The ISM price index is the highest since August 2022.

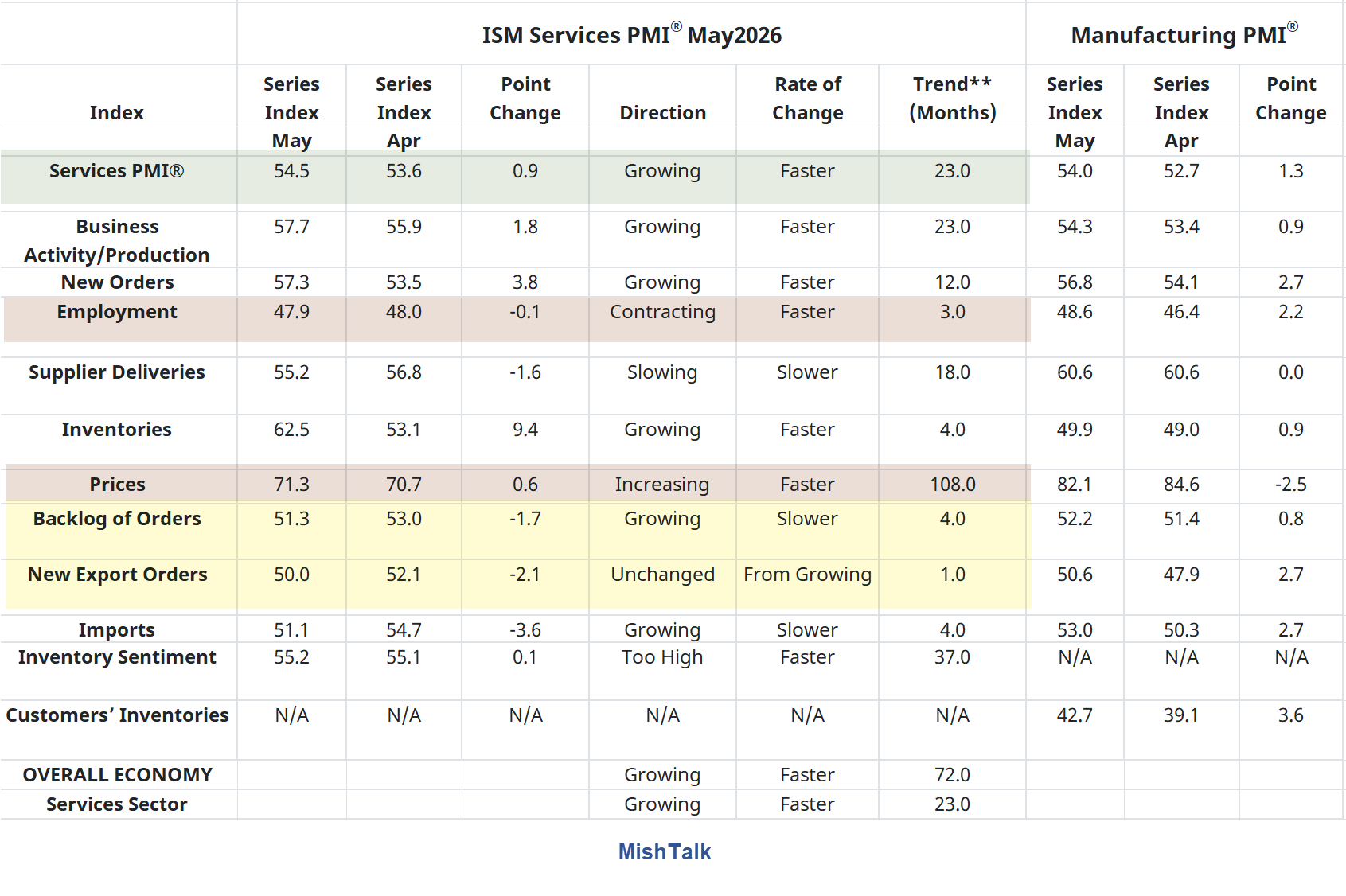

The May 2026 ISM® Services PMI® Report shows production is expanding faster but employment is in negative territory for the third month.

Economic activity in the services sector continued to expand in May, say the nation’s purchasing and supply executives in the latest ISM® Services PMI® Report. The Services PMI® registered 54.5 percent, the 23rd consecutive month in expansion territory.

The report was issued today by Steve Miller, CPSM, CSCP, Chair of the Institute for Supply Management® (ISM®) Services Business Survey Committee: “In May, the Services PMI® registered 54.5 percent, an increase of 0.9 percentage point compared to April’s figure of 53.6 percent. The Business Activity Index remained in expansion territory in May, increasing 1.8 percentage points to 57.7 percent from April’s reading of 55.9 percent. The New Orders Index registered 57.3 percent, 3.8 percentage points above April’s figure of 53.5 percent and 2.6 percentage points higher than its 12-month average reading of 54.7 percent. The Employment Index contracted for the third month in a row with a reading of 47.9 percent, a 0.1-percentage point decrease from the 48 percent recorded in April; of the four subindexes that make up the composite PMI®, it is the only one that remains below its 12-month moving average,” says Miller.

“The Supplier Deliveries Index registered 55.2 percent, 1.6 percentage points lower than the 56.8 percent recorded in April. This is the 18th consecutive month that the index has been in expansion territory, indicating slower supplier delivery performance. (Supplier Deliveries is the only ISM® PMI® Reports index that is inversed; a reading of above 50 percent indicates slower deliveries, which is typical as the economy improves and customer demand increases.)

“The Prices Index increased to 71.3 percent in May, 0.6 percentage point above April’s figure of 70.7 percent and recording its highest reading since August 2022 (72.6 percent). The index has exceeded 60 percent for 18 straight months, increasing its 12-month average from 67.7 percent to 68 percent. Diesel, gasoline, oil and related commodities were once again most frequently mentioned as up in price in May.

Miller continues, “May’s Services PMI® is the fifth month in a row with an increase in the 12-month PMI® average, up 1.1 percentage points from 51.7 percent in December 2025 to its current 52.8 percent. The Prices Index increased to 71.3 percent, its highest reading since August 2022 (72.6 percent). In this month’s report, petroleum-related products were mentioned as a commodity up in price, a dynamic panelists had not yet reported in April. The Supplier Deliveries Index continued to indicate slower performance; while it eased by dropping 1.6 percentage points in May, its reading of 55.2 is still 2.1 points above its 12-month average.

“Business activity hit its second highest reading since achieving the same reading of 57.7 percent in October 2024, and the New Orders and Supplier Deliveries indexes hit their third highest readings in that time frame. The Employment index, however, hit its second lowest reading since September 2025, 0.5 percentage point below its 12-month average. Respondents commented frequently that their companies had instituted hiring freezes or were not backfilling vacated positions, however, most industries reported that they were holding flat in employment month over month. Respondents reporting that new orders were higher than last month most frequently attributed this to seasonality.

“For the third month in a row, no commodities in the report listed as down in price, with multimonth runs of being up in price for aluminum, copper, diesel, gasoline, software licensing and transportation. Although the Inventories index hit its highest level ever, tied with its reading in May 2010, the Inventory Sentiment was only 0.2 percentage point above its 12-month average. Despite the 9.4-percentage point increase in the Inventories Index compared to April, a 0.1 percentage point increase in the Inventory Sentiment Index indicates respondent confidence that business activity will remain strong amid higher costs, so expanding inventories are not of concern.”

What Respondents Are Saying

- “We are seeing the dual effects of the administration’s tariff policy dynamics and the conflict in the Persian Gulf affect our pricing. Suppliers across numerous industries are trying to pass price increases for fuel surcharges and increased input costs for resin-based products and the like. This is the definition of inflationary pressure starting to affect us. We expect significant cost increases to impact us by late second quarter (Q2) and definitely in Q3.” [Accommodation & Food Services]

- “Starting to see increased supply constraints and associated price increases, especially for construction materials and computers like laptops and tablets.” [Educational Services]

- “Patient volumes and activity remain high, employment is steady and supply chains are operating effectively. There are some product lines on allocation as a direct result of the Middle East conflict; however, the current state is manageable. Another concerning factor on the horizon: the current drop-out rate on Affordable Care Act (ACA) health insurance plans after the federal subsidy was eliminated as of January 1. Year-to-date dropout rates are approaching 14 percent, indicating we may be seeing a potential increase in uninsured patients in the foreseeable future. The short-term forecast is cautious optimism.” [Health Care & Social Assistance]

- “The groundwood paper market remains tight. The announced sale of Norpac to International Paper has caused some tightness. We figure intellectual property issues will eventually take Norpac out of the book market. Freight remains expensive, with gas prices and fuel surcharges starting to come through.” [Information]

- “Effective commodity prices (oil) have increased about 20 percent so far in 2026.” [Mining]

- “Due to rising fuel costs, a major distributor has decided to hold freight with resellers until a new contract is negotiated that addresses these increased expenses. Unfortunately, this means there will be delays that will impact our internal projects.” [Public Administration]

- “Supply chain reliability for aviation parts and consumables has generally improved, but volatility in jet fuel prices — driven by geopolitical and logistics disruptions — continues to complicate forecasting and inventory planning. Wage inflation and a tight labor market for skilled personnel are increasing supplier service costs, and growing sustainability expectations are raising demand (and cost) for sustainable aviation fuel, with availability still uneven by region. Overall, conditions are more stable than during the peak of supply chain disruptions, but elevated fuel, labor and sustainability-related costs remain key factors shaping our purchasing strategy and industry outlook.” [Transportation & Warehousing]

- “Inflationary pressures continue to impact pricing in certain categories. General concern over supply continuity due to unprecedented demand continues in the utility space.” [Utilities]

- “Capital expenditure energy projects continue to be delayed or revamped based on macroeconomic factors. Data center power generation projects are driving demand and reducing available inventory across the piping market.” [Wholesale Trade]

That is a nasty set of comments. It’s similar to the ISM manufacturing comments but services are much more important to the economy.

Odds are Kevin Warsh’s first move as Fed chair will be to hike interest rates. That’s certainly not why Trump appointed him Fed chair.

Related Posts

June 3, 2026: How the War in Iran Is Contributing to Soaring Food Prices

Fertilizer, diesel, and natural gas all have an impact on food. The impact first shows up in producer prices, then consumer prices.

May 28, 2026: Inflation Expectations Surge in Two Distinct Consumer Confidence Surveys

57% of consumers say high prices are eroding their personal finances.

May 28, 2026: PCE Inflation Spikes Again, Year-Over-Year Highest Since May 2023

Year-over-year PCE inflation jumped to 3.8 percent. The Fed wants 2.0 percent.

June 2, 2026: Trump’s Economic Director Claims Real Incomes Are Going Up

Let’s do a fact check on the administration’s claim.

American Airlines (AAL) is reportedly suspending routes, including four nonstop flights from American’s Los Angeles International Airport hub, as a result of soaring fuel costs.

The decision to cut the majority of flights to and from California can largely be blamed on a 50% spike in jet fuel prices at Los Angeles International Airport, which reached a high of $15 per gallon. Other carriers have made similar cuts to their California routes including United Airlines (UAL), Air Canada (ACDVF), and Norse Atlantic Airways (NRSAF).

https://www.politico.com/news/2026/06/04/oil-price-spike-white-house-hormuz-00949435

Politico is reporting that energy industry execs have been telling the White House that inventory levels will generate a meaningful spike in prices in a matter of weeks. A source in the White House denies these conversations and further comments suggest the US is “in a position of strength”.

“We’re at dangerously low levels already,” said one industry executive who was granted anonymity to discuss private conversations with the administration. “We have shared those concerns at the highest levels of government about what’s coming in mid-to-late June. … I hope they are paying attention to inventories right now. You’re hitting tank bottom.”

A White House official denied that any senior members of staff have been warned privately by the industry about inventories. “Politico’s anonymous sources are wrong,” the official said.

An Energy Department official said that while the agency remains in regular dialogue with energy industry leaders, there have been “no such discussions” about inventories.

Inflation causes depression.

During the 1970’s inflation shock, it was possible for most households to cope by sending the wife out to work. This time, the only readily available option is to go deeper into debt, which is only a temporary solution. There is a limit to how much debt a household can carry (the private credit crunch shows we are approaching it now) ultimately resulting in a steep, permanent decline in living standards for a large segment of the population.

I don’t think many households sent their wife out to work in the 70s. I was a kid then and my mom worked (teacher) but in my neighborhood only one other mom worked (nurse) while all the rest of the moms (at least 10+) were housewives. During that entire decade not a single one of those housewives ever ‘went to work’ to help cope.

The reason I suspect was that outside of a mortgage and maybe a car (one car, not two), the average household did not have debt. No one had credit cards (business cards yes, personal cards were almost non-existent), no one was paying for 3-5 cell phones, no one was paying for streaming/TV/internet (it was all free over the air TV, cable didn’t arrive till the 80s) and you rarely ate out. Property taxes were also low (no crazy pensions to pay).

My mom went to work, no longer a housewife

Did she have to in order to make ends meet or did she just want to work to earn extra money. There’s obviously a difference.

I know by the early 70s you were in college so that’s why I am asking (unless you had a lot of younger siblings still at home).

My mom did. She was a school teacher. Went from being a part-time substitute to full-time.

If your mom was a part time substitute then she was already working.

She was at least still a most-of-the-time housewife. She would get called in to sub maybe once or twice a week.

I can’t wait for the new Texas Tom’s to open near me. Great fried food and killer prices. 2 large catfish fillets, 3 large chicken tenders(bigger than canes), a huge pile of fries and onion rings AND a drink for $12.49. It’s really 2 meals unless you’re starving. Can’t hardly eat it all.

So what’s everyone else’s excuse for raising prices?

I just checked online. Texas Tom’s “Catfish combo” is now $13.99.

Looks like they’ve raised prices since you just ate there.

Child labor? Perhaps there is a coal mine hiring?

Oh wait….

Oh there’s another option. Switch banks and let everything like cards, phones etc get declined.

My mom worked. Think she made like $5hr as an office supplies clerk. Dad got drunk nearly every night and raised hell about her spending her whole check every week at the grocery store and there was never anything in the house to eat unless you cooked it.

N-gDp is too high for the 2nd qtr. 2026. Atlanta gdpnow’s latest # is 3%. Inflation over 3%

Dr. Philip George’s unified theory in his The Riddle of Money Finally Solved has failed (Alfred Marshall’s “cash balances” approach). It ignores the flight to liquidity. But his observations were correct.

Dr. Leland James Prichard, Ph.D. Economics Chicago 1933, M.S. Statistics, Phi Beta Kappa, said the same thing 40 years earlier but his unified theory that banks don’t lend deposits, still works. The ratio of demand deposits to time deposits has increased during C-19. That has helped propel the economy.

You wonder what Keynes would think of 2 trillion dollar deficits with a 4.3 percent unemployment rate.

I keep hearing banks do not lend deposits but why do banks panic during depositor bank runs? If money is truly fungible, how does one identify from what accounting bucket money is lent if in time of trouble all buckets are at risk to make ends meet?

No bank can make loans – if it does not have a net inflow of funds, a positive balance of payments.

Loans/investments equal deposits in the commercial banking system. Then all outside factors, the inputs and outputs of the banks, increase in currency outstanding, bank capital, reserve bank credit, etc., are offsetting. The only conclusion possible is that the funds were created internally.

See: BANKS DON’T LEND MONEY (youtube.com) Dr. Richard Werner

See: Dr. Philip George’s “The Riddle of Money Finally Solved”

See Steve Keen.

HYPERLINK “http://bit.ly/2GXddnC”

“The fallacy in their thinking is easily demonstrated by looking at the two types of lending – from one non-bank agent to another (Loanable Funds or LF) and by a bank to a non-bank (Bank Originated Money or BOM as an accountant might call it).”

“A “Loanable Funds” loan simply shuffles existing money from one person’s bank account to another: no new money is created (row 1 in Table 2). A “Bank Originated Money” loan creates a new asset for the Bank, and creates new money as well – which the recipient then spends.”

Anyone in their late 70’s or older remembers adulting in the 1970’s. Johnson’s war upset the economy and created a yo-yo effect of inflation and recession. The mess ended with double digit interest rates, inflation and unemployment, only saved by Volcker’s double dip recession in the early 80’s. History repeats or rhymes or whatever.

The Great Inflation was due to the monetization of time deposits, the end of gate keeping restrictions and the conversion of clerical processing to digital processing. The FED also changed its operating mechanism from free reserves to interest rate manipulation. The time frame of the FED’s operations became 24 hours rather than 24 months.

So, the oil shocks were irrelevant. How about closing the gold window and allowing the fed to create money for political points? We can go into what ever detail our ego’s demand, but we also make our posts unreadable.

You think Alan Blinder is correct. But OPEC was irrelevant. The FED increased monetary flows by 33 percent during 73-74 more than validating OPECs administered rates.

During the decade before 1965 the annual compounded rate of increase in our means-of-payment money supply was about 2 per cent. During the same period, the annual transactions velocity of money increased from c. 21 to 31. In ten in-year period since 1964, the money stock grew at an annual compounded rate of c. 6.5 percent and the transactions velocity of money reached an average level of 70 in 1973.

Velocity continued to increase to over 80 during 1974. Both money and velocity figures were taken directly from the Federal Reserve Bulletin. The impact of both an accelerated increase in the volume and velocity of money on prices is made even more evident if the rate of increase in aggregate monetary demand (money time’s velocity) is examined.

During the decade ending in 1964, money flows increased at an annual compounded rate of about 6 percent. In the nine years since 1964, the increase was more than 13 per cent, and in 1972-73, nearly 30 percent. Because R-gDp and presumably, the volume of goods and services offered in the markets, was increasing at a rate of less than 5 per cent, it should have been no surprise that there was an intensification of our chronic rates of inflation to devastating levels.

If the FED doesn’t validate the administered prices, the administrative price increase is deflationary.

The so-called legal link to gold, or the “gold standard”, prior to the “gold cover” bill of March 19, 1968, was fictional, the economic tie tenuous, and its protection was another myth.

For example, in April 1933 we nationalized gold, made the dollar inconvertible, and by administrative fiat capriciously raised the dollar price of gold in a series of steps from $20.67 to $35 per ounce. All of this was done even though we were a creditor nation and had a chronic surplus in our balance of payments.

Two principal factors were responsible for the origin of the E-D banking system (for the drop in the value of the U.S. $);

(1) the possession by foreign commercial banks of an excess volume of short-term claims against the U.S. dollar, and (2) the preeminence (at that time) of the U.S. dollar as the reserve, standard-of-value, and transactions currency of the world.

Beginning in 1950 the U.S. incurred the first of a chronic series of net liquidity deficits in its balance of payments. These deficits have grown in magnitude and continued uninterrupted ever since 1950 with the exception of 1957 (and they were entirely the result of the Pentagon’s military bases and communist containment wars).

By the mid sixties foreign banks had acquired more dollar balances than were required to cover their own international transaction needs – so they started lending their excess U.S. dollar balances (destroying the $’s value).

What bullshit

Look up Nixon Shock

Search my blog for it

The Korean War, which began in June, 1950, initiated the chronic balance of payments deficits that persist to this time and which will probably continue as long as foreigners are willing to increase their net investments in this country.

The U.S. has had a net liquidity deficit in every year since 1950 (with the exception of 1957), Up to 1976 (when the private sector contributed its first trade deficit ) these deficits were entirely the consequence of excessive U.S. government unilateral transfers to foreigners (re: foreign policy – solely our far flung military bases and personnel).

During all this time the private sector was running a surplus in all accounts: merchandise, services and financial. The Vietnam Ten-year War administered the coup d’etat to our gold bullion standard. By 1968, in an effort to keep the dollar at the $35 par, we had exhausted nearly two thirds of our monetary gold stocks, or approximately 700 million ounces to about 260 million ounces.

Although the dollar ceased to be freely convertible in March, 1968, institutional (central bank practices) and attitudinal lags were sufficient to offset, until late 1970, the excessive expansion in the supply of dollars. In August 1971, all convertibility was ended.

See: “The Case of the Missing Money” STEPHEN M. GOLDFELD Princeton University

See: Velocity: Money’s Second Dimension – By. Bryon Higgins

“Money has a ‘second dimension’’, namely, velocity . . .. ” Arthur F. Burns in Congressional Testimony.

See: “Quantity leads and velocity follows” Cit. Dying of Money -By Jens O. Parsson

c. 1963: “If, in due course, it is decided to follow an easier (or less restrictive) monetary policy, this is presumably undertaken to counteract recessionary tendencies in the economy”…”it must be presumed that the growth of time deposits could not induce a shift toward a relaxation of monetary restraints unless such growth has a dampening effect on the economy, a not unlikely possibility since savings held in the form of time deposits are lost to investment (and to any other type expenditure) , so long as they are so held”…”but we know this: a by-product must be a large dosage of new money in the economy.” — Dr. Leland James Pritchard, Ph.D. Economics, Chicago 1933, M.S. statistics Syracuse, Phi Beta Kappa

I read it.

The Gold Cover, Joseph C. Ramage, HYPERLINK “https://fraser.stlouisfed.org/” \t “_blank”Monthly Review of the Federal Reserve Bank of Richmond, July 1968, pages 8 – 10

HYPERLINK “https://nationalinterest.org/feature/who-really-killed-the-gold-standard-12435”Who Really Killed the Gold Standard? | The National Interest

Additionally, there was a change in banking regulation that took place, IIRC, in 1974. Before then, a bank could take only one income into account in deciding whether to extend a mortgage loan. A second income was considered “temporary”, as if the either spouse lost their job, the family’s ability to service the loan was called into question.

After the change, the bank could take two incomes into account. The upshot of this change was that both spouses had to work to afford a home in a semi-decent school district, because they were competing with two income families. (This is also one reason why the prices of residential housing soared in the 1970s, as there was more money available to chase real estate.)

For those of us who are not feral cats or hedge fund billionaires, anything else was like bringing a knife to a gunfight.

This rather obscure change in regulation went almost unnoticed at the time. But it probably had more real world impact on the average frustrated American family than all the Supreme Court decisions ever handed down. We can argue later whether the change was a good thing or not. At this point, good luck getting that genie back into the bottle.

It was a simple matter of 2 incomes > 1 income. So families with 2 spouses working could simply outbid families with 1 spouse who worked for prime real estate (good schools, lower crime areas etc). That meant either 1 high income earner or 2 earners was needed if your family wanted to get ahead.

The change in Banking regulation didn’t cause the problem at all. It came after 2 incomes started to become more prevalent.

No. Two incomes may be greater than one income, but banks were not allowed to take two incomes into account when making a mortgage credit decision.

So the family might as well as had one income, as far as the bank and FDIC were concerned.

The expansion of two income families came after the change in FDIC regulation.

That may be true about what banks were doing but it didn’t really matter at all in terms of home prices soaring. They soared because 2 incomes had more money to spend and thus were able to bid up housing.

I know this because I grew up in Canada and prices soared there too (my parents bought their 1st home in 66 for 14500 and sold in 78 for 44900 which is 3x appreciation in 12 years which is WAY more than what happened in the last 12 years today) without the FDIC since that doesn’t exist in Canada.

How did any of the above affect the average family (Note: clerical replaced by digital didn’t really get going till the 80s and 90s) back then? The only thing people had in those days was a mortgage, no other debt (maybe a car loan) and no average person owned stocks etc.

You talk about 1965 and earlier below but 1970 is the start of things going bad price wise. I was a kid then a comic book price (and hockey cards + candy/soda) was what I noticed. In 1970 comics cost 10 cents and had cost 10 cents for decades (back to the 40s) so no inflation cost had happened there for a very long time. But the price went to 12 cents then 15 then 20 then 25 then 30 and finally 35 by the time 1980 rolled around. That’s 250% inflation in 10 years after nothing for decades.

I said not a word about 1965 or earlier.

This was a comment to Spencer, not you.

One cause was as you say Johnson’s war but also his great society legislation that led to fiscal outlays exceeding the country’s ability to pay. Foreign central banks realized this would be a strain on dollar purchasing power and started converting dollars to gold at a rate that made government officials nervous. Rather than government fixing the spending problem, Nixon ‘temporarily’ closed the gold convertibility option removing fiscal spending discipline. That was the first gimmick if one does not count gold confiscation and devaluing during the depression. No fiscal discipline leading to unrestrained borrowing is the root cause. The oil embargo shocks was a painful supply chain problem that in time went away, addictive excessive spending continued and inflation at about 4% in the early 70’s was ‘so bad’ Nixon imposed price controls that included goods, services and labor but excluded ‘new’ crude oil. It was a mess to administer and did not work because the root spending problem was not addressed.

Inflation got really bad around 1980 and Volker stepped in with very tight money and resulting economic contraction during the first Reagan administration to get the issue under control, but again the excessive spending problem was not addressed, so in time things only got worse, exacerbated by the fed cutting interest rates every time a problem, real or perceived, raised its head which encouraged more borrowing by continuously lowering the servicing cost. Basically, we have a tax, spend, and borrowing problem that will not be fixed with more taxing, spending and borrowing or holding interest rates below free market price discovery rates. If we as a country do not address the problem, the market will in its brutal way.

unfortunately the issue now is moral hazard in all things whereby TPTB refuse to accept bad outcomes and instead backstop bad actions, investment, behaviour.

they simply have refused to allow a recession to occur despite all the ingredients that should have guaranteed one. we are 50 years into this printed-money regime and 2008/9 left a bad taste AND demonstrated how far they could push legal and illegal financial limits/wranglings to avoid them in the future.

sad because, although recessions are painful they are necessary to clear out malinvestment, bubbles, bad financial actors and the politicians that created the environment for all of it to exist. it’s the latter part that reinforces it all for, if the economy were allowed to operate, if markets were still allowed to reward AND PUNISH, proper discounting would occur.

now, not so much. stocks ATH along with the prices of everything.

even us gen x’ers recall living as children through the angst and inflation of the late 70’s. you become tougher when pain imparts lessons even if you see it mostly in how your parents lived.

108 straight months of inflation reported in the ISM services report is embarrassing.

Never mind, i see what you’re saying here. Still not sure the war was Johnson’s, although he certainly escalated it.

The US defaulted the first time and refused to return gold to Arabs and the French. Inevitably the US is always no good for the money and renegs on the contract. Then goes to war over and over again. A sad country with no direction.

So interest rates have to go up as economy rolls over and the US becomes more insolvent.

And Paul Volcker’s operating procedure Volcker targeted non-borrowed reserves (@$18.174b 4/1/1980) when at times there were over (@$44.88b) in total reserves. And total legal reserves increased at a 17% annual rate of change in 1980.