run expected inflation and inflation’s longrun trend, and no evidence at all about what might be required to keep that trend fixed (beyond that it might involve keeping actual inflation from moving up too much above two percent on a sustained basis).

[Mish note: The lpreceding two paragraphs are a direct criticism of Fed policy as practiced by every Fed chair and people dismiss these reports without reading. The next paragraph is a hoot as well.]

Or would you justify the view that expectations “matter” by pointing to the inflation experience of the 1960s and 1970s, even though that period provides no actual evidence that workers or firms tried to boost their wages or raise their prices in anticipation of future price or cost changes?

Amusing Quotes

- Expectations are by definition a force that that you intuitively feel must be ever present and very important but which somehow you are never allowed to observe directly: R. M. Solow (1979)

- Pure economics has a remarkable way of pulling rabbits out of a hat. It is fascinating to try to discover how the rabbits got in; for those of us who do not believe in magic must be convinced that they got in somehow: J. R. Hicks (1946)

- Don’t interfere with fairy tales if you want to live happily ever after: F. M. Fisher (1984)

- Few things are harder to put up with than the annoyance of a good example: Mark Twain, The Tragedy of Pudd’nhead Wilson (1894

Inflation Expectation Theory and Practice

The widely held view is that if inflation expectations get entrenched prices spiral higher.

It’s a good thing for the Fed they don’t matter because they are getting entrenched.

And note the survey responses. People are trying to spend less. But that hard when prices are going up.

Meanwhile, credit stress mounts.

Related Posts

May 19, 2026: A WSJ Opinion Article Tries to Explain “Why Everything Feels More Expensive”

The WSJ explanation is hugely lacking. Let’s discuss.

May 26, 2026: Consumer Credit Stress Is Comparable to the Great Recession

Auto delinquencies are at a new record and credit cards are near record high.

Don’t worry, as taco will continue to do stupid things to ensure inflation stays elevated.

Did anyone see this story about a CIA employee stealing $40m in gold bars and Rolexes from last November to March?

https://apnews.com/article/cia-gold-bars-theft-arrest-689029ef34d6ccb2bb3aaf3f3cc259f4

-How did an employee have access to so many gold bars and Rolex watches?

-How can US security not notice someone walking out of a government facility with gold bars?

The incompetence of this administration is just unbelievable.

The global oligarchs want more for them and less for everyone else. It appears that humanity simply cannot evolve after all and a new feudal system (this time digital) is being imposed on the planet. Meanwhile in America, what has happened to real investigative journalism, why is no one asking the obvious questions? If everything is fine economically, why is the Fed expanding it’s balance sheet again? The laws of physics and Nature bat last and an economy requires consumable calories to actually work. Print all you want, if those calories are not available for consumption, people die, full stop. It’s 1973 again, this time with 120% DEBT:GDP

Hedge accordingly

Trump went from Mildly entertaining and funny at times, to downright ridiculous. Waging this war will not only cause PRICE inflation but also SHORTAGES. Will it be as bad some past historical moments? Well, let’s explore the WORST moment in history. Hold on:

“Throughout history, some of the most devastating food shortages have been caused not by bad weather, but by the deliberate strategies, economic disruptions, and logistical collapses of war.”

1. 1942–1945: World War II Famines (Global)Estimated Death Toll: 10 million to 14 million people

2. 1932–1933: The Holodomor & Soviet FamineEstimated Death Toll: 5 million to 7 million people (3.5 million to 5 million in Ukraine alone)

3. 1921–1922: The Russian Famine (Russian Civil War)Estimated Death Toll: 5 million people

Following World War I, the Russian Civil War broke out between the Bolshevik “Reds” and the anti-Bolshevik “Whites.” Both sides, but particularly the Bolsheviks under a policy called War Communism, forcibly seized grain from peasants to feed the Red Army and the cities.

….and on and on and this one could happen due to the Hormuz Strait leading to Fertilizer shortages.

THEY WANT THIS. TRUMP is not the cruel creator: he is following orders.

Is it the WEF?

As long as the rich are not unduly inconvenienced, who cares?

Spot on comment!

…and 43% have never been wealthier with real estate, Nasdaq/SP500/Dow, gold, silver….

With some of the 57% actually owning all of the above and still, rightfully, complaining about prices.

Granted, I hate inflation and have said many times it is THE unhappiness creator as it is sourced in uncertainty in its degree, capricious nature of where it lands, how long it may persist, etc…..but this K-shaped economy is massively benefitting a large swath of the population. Still, the pain it is inflicting on its victims, aka the rest of us, and the young who have not yet had a chance to benefit from asset ownership outside of their pending inheritance, should it last, is creating all sorts of problems.

Those MPO45v2 turtles are really stacking up.

You get 1-star Mishelin award for comment.

And you have no idea how bad it is out there.

https://www.cnbc.com/2026/05/28/fidelity-average-401k-balances-q1-2026.html

The average account down 4% when markets are at all time high?

“It’s Trump & Walrus turtles all the way down and inflation all the way up!”

The roaring 20’s were fabulous. Something underlying was wrong and it came to a shuddering halt!!!

PCE 3.3% today. Yikes! Rate cuts? Lol.

https://www.cnbc.com/2026/05/28/core-inflation-hit-an-annual-rate-of-3point3percent-in-april-as-expected-feds-preferred-gauge-shows-.html

Like the factors affecting and about to decimate the private credit market…I have the following observation. We’ve had about 10 years or so of very low interest rates which prompted many people and businesses, including private credit firms, to load up on very low interest debt, mortgages, car loans, extend and pretend etc. However with inflation and elevated asset prices now in place—to control inflation central banks may be forced to further jack up interest rates…which is squeezing consumers and companies now having to pay higher interest rates.Higher 10 year rates, when used in discounted cash flow models, reduces the value analysts determine for all financial assets, Oil price shocks have also been shown to negatively effect stock markets. Too much national debt is also a problem Warsh is having to deal with. I moved all my exposure to gold and other hard assets to protect my purchasing power as a result

LOW interest rates? No, ZERO interest rates for 11 full years from March 2009 to present.

They were only above a whopping 1% for 6+ years over the last 17.

Fed complicity in this bipartisan gutting of the US Treasury to backstop/prop-up anything and everything.

Please. The true goal of the Fed has always been to facilitate the consolidation of power and control through the manipulation of the currency. The Fed has been tremendously successful for its owners. The Fed now OWNS America’s representation and assets.

Price of tomatoes is up 39.7%. That’s terrible news for food affordability *and* public health. Tomatoes are one of the most popular fresh vegetables.

https://x.com/IsabellaMWeber/status/2059594273062805746

The politicians tell us they can lower prices by spending more money. Does anyone believe them?

Only way is via bulk, but they order 1 at a time it seems…

Maybe apply bulk to benefits, and allow the people to manage it for themselves. Eliminates the massive Middle People we shall call them now days, or the cost of doing business as the mob would say. Jan 1 they get the check, no more until Jan 1 the following year. Food for thought, so to speak.

Check out aggregate demand.

Thank You!

– I get the domestic final (like effective more) demand is the total demand for final goods (domestic product?) and services in an economy at a given time. > I want to know Who, and How and Why they set up this scenario, and who is or has been allowed to change it in any way?

– results show that the slope of the curve cannot be mathematically derived from assumptions about individual rational behavior. > So like many things the Taxpayers Pay For, it’s useless information, or selective at best? An agenda within the theory and results perhaps? Not used for anything of value, or shouldn’t be?

I want Facts, Who, Why, Where, and When and Changed and if so, How Often? This sounds like a total waste of Peoples time, cost, energy, and most importantly, Effectiveness!

Not that it shouldn’t be done, but extremely efficiently and effective but only where it makes sense, works, and accomplishes whatever demands are set into place, that it should constantly being challenged on.

Politicians can lower the prices you pay by subsidizing the price by giving money to the producers. The overall price will likely be higher, but you won’t notice, they’ll be lower for you. The deficit will go higher, but no one cares.

It sure looks like the orange man is going to start bombing once the Hajj is over, so this is going to get a lot worse. You oil traders should be loading up

the US is a plutocratic slave plantation with a blackmailed leader so expeditions don’t matter, except to the people who actually have power and for them controlled inflation is beneficial- see S&P

A majority of Americans are now too programmed to see this – but they will wake up at some point but first we have to showcase a

naked man fights on the White House lawn

this is Rome all over again

Caligula (12–41 CE), formally named Gaius Julius Caesar Augustus Germanicus, was the third Roman emperor, ruling from 37 to 41 CE. Nicknamed “Little Boot” by soldiers in his youth, he is infamous for his short, controversial reign marked by alleged megalomania, cruelty, and financial extravagance

“CE” lol

Caligula comes to mind. My Mom, when I was in 5th Grade, MADE me take Latin (Paid off). The best part is that the Latin Teacher LOVED Roman history and taught us MORE about that then Latin itself…. it was the best introduction to past patterns that pay themselves forward to today as mankind is a repeating matrix.

The list of questions is very selective. I have been warning about food costs and I believe they will continue to rise so I have stocked up on reasonable items: beans, rice, tuna, etc. Stuff with very long shelf life. I would not have done this if I did not think food costs would rise.

Before Trump instituted his tariffs in China, you made numerous posts about people “front running” purchases, was this not inflation expectations?

https://mishtalk.com/economics/how-long-will-front-running-tariff-inventories-supply-shelves/

As for vacations, people won’t go on two vacations if they expect them to be more expensive in the future, they will likely take more vacations but shorter ones (long weekend vs 2 weeks).

Bottom line is some behaviors do change. Wife and I went to the grocery store this past Saturday, we were consternating the fact that it’s usually packed on Saturdays and it was empty at noon. Perhaps it was because it was memorial day weekend but I noticed traffic was very light in/out of the city.

We used some in-store coupons and were shocked to have saved $20 on items. I guess even the grocery store is getting desperate for sales.

Had you gone on Friday you might have seen what I saw–every place was as packed as ever on a holiday weekend. There’s been some behavior change but not a significant amount from what I’ve seen. Not enough as there should be. Reminds me of a stock market that isn’t discounting war, elections, inflation, or, frankly, anything any longer other than the value of the dollar!

Bill i think there is a certain age group whos parents have passed. They are the first maybe second or so generation to inherit their parents 401 k. Combined with their own they are doing well.

Whatever happened to all the money? My understanding is that there was/is roughly $200 Billion currently still tied up in litigation from the Tariffs.

A portion of that money, and a very large one at that, is to be refunded to U.S. businesses following a Supreme Court ruling against those tariffs. When?

That’s a boatload of money, and I don’t see or hear it spoken much about. We are talking game changer type of money, are we not? What about DOGE too, as there were Billions found there as well. When?

Lol. Trumped threatened that he would remember the companies that applied for a tariff refund. He’s such a tough guy. 175 billion is subject to refund. 85 billion has been applied for. 20 billion has been paid out. The companies will use that money to try and survive the remainder of the moron’s term in office.

Inflation expectations don’t matter as long as they are anchored. If they get unmoored—as during the 1970s—they become central at the macro level to understanding price and wage setting and financial market behavior. And once there is hyperinflation, the only thing that matters are inflation expectations.

My observation during covid was prices went up. Those who could raised their wages to maintain living standard. Doctors lawyers etc. those with union followed. Eventually every other employer had to compete. Then the fed had to crush demand to slow the cycle.