“I did not have this on my bingo card,” quipped John Mauldin.

Shootout at the Inflation Corral

Lacy Hunt has seen enough. But others, including Danielle DiMartino Booth, haven’t.

Mauldin’s reflections stem from his recent Strategic Investment Conference (SIC) where he was shocked to learn Lacy reversed course on bond yields.

Mauldin discusses the bond market bulls and bears in his latest “Frontline Thoughts” newsletter, Shootout at the Inflation Corral

I Felt the Earth Move under My Feet

I think everyone knows that Dr. Lacy Hunt has been a bond bull for 44 years. He turned bullish on bonds as Paul Volcker started raising rates in the early 80s and has stuck to it over time and it is up until recently been the right call. The funds he managed at Hoisington have been the top performing funds off and on for decades. Not so much in the last few years.

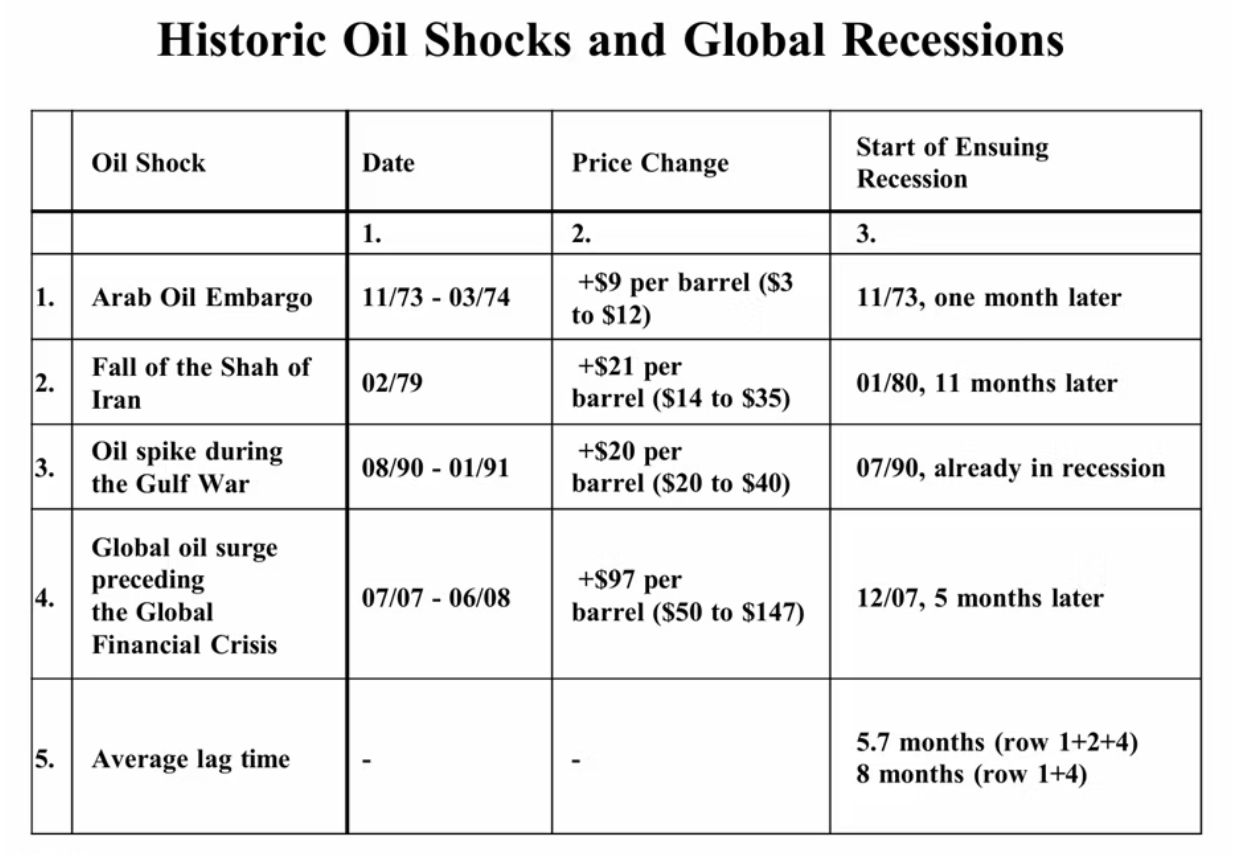

So… 30 minutes before the presentation, I get a note from Lacy basically saying, “I just want you to know that I am going to be making the case for a rise in long-term interest rates.” That started some internal text messaging with my team because this was not on my bingo card. A major 180° change after 44 years? He had two basic reasons, one that everyone is aware of (the oil price shock) and the other was a significant problematic change in Fed policy. When Lacy Hunt starts talking about higher long-term interest rates you have to pay attention. Let’s start with oil first.

By Lacy Hunt’s math, oil prices directly and indirectly account for roughly 12–15% of CPI. If oil prices settle even 20% higher than pre-war levels after the Strait eventually reopens—and I have no particular reason to question Lacy’s arithmetic—that alone could add roughly 240–300 basis points to the price level. Our price shocks have had significant negative effects on the economy.

That inflation pressure is not insignificant, to say the least. Of course, that’s before demand destruction even enters the equation. But the oil shock didn’t arrive in an otherwise clean system. And therein lies the rub…

Starting in mid-December, the Jerome Powell led Fed began purchasing roughly $40 billion a month in Treasury bills, lifting holdings from just under $200 billion to nearly $430 billion by late April.

Impact of Fed Driven Liquidity Impulse

The Fed framed this as a technical liquidity or “plumbing” operation.

Lacy sees that explanation very differently.

“The Fed said that they were upping the bill purchases because the banks were short of liquidity, and this was a technical operation. Nothing could be further from the truth. This was not a plumbing issue. If the banks were in dire need of liquidity… the bulk of those purchases would have gone into idle balances, but they were not. They were directly used and explosively sold.”

I remember asking Lacy and a few others over the last decade why the massive QE and liquidity expansion after the Great Recession didn’t result in an explosion of loans and other bank activities. Partially, it was because the demand wasn’t there and partially the banks were repairing their balance sheets from the aftermath of The Great Recession. That has changed.

This is the part of Lacy’s presentation I kept coming back to afterward.

“In essence, what the Fed did starting in mid-December is they actually were reversing the elements that had been previously pushing the inflation rate generally downward. So now we have the issue of not only solving the oil shock, but we have to unwind the Fed balance sheet as well.” (Emphasis mine.)

I asked Lacy in the Q&A why a 5% move in the Fed balance sheet made a difference. Part of it is answered in this next chart, as it is what is in the balance sheet that makes a difference. They are partially moving from longer-term debt to shorter-term debt.

Federal Reserve holding of Treasury Bills

You can see why Lacy thinks this changes the arithmetic rather dramatically.

His inflation outlook is fairly blunt: inflation will climb above 4%, with periods that could push closer to 5% or even 5.5%!!! That’s a very different world than the one investors got used to after 2008. The historical parallel Lacy reaches for is Arthur Burns easing monetary policy into the 1973–74 oil shock, which he views as one of the great policy mistakes of the modern era. The difference this time, in Lacy’s view, is that the Fed began easing conditions before the oil shock fully arrived.

(By the way, I asked Lacy off-line if he agreed with me that Jerome Powell has been the worst Federal Reserve chair since Arthur Burns. He said yes and then said why. A number of other speakers said the same thing to me, but I don’t have their permission this morning to mention their names, but I will try to. If it was just this one mistake, I wouldn’t say that. But his disastrous handling of monetary policy during and after Covid, his 2019 debacle and other various misadventures didn’t speak well for his tenure. I am sure he is a very nice man, educated and thoughtful. But his core understanding of the mechanics of monetary policy and the outcome from his choices leaves something very lacking.

In future letters about this SIC, we will talk about the extraordinarily difficult situation that Kevin Warsh finds himself in as he begins his tenure as Fed chair. I can’t recall a time since Volcker that a Fed chair came into his position with such extreme externalities. If Lacy is right and we see 4.5% or 5% inflation, how can he cut? We will get to that when we talk about interest rates and Fed policy in a later letter.)

Fog Beneath the Surface

David Rosenberg was our leadoff hitter this year (as he has been for almost 20 years) with a presentation titled The Fog of War, though he quickly moved beyond the war itself. In Rosie’s view, what mattered more was oil, and beyond that the economic and financial imbalances already embedded in the system before the conflict even began. Rosie offers a somewhat different view on inflation.

Rosie’s not an inflationista. In his view, the larger danger is recession, not inflation. He pointed out that inflation lingered in 2021–22 because workers had real bargaining power and wages could chase prices higher. That mechanism, he believes, is largely missing today. Several of his charts suggested the labor market may be softening faster than many appreciate, with unemployment expectations already approaching recessionary territory.

Rosie then turned to productivity, which I think is one of the more interesting parts of his framework.

“In the past two years, 92% of the economic growth in the US economy came from productivity. 8% came from labor input… In any given year, what is normal? What is normal is that there’s an even split, 50/50… At those technology peaks, it’s 70% productivity, 30% labor input. This is 92 to 8. How does anybody think that 92% contribution to the economy of productivity… is inflationary?”

He also spent time on the shelter story, which in Rosie’s view still doesn’t get enough attention. Shelter costs, including rents and owners’ equivalent rent, make up roughly 30% of CPI and nearly 40% of core CPI. Real-time housing data already show new lease rents falling, vacancy rates near cycle highs, and home prices cooling.

The problem is that the BLS shelter calculation lags reality by 12–18 months. That means the disinflationary impulse is still slowly working its way into the official inflation data and should continue doing so for some time.

Finally, before the war introduced a new oil shock into the equation, Rosie pointed to the Dallas Fed’s trimmed mean PCE as evidence the inflation problem was already beginning to solve itself. Both the 12-month and 6-month trends were already moving steadily back toward 2%.

As Rosie put it:

“Here’s Warsh’s favorite inflation metric. The underlying-underlying trimmed mean 12-month PCE, the six-month trend, they’re already heading back down to 2% before the war started.”

Revisions, Revisions, Revisions

Danielle DiMartino Booth thinks we should probably stop talking about recession entirely in the future tense. In her reading of the revised data, the US economy may already be in one.

The BLS initially reported 1.7 million jobs created in 2025. After revisions and quarterly census adjustments, that number fell to just 123,000. In Danielle’s framing, eleven out of every twelve reported jobs effectively disappeared. That should probably get more attention than it does.

More importantly, beneath the headline numbers, the private sector posted net job losses in both the second and third quarters of the year.

“You do not have two consecutive quarters of job losses — and this is the hardest data that exists — without the United States economy being in recession. Mark my words.”

Danielle also pointed to consumer data that increasingly tell the same story: flat real retail sales, a depleted savings rate, and growing use of buy-now-pay-later financing not for discretionary purchases, but for utility bills and dental work.

You can see why she believes the Fed is drifting toward an uncomfortable corner. Layer a five-sigma gasoline CPI shock on top of an already weakening consumer, and Danielle sees a central bank trapped between inflation it cannot really fix and a recession it still refuses to acknowledge.

Middle Ground

Let me briefly touch on Barry Habib’s inflation framework as well. Barry has won four out of the last seven Crystal Ball awards from Zillow for the most accurate mortgage interest rate predictions out of 150 economists and has always been in the top five.

Barry’s view is that oil matters and matters a lot. Tariffs matter too, but more as a one-time price adjustment than a permanently compounding inflation cycle.

As he put it:

“Inflation looks like a staircase. One on top of another, every year, higher, higher, higher. Tariffs are different. A tariff is a one-time price adjustment. It’s like one step and it stops.”

Most of the tariffs were imposed last summer, so as those year-over-year comparisons begin rolling off, they eventually become disinflationary mathematically.

He also pointed back to shelter, which still makes up roughly 44% of core CPI and is measured using a BLS methodology that has barely changed since the mid-1980s. Barry believes real-time shelter inflation is running closer to 1% while the official data still shows something closer to 3%. If Barry is right, official inflation data may still be materially overstating real-time shelter inflation. That lag alone should continue pulling reported inflation lower over the coming months regardless of what happens with oil prices.

Thus, his government-calculated CPI inflation forecast is between 3.2% and 3.5%. He would agree that CPI might not be the best measure of inflation, but it’s what we pay attention to. And he has a pretty good track record of forecasting that number.

Mish’s Take

Welcome to the club Lacy.

Things have changed. I have been discussing this for quite some time. I don’t fault Lacy for a late change. I credit him for not clinging to a view he now believes is wrong.

When you have a firm position for 44 years, it is very difficult to make a change.

Yogi Berra famously said: “It’s tough to make predictions, especially about the future.”

I have had several bad recession call predictions. I will have more bad predictions.

The Recession Club

I was fully in DiMartino Booth’s recession camp a couple years back. But when the data changed I changed my call.

Although I thought recession was coming, I was no longer willing to make that call for the near term. That was the right view and it’s still my view.

The question now is not whether there will be a recession, but when and what kind.

For eight months or so, I have been pondering stagflation. Booth still sees a disinflationary recession.

I am still open minded, but things look increasingly stagflationary to me, and have all year. I also take clues from the bond market itself.

The long bond at 19-year highs should make everyone stand up and take notice.

The Shelter Factor

Barry Habib says “real-time shelter inflation is running closer to 1% while the official data still shows something closer to 3%.”

Rosie says “The problem is that the BLS shelter calculation lags reality by 12–18 months.”

Mish says, “Sorry Rosie, time has expired!”

And alleged “real time measures” are flawed. Truflation makes the same mistake.

Only 10 percent of people move each year, and real-time measures overweight new contracts vs existing contracts.

Two Reasons the CPI Report Will Give the Fed Severe Headaches

I discussed shelter on May 13, 2026 in my post Two Reasons the CPI Report Will Give the Fed Severe Headaches

There are two very troubling aspects of the latest BLS CPI report. Did you spot them?

Month-Over-Month Shelter Percent Change

- Shelter: 0.61 percent

- Owners’ Equivalent Rent: 0.53 percent

- Rent of Primary Residence: 0.55 percent

Those are all hot numbers. More importantly, the disinflationary trend in shelter appears to be over.

Take Rosie’s 18-month lag. The month-over-month peak was in August of 2022.

CPI Year-Over-Year Shelter

Shelter Year-Over-Year Percent Change Shelter

- CPI: 3.8 percent

- Shelter: 3.3 percent

- Owner’s Equivalent Rent: 3.3 percent

- Rent of Primary Residence: 2.8 percent

“If Barry is right, official inflation data may still be materially overstating real-time shelter inflation,” says Mauldin

But what if I am right that the 18-month lag is over.

Shelter Comparisons Looking Ahead

Looking ahead, the year-over year shelter component will depend on the month-over-month number a year ago.

If I am in the ballpark, shelter is going to be adding to year-over-year CPI inflation, perhaps substantially.

If the bond bulls are right, things are at best neutral.

* Key BLS Methods for Rent of Primary Residence and OER

- October 2025: Full rent/OER survey collection was suspended. BLS applied the carry-forward method: Rents were carried forward from the April 2025 panel (the last collected data for that rotating 6-month sample). This produced completely unchanged index levels for rent and OER in October (effectively 0% price change imputed).

- November 2025: Collection resumed mid-November (Nov 14–30).

November indexes used actual collected November rent data where available.

For the 1-month price change (applied to the flat October level): BLS estimated it as the sixth root of the 6-month price change (May 2025–November 2025) from the November-collected sample. This was then used to set the November index level off the carried-forward October value.

Shelter rose only ~0.2% over the two months Sept–Nov 2025 — one of the weakest readings in years outside major crises. This made shelter/OER appear to flatline or decelerate sharply, with the October zero-imputation “anchoring” the numbers lower.

The Tariff Stairstep

“Inflation looks like a staircase. One on top of another, every year, higher, higher, higher. Tariffs are different. A tariff is a one-time price adjustment. It’s like one step and it stops,” says Habib.

Q: Does that sound plausible?

A: Yes. It “sounds” plausible.

The problem is Trump replaced reciprocal tariffs with tariffs broad-based aluminum, steel, and other tariffs that are even worse.

Trump was twice rebuffed by the courts, fist on reciprocal tariffs and a second time on Section 122 tariffs.

Trump will eventually get his way with section 301 tariffs.

Trump Slams Supreme Court, Orders New 10 Percent Tariffs. How Easy Is That?

On February 20, 2026, I commented Trump Slams Supreme Court, Orders New 10 Percent Tariffs. How Easy Is That?

Trump has seven other tariff options. What are they?

Section 122 tariffs went down the drain on May 7, as predicted. See Trade Court Sends Trump’s Section 122 Tariffs Down the Drain

Gee, I get another Tariff “I Told You So.”

But ultimately, Trump will turn to section 301 tariffs.

So, I don’t accept this one-time view of tariff inflation because Trump is hell bent on making matters worse.

Let’s now discuss jobs.

Manufacturing Is the Biggest Net Loser in Jobs, 5 Quarters Total

Please consider Manufacturing Is the Biggest Net Loser in Jobs, 5 Quarters Total

Education and Health Services was the only sector to gain jobs in every quarter. It took a massive 862,000 net gain to hold the overall net total barely positive at 94,000.

On average, that is 18,800 jobs per quarter, only 6,267 jobs per month on average.

Manufacturing, and Professional and Business Services are the only sectors that lost jobs every quarter.

BED Manufacturing Jobs Gains and Losses by Quarter Details

- 2024 Q3: -79,000

- 2024 Q4: -55,000

- 2025 Q1: -37,000

- 2025 Q2: -69,000

- 2025 Q3: -100,000

In contrast to monthly jobs reports, this lagging data is very accurate.

Were it not for AI and boomer health care, this economy would be in the gutter.

So, I certainly agree with Booth about job weakness. Demand destruction will follow, eventually.

Meanwhile, inflation pressures are up across the board, much more so than jobs to the downside.

Trump Twice Says American’s Financial Situations Don’t Matter

That tells you what you need to know about the war, tariffs, and inflation.

Regarding Quantitative Tightening

I agree with Warsh on QT. But he only gets one vote.

I do not expect a policy change soon. So, pay attention to what Lacy is saying here.

Trimmed Mean Inflation TMI

As for trimmed mean inflation TMI that Warsh proposes using, I consider that idiotic.

TMI throws away masses amounts of components at the top and bottom end, but mostly the top, and averages the rest.

I commented on TMI on January 4, 2022.

Please consider my January 4, 2022 post (chart above) Trimmed Mean Inflation Is the Ultimate Absurdity in Inflation Measures

Measure Comparison

- Essentially the Dallas Fed says lets throw out the top and bottom items of the PCE and average the rest.

- The PCE stands for Personal Consumption indicators and is the Fed’s preferred measure of inflation.

- PCE differs from the CPI in that it counts expenses paid on behalf of consumers such as medical insurance.

- The Consumer Price Index weights rent much higher than the PCE which in turn weights medical higher.

Even with that explanation it’s not quite clear how the Dallas Fed fabricates a preposterous 2.8% year-over-year measure of inflation.

A chart download shows the magic of throwing out “a certain fraction” from both ends to “outperform” conventional measures.

Click on post for more details. Again, note the date January 2022.

Wash beats up on Powell for getting things wrong, but he proposes using an idiotic measure that is as least as bad, in arguably similar circumstances.

“Rosie pointed to the Dallas Fed’s trimmed mean PCE as evidence the inflation problem was already beginning to solve itself. Rosie pointed to the Dallas Fed’s trimmed mean PCE as evidence the inflation problem was already beginning to solve itself,” noted Mauldin.

Yes, just like it did in 2022.

I rest my case. Lacy is now in the right place. Welcome Lacy.

It seems as a lot of people blame one party for all our disasters. How about this, they both are horrible. Until this country gets term limitations, things will get worse. Meanwhile, our youth wants socialists. I just don’t get it!

The youth want Socialists because billionaires are turning out to be a scourge, and capitalism feels like it is broken at the lower rungs of the ladder.

I may disagree but I understand the appeal.

I can understand T bills, as a temporary place to park money, but 10 or longer notes or bonds are not going to even keep up with inflation, so why bother? I think we are in for a long period of serious inflation, and one must do their best to offset this decline in the purchasing power of the US dollar.

I don’t understand why the Fed is buying so many T-bills. Seems so pointless.

Lacey Hunt seems a bit late to the game. The secular bull market in bonds ended in 2021. Post WW2 the bear market in bonds ran from 1946 all the way to 1981, the secular bull market ran from 1981 all the way to 2020. It was obvious to many the turn in bond rates with the rise in inflation from 2021 was upon us. The secular bear market which we are in is likely to run and run, compounded by the inability of the Western world to get a grip on deficit spending.

I agree – but better late that never

Compare to Rosenberg and Danielle DiMartino Booth and the entire truflation crowd.

I am not overly concerned about Powell or Warsh or the Fed. I believe that ultimately, the market will set rates.

My bigger concern is with the global economy going forward.

Since the end of the WW2, the US has been at the forefront of global economic development and prosperity. The US forged political, military, and economic alliances with most countries in the world after the war. We encouraged free trade and provided the naval security needed to allow the free flow of goods worldwide.

The result was massive global economic growth and increasing standards of living that benefited those who were willing to work with us.

The biggest beneficiary was the US itself, as our economy and living standards skyrocketed. We were the shining example of what free markets, capitalism and cooperation could accomplish.

But nothing lasts forever. The US is now dismantling the very system it put in place for shared prosperity. We are no longer nurturing the relationships we developed with the countries that we called friends, partners and allies. Instead, we threaten them with tariffs, trade restrictions, and sanctions. Worse still, we threaten their very sovereignty with talk of takeover and annexation. We no longer consult with them; we merely tell them what we think they should do for us.

We are no longer the world’s policeman; if we ever were. We are now the world’s criminal state; invading, bombing, threatening, and shaking down others for our own short-term benefit.

This is a structural change that will alter the world in very significant and negative ways going forward. The key reason will be the “uncertainty” that this change will cause.

The first grenade that was lobbed into the gears of the global trading system was tariffs placed on almost every country in the world. This forced a rerouting of trade routes and flows that is still going on; raising costs and causing disruption. Uncertainty of supply also forces governments to rethink “security” of supply. This results in hoarding, stockpiling, and expensive efforts to self produce.

Grenade number 2 is our inability to guarantee the free flow of goods being shipped all over the world. This recent uncertainty will raise shipping costs as companies seek safer, but longer alternate routes. Insurance rates will rise. Delivery times will lengthen.

Grenade number 3 is our attack on Iran. This led to Iran taking control of the strait of Hormuz and interrupting the free flow of 20% of the world’s oil and gas; as well as helium, sulfuric acid, fertilizer, aluminum etc.

Oil and gas are the lifeblood of the global economy. So far, we have managed to prevent an economic collapse by burning through storage and reserves. But those are running out. Shortages of refined products are already occurring, and they are about to get a lot worse. The global economy is heading into a recession as a result.

Assuming the best case scenario and the strait opens again soon, the structural damage is already done. The level of global shipping through the strait will not return to previous levels and more expensive and time-consuming alternative routes will be sourced going forward.

Assuming that Iran keeps control of the strait, then shipping will be even more disrupted, with upward pressure on the price of oil and other products that normally transit.

The net result is a stagflationary combination of slower global economic growth and higher prices for the foreseeable future.

It took many decades to build the trust needed to develop the global trading system to the benefit of all. Trump has managed to undo it all.

And this will irreparably damage the future of the country for ourselves and our children. Let’s not forget this was 100% aided and abetted by Republicans in the House and Senate, 3 of which (2 Senators and 1 Rep) I voted for. They happily traded the future of the country for short term political safety. Never again. I will vote party line Democrat until every one of these cowards are gone.

I think most folks who voted republican didn’t see any of this coming. All Trump had to do was eliminate red tape and allow prosperity to take off but he blew it big time.

Though I don’t recall that being a big part of his platform.

Hes covering for a bunch of pedos and his crimes.

You should consider not voting for state and local republicans also. The way i see it. When you vote republican you are voting for the republican party not a representative. The republican party is controlled by welathy individuals corporations and such who can throw an ever increasing amount if money to get voters to elect their guy. Look where the money comes from for conservative talk shows. . Charlie kirk was not getting money from selling tickets at the door. Its an organized machine. Dems seem to be more loosely organized. Imo.

Im an independent an over the last 15 or so years i find it hard to vote r.

Exactly, very well stated!

You say Shared Prosperity like it is a real thing. Monetization has just created larger numbers. Not higher quality or wealth.

Eh, cars are way better now than in the eighties.

Houses are bigger.

More people have college education.

Healthcare can do incredible things compared to fifty years ago.

We live a vastly higher standard of living than our grandparents did.

Now whether we are happier — that is debatable.

Non of the things you mentioned are shared prosperity. They are all expensive individual choices. The 80s were a bad time period for cars except Japanese cars, and just a few great American cars. The very newest cars are garbage and have expensive problems because of over engineering. College costs more than ever, and is loaded with debt for a lot of useless degrees. A greater number of Educated idiots is not prosperity. Many of the brightest people I know are not college educated. Houses are bigger but of poorer construction, often using wafer board for sheer requirements. People are more unhealthy than ever so medicine has to be more dynamic. Depression is at all time highs. Modern society is overwhelming for the majority. There is no shared prosperity. Only individual success stories often at other people’s expense. I am ok but I see so many desperate lives. All I can do is pitch in and help others. Unless someone is really pitching in to help others their prosperity is not shared. Let’s not fool ourselves.

In his December 5, 2010 60 Minutes interview, Bernanke was asked whether the Federal Reserve could act quickly enough to stop inflation if it began to accelerate. His response:

You make a lot of sense. Thanks Spencer.

Say what you will about Powell, but he decoupled US rates from LIBOR and its successor, thereby reducing undue City of London influence of US markets, not to mention kicking the Eurodollar to the curb. Resisting Trump’s demands for lower rates probably spared the US from at least two years of malinvestment, which seems to be the baikiwick of Real Estate developers, inter alia.

1/ People who should know better ascribe all blame for Fed policy to Powell. They forget he is the chairman of a *19* member board, 12 voting at any given time. He can try to steer the conversation but does not have carte blanche.

2/ Iran war inflation is not just oil and its derivatives (plastics, etc). Aluminum, fertilizer and many other inputs are now in short supply and it will take quite some time for that to reverse. Oh – and companies will never ever lower prices again so it is structural, not transient.

If any of you want to know your future, just look at England…

Donald Trump’s Inflationary AgendaHe was elected to tackle one problem. Instead, he’s made it worse.

https://archive.is/nFz9D#selection-609.0-615.66

I have an ex co-worker that’s just like the first guy in the video wearing the red shirt and hat, completely clueless cult member that will support Trump no matter what.

https://www.reddit.com/r/TikTokCringe/comments/1texbib/i_dont_know_you_caught_me_off_guard/?utm_source=share&utm_medium=web3x&utm_name=web3xcss&utm_term=1&utm_content=share_button

Whenever I ask him what Trump’s done, he comes up with stupid things like “freedom” or “the economy” – he is on the verge of losing his job, called me to have lunch to “catch up.” He’s really fishing for job opportunities. Total moron.

The last 44 years has been characterized by:

All of these things have been massively disinflationary allowing bond yields to collapse and bond prices to increase.

The next few decades will be characterized by:

These things put together will put upward pressure on inflation and interest rates, forcing down long-term bond prices. If AI makes it to the next step, it will be the only brake on an inflationary future, and maybe not a large enough one to make a difference.

Donald Trump put an end to the era of American economic and financial dominance. And that is not really Trump, but the voters who put him in power. We have moved to an inflection point in history where the US becomes a far weaker player and the American people become far poorer for decades to come.

As I try to repeat here often: inflated dollars end up on corporate P&L statements. Your only hope is to be invested in those corporations best able to control costs through some level of vertical integration and have pricing power through some level of market monopolization. Those corps who have a strong international presence will also be successful as they can sell in higher valued currencies.

Trump’s Corruption Is Going to Sink HimConditions are right for voters to stop turning a blind eye to his greed, grift, and gold leaf.

https://www.thebulwark.com/p/trump-corruption-irs-lawsuit-plane-crypto-scam-pardons?utm_medium=web

This is also fundamentally driven by the fact that economic Empires are cyclical. Your lists describe the effects oh the rise and waning of an empire.

One could argue that Trump is the populist side effect of the citizens having trouble accepting this reality.

I agree with your investment thesis, and so do corporations which are becoming more and more trans national for the same reason

inflation happened well before trump. the very things you mentioned would have destroyed the system eventually imo. every president bails out the banks in the end, and the rich get richer and buy assets and stocks which will also inflate. it’s exponential and takes time.

you think the next corporate dem will change things? Also you blame the voter when we live in a first past the post republic. non politicans have very little power vs the capitalist oligarchy in charge.

legal corruption is what is destroys are system. You think trump did this all by himself? You must think trump is a super genius and the smartest person to have ever lived.

No, I certainly don’t think Trump did this by himself. I simply think that Trump’s solutions are the exact opposite of what needs to happen. The problems are extremely complex, and Trump’s simplistic solutions have great appeal to simplistic voters. I don’t for a second think Democrats are going to solve the problems either. They will just make it less worse than Trump will.

In 2020 Trump increased the money supply for Covid. Very simple math and I know it complicated blah blah blah but the simple fact is the money supply increased from 4T to 16T

https://tradingeconomics.com/united-states/money-supply-m1

it is all Trump the molester and Thief

Agree.

Oil jumps almost $5.00 on Trumps return from China and he and Fox declare success.

Are Fox watchers clueless?

I watch it as a form of parody for its comic value alone.

As humans we all work on assumptions, and when these assumptions are dictated from above (officials with authority), practiced, and then rewarded (good paying job for example) it’s hard to believe in anything else but the assumptions of what one has built their entire lives around.

People will go to great lengths to ensure their beliefs stay the immutable truth that gives them meaning, hope, and self-expression. They can be presented with facts that proves without a shadow of a doubt their beliefs aren’t reality, and yet they will disregard these facts even to their own peril (if believed strongly enough).

Beliefs arise from conditioning so we look at the social fabric of an individual and can see the connection to other individuals and organizations. These small threads off the fabric of society which connect to the individual are often tied to like minded individuals who hold the same beliefs as one’s own.

To suddenly arise to a moment of the poison of truth, which smashes belief, one sees not just how deeply the poison runs through the threads of their own life, but also the fabric that makes up the society one lives in. This experience is so traumatic for most humans that they choose to live in self chosen ignorance. Refusing to be around others who don’t think like them, or engage in the same social rituals, or even hold a conversation with people that have a different belief. If pushed to engage and interact with these beliefs that differ from what one holds for themselves often we see violence.

“Are Fox watchers clueless?”

I wouldn’t call them clueless, its more of a self chosen ignorance and it’s for survival.

Marx once said religion is the kool-aid (opium) of the masses, but today in America I would argue politics has become the kool-aid of the masses; so much so that Americans can’t see the peril they are now in.

You get a Mishelin star award for excellent comment.

The universe is built around “control systems” – they are immutable systems, mathematics is the founding layer which leads to the layer of physics, then chemistry then biology. Biological systems then have own sets of layers using the aforementioned foundation layers which lead to cells, neurons, organs, bodies then brain. The brain then creates its own systems to navigate the layers of the universe.

To make a long story short, we get to where we are today with new control systems based on religion, politics, socio-economics, etc.

Then there are high dimensional layers that will be over the head of most of the commenters here, especially the lizard brain MAGA cult so we’ll leave that discussion for another day.

But yes, your comment is a nice way of saying you need an exit strategy from the current control environment.

“You get a Mishelin star award for excellent comment.”

I appreciate your kind words, thank you.

When we talk about control environments (the glue that holds society together) and escaping them we often find violence was required unfortunately. This happens because those in control refuse to see reality that sits outside their beliefs, and often double down or more to force their beliefs not only on those they can exert control on but also on reality itself.

Refusing to consider reality leads to stagnation: the inability to innovative, the inability to compromise, the inability to find solutions to problems, and the inability to find beauty in diversity. This leads to the deterioration in living standards and ultimately the death of society itself.

The Western world has lived in stagnation for a long time now, and its own people along with the rest of the world are sick of its failed beliefs being shoved down their throats. Thus the death throes of a society is plagued with violence, internally and externally, and such violence eventually becomes the birth pains of a new society.

What we will witness in less than 20 years is something most humans in history rarely see: a true global paradigm shift of power. And though this will be painful to endure it should still be viewed as an honor to be living through these times.

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.”

– Charles Dickens

A human i know, a card-carrying communist, said that religion is not the opiate of the masses. Nobody believes in God anymore.

Rather, buying on credit is the opiate of the masses.

Remember when this type of interesting economics and finance analysis were all you would read on MishTalk? Sigh…..

Lol.

We wouldn’t be having this conversation if the the political events he covered that you’re presumably griping about hadn’t happened. Many people including myself are not interested in economic legerdemain practiced in isolation from reality. Seeing economic consequences follow from real world choices is compelling. Actions have consequences.

The Chinese Nostrsdamus says WW3.

https://m.youtube.com/watch?v=BTJGr78-zyw&pp=ugUEEgJlbg%3D%3D

No election in 2028 BTW. And Russia will join Iran. The US agreements with Gibraltar and Indonesia are going to cut off global trade.

The playbook is straight out of the Pentagon. Trump clearly is following it according to the video.

TRUMP: “We’ll keep bombing Iran until the Dow gets to 50,000 or higher, anything lower then 50,000 and the bombing will continue.”

Thank you for you attention to this matter!!!

Trump has never built anything of value. Inherited his wealth and purposefully went bankrupt multiple times ~ lies, war and destruction are the only things he is good at.

Mish, how are you invested?

QT is pretty much out of the question.

Since Dec 3rd, 2025, the Fed has been practicing Quantitative Easing.

Over $190 billion has been added to the Feds balance sheet and things are just getting going.

https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

Shhhhh, it’s Stealth QE…

Given the massive increase in US debt and deterioration of our credibility as ally, trading partner or friendly nation, it seems that our credit rating may be reviewed and a downgrade would result.

What would that do to interest rates?

I cast the bones.

And the bones say?

Shi no kami

got oil? https://imgur.com/a/gvmz5BJ

When it comes to tariffs my question is what his plan will be if he loses house and senate. Because it’s looking entirely possible now and it seems like that would be an unceremonious end to the king ruling by decree.

His plan is to have the Election Integrity Army intimidate people that look like they’ll vote against him, and if that doesn’t work cry that the election was stolen.

He will have to be dragged out, someone will have to be willing to do what it takes to drag him out, and the golden statue worshippers will need to be persuaded to let him be dragged out.

“His plan is to have the Election Integrity Army intimidate people that look like they’ll vote against him, and if that doesn’t work cry that the election was stolen.”

It would be far simpler and easier to mask the truth by using the current war with Iran to suspend elections. All that needs to be done is either a false flag event that can be said puts American security at risk, or due to lack of oil (and other supplies like food) the govt can implement covid style lockdowns, again for national security.

I’m not saying it will happen like this, it’s just if you want to control the outcome of the election you need to either put fear into people or doubt that it wasn’t planned for it to be successful without pushing the country into civil war (which having an “Election Integrity Army [to] intimidate people” publicly would do; ICE push back supports the fact this could happen).

And crying foul about the integrity of the elections is a dead end IMO because of the nature of midterm elections, which are controlled by the state and the fact that there is over 400 separate elections for the house just alone. Its just very hard to prove IMO and thus if there was an investigation and brought to a judge I doubt they back Trump.

This last option is the hardest to succeed IMO and Trump be better off using an “Election Integrity Army [to] intimidate people” as you say. At least in this situation should the citizens push back he can have the excuse to roll out the military and suspend elections.

Yes and not much going on with the epstein files anymore

The reason he made such a issue about an election being stolen is he is doing the same thing. the redistricting in the red states to control the house and the intimidation he is putting in place. It is one of his tactics blame the other for what you have done or about to do.

The trimmed mean will allow Warsh to *say* inflation is low as a pretense to hold the Effective Funds rate steady or even cut. Meanwhile the actual neutral rate (vs the rate reported) gets pushed up, and the real (inflation adjusted) interest rates will be negative for corporate debt and Treasury bonds. Back a few decages ago, when people had critical thinking skills, the bond market would see right through this, and just completely ignore Warsh’s reported inflation number. I’m not sure how things were done a few decades ago will shine through today though, since markets no longer pay attention to fundamentals. Warsh’s “trick” (aka lie) might actually “win” in today’s environment, keeping long bond rates low.

PS The way inflation works in the real world is that it rolls through one sector at a time rather than being applied broadly. The net effect of this is that trimmed inflation will never account for this, and it will always look like no inflation, rather than the actual “rolling” inflation, acting like a forest fire, blazing through sector by sector, one sector at a time.

The problem is there may be a shortage of lenders which will drive rates up at the auctions. Warsh can do what he wants but there is a supply vs demand issue which he can’t lie his way through.

You almost need a recession to trigger the flight to safety to support US borrowing and maybe drive down inflation (or maybe not).

Trump has truly messed things up.

Oil is behind this inflation, and that supply chain’s not getting fixed for at least a couple months. This minor number diddlery wont make much difference.

Higher interest rates would reduce speculation in the makets, since the risk/reward would moves things towards risk off (aka less inflation). Interest rates are just a knob that controls speculative activity. And speculation is always inflationary.

did you notice the chair? None of this was accidental. The Chinese are masters of protocol: every chair height, every step, every distance is calculated. Trump’s chair sat lower than Xi’s because Beijing wanted it that way. https://imgur.com/a/xOt5frc

Xi always looks like he’s about to giggle.

Trump’s body language shows weakness.

He looks like he’s about to keel over and die.

Oh you tease

Taco has caused more economic damage than any previous president in the shortest period of time.

Incredible damage! Like nobody’s ever seen!

AI and associated tech/infrastructure and associated equity growth frothily fed on themselves; private credit sources provided the frenzied and circular credit expansion. Stressed private credits sources have already underwent debt default and restructuring with falling associated equities in 2025 (eg Blue Owl and Blackstone) The Fed must now supplement t-bill purchases in the vacuum of shifted investment and defaulting private debt. Now add the ongoing oil shock …(Global manufacturing, consumer, farmer stress.) Now add an extra 4-500 billion for defense spending … Where are the buyers for that new debt? (The Fed) Lucy is right. Danielle DiMartino Booth’s recessionary disinflation scenario will become obvious when gold and oil fall 40-50% in the next 9 trading days during the global equity initial crash.

Not 9, 8 trading days globally; 7 trading days for the US.

these people love it all

https://www.reuters.com/business/energy/trump-says-iran-war-is-worth-economic-pain-these-rural-voters-agree-2026-05-16/?link_source=ta_bluesky_link&taid=6a08460005fd2a00018cbe86&utm_campaign=trueanthem&utm_medium=social&utm_source=bluesky

Do they love that Trump promised China they could send 500,000 students to America and use American farmland? Lol.

https://newrepublic.com/post/210539/maga-reeling-trump-welcomes-chinese-students-us-farms-xi

who needs open borders and ICE when you got Trump pouring them in legally.

Once we’ve sold our land, are we illegals?

Them Eyrainians can’t be having noooklear weapons… baby Jesus says so!

But them Israelis killed Jesus cause he was preaching peace and they can’t have that!

They killed grownup Jesus, I only care about baby Jesus.

It is my opinion (more like a hunch, but probably correct) that in order to have actual sustainable inflation of the dollar, there needs to be more dollars circulating around in the economy to sustain the higher price levels.

We had that during COVID, with at least $12 trillion appearing out of nowhere (don’t ask where it came from) that caused the price levels economy-wide to increase around 40% since 2020.

In order to have sustainable inflation now, there has to be more dollars entering the system to meet the higher price levels. Federal deficit spending will serve that purpose and I think we’ll see more of that soon. The Fed will start buying federal debt like they did during COVID and then we’re off to the races.

I do think there will be some sort of “gas rebate” gimmick very soon. Just remember, there is no such thing as free money. There’s always a price to pay.

“gas rebate” gimmick Is that not part and parcel of the repeal of the gas tax is?

The shifting of time deposits to demand deposits increases AD.

2-star Mishelin award for an excellent post. Curiously, I was thinking about Lacy Hunt recently, he used to get many mentions in the past then disappeared. I think there is a Mishtalk TV episode somewhere with him.

Everyone’s talking about the return of the 1970s inflation and if we are at the start of it expect out-of-control costs over the next few years, gee who has been saying that for a while now?

I am assuming politicians will use the same playbooks: price controls, dumb policies, appeal to people to cut back, heavy taxation, and eventually raise rates to the heavens.

I will be positioned for massive profits 🤗

Of course this post needed a musical tribute for Lacy. I suggest Cindi Lauper’s Change of Heart.

https://www.youtube.com/watch?v=svHeFdSvPL0&list=RDsvHeFdSvPL0&start_radio=1

“It’s Trump turtles all the way down and inflation all the way up!”

and

Do worry, Trump will find a way to make things even worse.™

The Great Inflation of the 70s was due to the monetization of time deposits.

It doesn’t freaking matter what causes inflation, the only thing that matters is how to earn enough profits to stay ahead of it.

On the day the market bottomed, I repeated myself 3 times:

That’s B.S.

Bottom’s in.

Mar 23, 2020. 10:34 AM

Link

Margin Call: The Story Of A Historic Week – The Heisenberg

Bottom for stocks, not the economy. It will decouple.

Mar 23, 2020. 10:33 AM

Link

We Likely Saw The Bottom – Michael A. Gayed, CFA

The bottom’s in.

Mar 23, 2020. 10:28 AM

I’ve watched Danielle DiMartino Booth’s podcasts with other financial media. I think she has very good analysis. Her call for disinflationary recession aligns with observations of FedReserve actions due to bank stress. Consumer use of credit for necessities is an indication the money supply is not driving prices up; otherwise, people would have jobs to pay for needs. Defaults are deflationary because the credit is contracting.

Since October 2025 our means-of-payment money supply has increased by 1.161 trillion. Inflation was the inevitable consequence.

The bull market in bonds was caused by the drop in the transaction’s velocity of money.

Professor emeritus Pritchard never minced his words, and in May 1980 pontificated that:

“The Depository Institutions Monetary Control Act will have a pronounced effect in reducing money velocity”.

The DIDMCA caused the Savings and Loan Association crisis, or “the failure of 1,043 out of the 3,234 savings and loan associations in the United States from 1986 to 1995”; and created the U.S. July 1990 –Mar 1991 economic recession.

Demand deposit turnover went negative for the first time since the GD.

And if you destroy the nonbanks, you destroy velocity as in the GFC.

Velocity is a nonsense measure. It predicts nothing. It is a result.

It can rise or fall with rising or falling GDP.

Totally useless.

Income velocity, Vi is a contrivance. Friedman bastardized the equation of exchange that he had printed on his car license plate. The transactions’ velocity of money has sometimes moved in the opposite direction as income velocity, as in 1974-1975 or 1978 (all economist’s forecasts for inflation were drastically wrong in 1978).

Money has no significant impact on prices unless it is being exchanged. To sell 100 bushels of wheat (T) at $4 a bushel (P) requires the exchange of $400 (M) once, or $200 (Vt) twice, etc. Or a dollar bill which turns over 5 times can do the same “work” as one five-dollar bill that turns over only once.

There’s been no valid velocity figure reported since Ed Fry discontinued the G.6 Debit and Deposit Turnover Release in Sept. 1996 (by mistake)

Dr. Philip George gets this right. “Changes in velocity have nothing to do with the speed at which money moves from hand to hand but are entirely the result of movements between demand deposits and other kinds of deposits.”

Vi, a contrived figure, “≠” Vt, or money actually exchanging counterparties. And no money stock figure standing alone is adequate as a guidepost for monetary policy. Aggregate demand, AD = M*Vt and not N-gDp as the Keynesian economists define it.

Example: In 1978 (when Vi fell, but Vt rose) all economist’s forecasts for inflation were drastically wrong.

Put into perspective: There were 27 price forecasts by individuals & 9 by econometric models for the year 1978 (Business Week). The lowest (Gary Schilling, White Weld), the highest, (Freund, NY, Stock Exch) & (Sprinkel, Harris Trust & Sav.).

The range CPI, 4.9 – 6.5 percent. For the Econometric models, low (Wharton, U. of Penn) 5.7%; high, 6.6% U. of Ga.). For 1978 inflation based upon the CPI figure was 9.018% [and Leland Prichard, in his Money and Banking class, predicted 9%].

The “result” is the distributed lag effect of money flows. The equation of exchange is a truism.

Contrary to Nobel Laureate Dr. Milton Friedman, there is no “fool in the shower”

“Extrait du Bulletin de ISI of 1937”. – History and forms. Irving Fisher (1925) was the first to use and discuss the concept of a distributed lag.

In a later paper (1937, p. 323),

American Yale Professor Irving Fisher stated that the basic problem in applying the theory of distributed lags:

“is to find the ’best’ distribution of lag, by which is meant the distribution such that … the total combined effect [of the lagged values of the variables taken with a distributed lag has] … the highest possible correlation with the actual statistical series … with which we wish to compare it.”

…Thus, we wish to find the distribution of lag that maximizes the explanation of “effect” by “cause” in a statistical sense”.

The earliest form of the velocity of money was formulated to show a relationship between the quantity of money and the value of all transactions. This is very different from the current formulation, which draws a relationship between the quantity of money and GDP, which is the income of a country.

Zombie Concepts: Velocity of Money – Joseph Wang (fedguy.com)

US recession predictor, US Treasury yield curve inversion is usually right within 1 – 2 years. Now it’s over 3 years. OVERDUE.

The most respectable predictor is going to be wrong if Trump doesn’t save.

Now predicting, as seen in the above article, TRUMP RECESSION is coming.

You know, I was always kind of surprised how property taxes were always left out of inflation calculations, as if those large amounts will “eventually” add 1-2% increases in 10-15 years. I recently read two articles with property tax increases (and now house insurance) on the same list as energy, transportation/gas and food as inflationary components. Maybe someone is realizing 15% of workers getting government pensions are gonna start to add to the average homeowners tax bill. And rates going up accordingly. We need more money.

In his 1967 presidential address to the American Economic Association, Milton Friedman articulated the challenge monetary policymakers face in setting policy based on the neutral real interest rate, also known as the natural rate of interest:

One problem is that it (the monetary authority) cannot know what the “natural” rate is. … And the “natural rate” will itself change from time to time.2

Interest is the price of credit. The price of money is the reciprocal of the price level.

Lending by the Reserve and commercial banks is inflationary (loans create deposits). Lending by the nonbanks is noninflationary (loans activate savings), other things equal.

If monetary savings are not expeditiously activated, then a dampening economic impact is generated in the circular flow of income (secular stagnation).

Link: “Changes in Wealth and the Velocity of Money”

Savings dissipated in financial investment, or impounded in idle savings, or as leakages in transfer payments, are stoppages in the flow of funds derived from the main income stream and have a direct and immediate dampening impact on the economy.

The flight to liquidity represents an inflection point. It is an increase in the demand for money.

Agree here. No one knows what the neutral rate is. The Fed tries to find it with backward looking data and frequently chases its tail.

any views on gold, especially in a rising interest rate and inflationary environment?

But have you seen the Dow lately?

💩 💩 💩