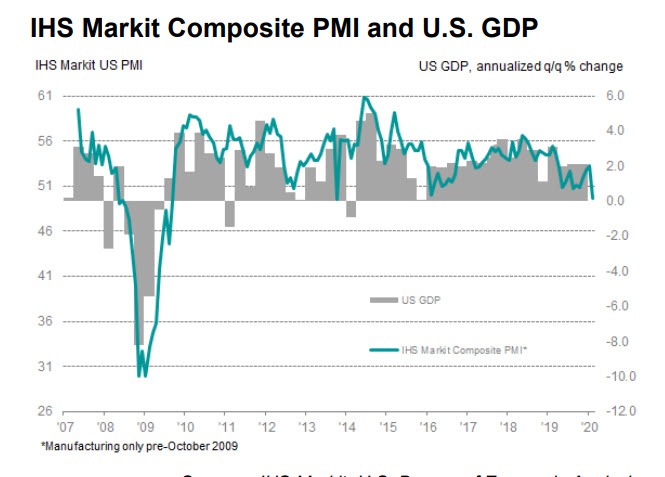

Markit reports Output Contracts for the First Time Since October 2013.

Key Findings

- Flash U.S. Composite Output Index at 49.6 (53.3 in January). 76-month low.

- Flash U.S. Services Business Activity Index at 49.4 (53.4 in January). 76-month low.

- Flash U.S. Manufacturing PMI at 50.8 (51.9 in January). 6-month low.

- Flash U.S. Manufacturing Output Index at 50.6 (52.4 in January). 7-month low.

Adjusted for seasonal factors, the IHS Markit Flash U.S. Composite PMI Output Index posted 49.6 in February, down from 53.3 in the opening month of 2020. Although only fractional, the decrease in business activity brought to an end a near-four year sequence of expansion following a contraction in service sector output and a slower rise in manufacturing production amid supplier delays following the outbreak of coronavirus.

New orders received by private sector firms fell for the first time since data collection began in October 2009.

Inflationary pressures softened in February. The rate of increase in cost burdens eased to the slowest since last October amid reports of lower demand for inputs. As a result, private sector companies raised their output charges at the softest pace for three months.

Chris Williamson, Chief Business Economist Comments

- “With the exception of the government-shutdown of 2013, US business activity contracted for the first time since the global financial crisis in February. Weakness was primarily seen in the service sector, where the first drop in activity for four years was reported, but manufacturing production also ground almost to a halt due to a near-stalling of orders.”

- “Total new orders fell for the first time in over a decade. The deterioration in was in part linked to the coronavirus outbreak, manifesting itself in weakened demand across sectors such as travel and tourism, as well as via falling exports and supply chain disruptions. However, companies also reported increased caution in respect to spending due to worries about a wider economic slowdown and uncertainty ahead of the presidential election later this year.”

- “The survey data are consistent with GDP growth slowing from just above 2% in January to a crawl of just 0.6% in February. However, the February survey also saw a notable upturn in business sentiment about the year ahead, reflecting widespread optimism that the current slowdown will prove short-lived.”

Yesterday I commented Record Low 30-Year Bond Yield and Record High on Gold Coming Up

And here we are. The 30-year long bond hit a new record low yield this morning of 1.896%.

Gold is up $29 to $1649.

As noted previously, there is Little Chance of Coronavirus Containment in South Korea.

And in China, Half the Population of China, 760 Million, Now Locked Down

From an economic standpoint, January saw the Largest Shipping Decline Since 2009 and That’s Before Coronavirus impact hit.

I expect a surprise rate cut at some point. This combination adds fuel for a further rise in the prices of gold.

In case you missed it, Gold at Record High in Euros. A record high in US dollars is also coming up.

Mike “Mish” Shedlock

What has been keeping the economies afloat for many years, the service sector, will be the first sector to implode in case most countries have to apply real containment measures to stem the virus, like China is doing now.

We now know that ten of thousands of virus (mostly non symptomatic) bearers and spreaders have travelled out and in and out China for some weeks before these containment measures started to be applied forcefully. The resulting silent infection in Iran is an example .

Should containment measures not be enforced carefully (like in the case of Cruise vessel, Chinese prisons, Iran, …) then the world pandemic will be the outcome together with a general economic collapse.

There seems to be at this stage (no way to kill properly the virus so far) no positive short term outcome for the world economy in general whichever scenario you choose…

Pray tell was there a recession in 2013 when PMI contracted then ?

Yes we do have multiple problems now. 2013 seems like an eternity ago.

Time to shut the gates (if it’s not too late already) and impose quarantine on all who want to return. If you’re outside you made an unfortunate choice by travelling now. China, Japan, Korea, Iran, Italy–seems to me that meets the PANDEMIC definition.

New study release in London today says that perhaps 2/3 of transmitted cases outside of China have yet to come to light.

Headline at CNBC: Larry Kudlow says falling bond yields don’t reflect the US economy’s fundamentals

Right because as we all know bond investors are among the most generous people in the world, happily overpaying for every bond they buy!

Mish: “I expect a surprise rate cut at some point.”

I know easy monetary policy is apparently the modern cure for everything, but I do not understand how a surprise rate cut is going to help as long as the virus is in play. What exactly will that do other than push consumer inflation higher and kill the dollar? When business supply chains are FUBAR, is taking real rates even more negative for the next several months going to help sell more product or service existing debt? I imagine not.

Me also, and I think it could be a BOLD 50 BP cut, before the 15th of march. Coronavirus fallout. I hope so anyway, I am locked in on my mortgage set to close on the 6th of April, but that lock is only for rates to the upside, a rate cut would still be calculated into my mortgage. On the other hand mortgage interest used to be very narrowly +/- 100 BP of the 10 year treasury. If that were still the case we would see mortgages now at 2.465% while I just locked in at 3.785%. So the old rules are history and mortgages are exceptionally profitable compared to the coupon rates otherwise available.

From what you are saying, mortgage rates are reflecting a higher risk premium than they used to.

Again I ask, how will an emergency rate cut help anything in the context of economic disruption from the virus? China has opened the monetary spigots, yet housing sales and auto sales are still cratering nonetheless.

Yes, one could take it as an implied risk premium over the old traditional mortgage rates, but I am thinking it is actually one of two things not related to fear of another GFC event. One is debt levels; even though interest rates in general are low, to the point of REAL NIRP after REAL inflation, that debt still has to be serviced. And, then there is just good old fashioned greed.

I am in Portland today for a doctor appointment at the VA Hospital. I got gas and was shocked to see it is a full 55 cents higher here than in the southern part of the state. Regular selling at $3.399 even though it is leaving the refineries at $1.58. It would be profitable at $2.20 and premium which my car uses is 40 cents more. There is no economic reason for it other than just naked blind greed. It is not as if price elasticity is going to work here. You can’t just say hell with it then I just won’t go to work till the price is reasonable.

But, the possibility of another GFC housing crash type event is certainly not off the table, because what people get wrong about the GFC is they think it was being driven by sub-prime. That was the trigger back then, but what drove the GFC was leverage and liquidity issues. With the residential real estate bubble now worse that it even was then, and households even more loaded up on debt relative to income, and liquidity issues as bad or worse in financial markets (Look at Deutsche and HSBC both on the very edge of collapse) it is going to take trillions for the PPT just to get through this day. Those banks can serve as the trigger just as well as sub-prime did. The equity market is easily priced at 200% of anything like a fair valuation and just five stocks are leading most of that bubble blowing.

It is no longer a matter of IF now, but when, and what comes after.

A surprise rate cut will do what a surprise rate cut always does: Transfer wealth to those who own assets benefiting from the rate cut. From those who do not. The virus, like anything else, is just an excuse to do some more of that.

Central banks have gone completely beyond the pale.

You’re asking sensible questions. We have already made the leap to a post-rationalistic economic parallel universe.

6 more people in Italy, hundreds more people in Iran, yet if you go to a live feed at@jcheethamwriter and watch the live feed from a Thai tourist bar area you will see no protective gear or apparent precautions, and as as he says, they will all be coming back to a city near you.

Meanwhile China orders millions back to work. This planet is one big slave plantation.

With new cases at a trickle in China, that was to be expected. Time to find out if new cases explode again.

Hubei said that economic activity would resume March 11th.

Who knows?

The hit reported is in the manufacturing end of things, but we are told that that end of the economy really doesn’t matter any more…

…but in the much vaunted “service” economy of the US, what is the hit when travel is self-restricted (or government-restricted)? What happens when far fewer eat out, attend events with others, do as little shopping as necessary?

“The hit reported is in the manufacturing end of things, but we are told that that end of the economy really doesn’t matter any more”

…

Read again.

Manufacturing PMI 51.9 —> 50.8

Services Business Activity 53.4 —> 49.4 (consensus 53.3)

I have to say that the reported drop in services business activity is pretty small to what will happen when it penetrates the consciousness of the general population or when actual restrictions are placed on activities.

“The survey data are consistent with GDP growth slowing from just above 2% in January to a crawl of just 0.6% in February. “

…

January benefited from being warm. February has been more of the same (probably not quite as nice. I live in a mid Atlantic state and haven’t seen a snowflake in over a month). Nice weather + seasonal adjustments = masking of true picture.

Imagine what happens in the services sectors when a big segment of the people no longer go out to eat or drink, no longer go out to see movies, no longer travel for pleasure or business, avoid public transportation options (including ride-sharing), avoid shopping, avoid any event with large audiences, etc, etc. Good for netflix and other streaming/broadcast services–bad for most of the rest of the economy.