Sales are mostly stable in a broad range, but inventories are rising and consumer sentiment souring.

The Census Department New Residential Sales report for April 2026 shows a 6.2 percent decline in sales.

New Home Sales

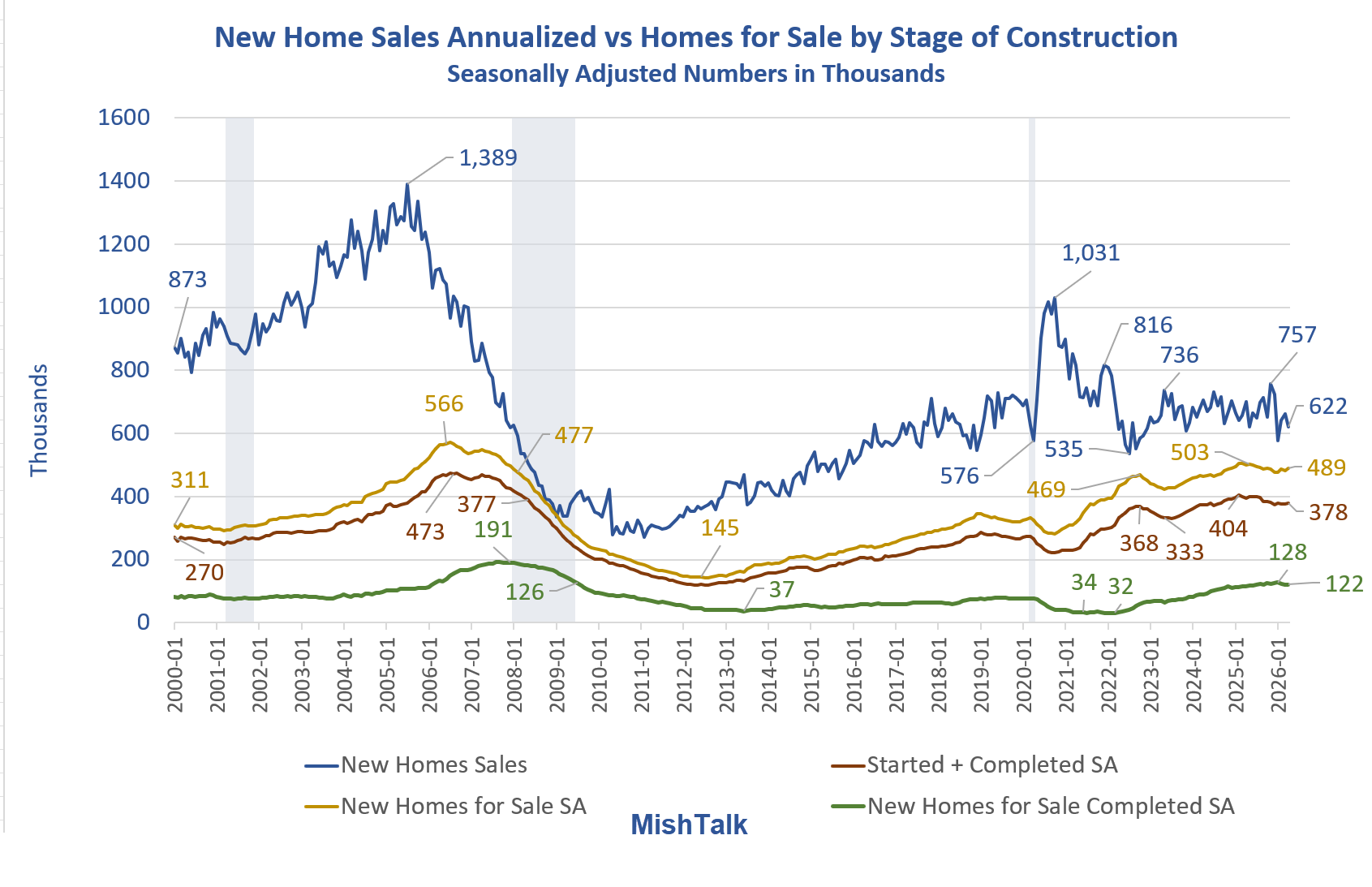

- Sales of new single-family houses in April 2026 were at a seasonally-adjusted annual rate of 622,000.

- This is 6.2 percent (±12.8 percent) below the March 2026 rate of 663,000, and is 11.3 percent (±11.5 percent) below the April 2025 rate of 701,000.

For Sale Inventory and Months’ Supply

- The seasonally-adjusted estimate of new houses for sale at the end of April 2026 was 489,000.

- This is 1.7 percent (±1.2 percent) above the March 2026 estimate of 481,000, and is 2.2 percent (±3.9 percent)* below the April 2025 estimate of 500,000.

- This represents a supply of 9.4 months at the current sales rate. The months’ supply is 8.0 percent (±16.3 percent) above the March 2026 estimate of 8.7 months, and is 9.3 percent (±13.5 percent) above the April 2025 estimate of 8.6 months.

Sales Price

- The median sales price of new houses sold in April 2026 was $422,500.

- This is 8.0 percent (±9.3 percent) above the March 2026 price of $391,100, and is 2.2 percent (±9.0 percent) above the April 2025 price of $413,600.

- The average sales price of new houses sold in April 2026 was $508,800. This is 0.7 percent (±8.6 percent) above the March 2026 price of $505,200, and is 1.1 percent (±7.1 percent) below the April 2025 price of $514,300.

General Comments

The margin of error in these monthly reports is huge, ±16.3 percent on supply and ±12.8 percent on sales.

The Commerce Department does not have a lot of confidence in the numbers, nor should anyone else.

It’s better to focus on long-term trends, and that’s why my charts do.

Long-Term Trends

From 2010 until 2019 (first set of arrows), people were buying homes faster than builders were accumulating unsold spec homes.

That was followed by a massive post-Covid spike in sales (no arrows) with a drop in unsold spec homes.

Since May of 2023 (second set of arrows) builders have had no traction. Sales are generally down, and inventory of unsold homes is generally rising.

New Homes For Sale by Stage of Construction

New Homes for Sale by Stage of Construction in Thousands

- New Home for Sale Total: 489

- Not Started: 111

- Finished: 122

- Under Construction: 256

- Under Construction or Completed: 378

I calculate total as the sum of Not Started, Finished, and Under Construction. The number may vary slightly from reported totals.

The number of finished homes for sale is high. Builders are under pressure to sell these homes in a very tough market, with rising mortgage rates too.

Unlike finished lots, started homes also represent a huge builder commitment. These are also high numbers but down a bit from a few months ago.

New Home Sales Annualized vs Homes for Sale by Stage of Construction

New Homes for Sale Supply

New Homes for Sale Supply in Months

- Official Supply: 9.4 Months

- Finished Supply: 2.4 months

- Started or Finished Supply: 7.3 Months

I don’t consider a vacant lot as a home for sale. So, I offer two alternative measures.

We see the same issue here. Builders are sitting on a lot of finished or started homes. Supply relative to sales is high and rising.

New Homes for Sale as Percent of New Home Sales

For Sale Percent of New Home Sales

- Total: 79 percent

- Under Construction or Completed: 61 percent

- Completed: 20 percent

These numbers will rocket if there is prolonged drop in sales from here.

Mortgage Rates

Between October 2023 and February 2026 Mortgage rates dropped from 8.03 percent to 2.00 percent.

October 2023 sales were 689,000. February 2026 sales were 641,000. Sales are now 622,000 and mortgage are rising.

This is evidence of a modest amount of price insensitive buyers, most likely wealthy buyers willing to pay cash and don’t care about rates.

Everyone else is trapped in setup where they are unable or unwilling to swap a 3 percent mortgage for a 6 percent mortgage.

Builders are also stuck. They have to sell. This puts puts pressure on builders, but with rising rates, potential buyers are not getting much if any relief from discounts.

Meanwhile, credit stress is high and rising. And consumers are in a seriously foul mood.

Related Posts

May 26, 2026: Consumer Credit Stress Is Comparable to the Great Recession

Auto delinquencies are at a new record and credit cards are near record high.

May 26, 2026: National Home Prices Decline for the First Time Since July 2025

I am pleased to report a month-over-month home price decline. But don’t get too excited.

May 28, 2026: PCE Inflation Spikes Again, Year-Over-Year Highest Since May 2023

Year-over-year PCE inflation jumped to 3.8 percent. The Fed wants 2.0 percent.

May 28, 2026: Inflation Expectations Surge in Two Distinct Consumer Confidence Surveys

57% of consumers say high prices are eroding their personal finances.

Au contraire de ce que tu prétends, cela n’est pas le cas.

There is a lot of pressure on retirees and workers to make more money.

Not sure how to interpret. 2% seems a low mortgage rate.

Mortgage rates were 2-8% lower than before, as a fraction of the mortgage per cent, so a few basis points?

I once read that Bill Gates got mortgage money at 1.5%.

Just sayin’.

Maybe drop[ped by 2% to 6.03? I know it breached into the five handle at least intraweek recently (last yr I think)

Those charts are telling another story nobody is discussing: builder strategy. When the housing market is growing in a healthy market, builders try to keep 1 month’s supply of completed homes, which is 10% of all new homes for sale.

With current levels at 2.4 months and 20%, and not started higher than the housing bubble peak; builders are still in speculation mode despite an economy that has every characteristic for the past 2-3 years of a recession except for 2 consecutive months of contraction. Builders bought into the story inflation is “temporary” and mortgage rates would fall substantially. At some point 3 years of temporarily is going to lead to capitulation.

29% of home purchases are all cash. This is down from the record 35% in 2023. As mortgage rates tick up, expect the percent using all cash to climb. The average down payment for those using a mortgage is about $80k nationally. Historically speaking, that is just an obscene amount for a down payment. Yes, there are people getting in with 3% down payments, but they are the exception not the rule nowadays (unlike when the Boomers and Gen-X were in the homebuying phase). Parental down payment support for 1st time byers is also near record levels.

Wondering if the decrease in all cash reflects a decrease in move down migrations by people moving into their last pre-retirement community home or age in place destination.

In the before times people examined such things as; The oldest prominent study forecasting the collapse of industrial civilization—and by extension the U.S. economy—within the 21st century is the 1972 MIT systems-dynamics study. Titled The Limits to Growth, the research was commissioned by the Club of Rome and modeled global economic and environmental trajectoriese

The Core Prediction: It concluded that if humanity continued to pursue unmitigated economic and industrial growth without accounting for resource scarcity and pollution, the global system would experience severe systemic declines—and potentially societal collapse—sometime in the mid-to-late 21st century

Plus let us not forget FUTURE SHOCK written roughly the same time.

Although I’m rather cynical and it’s hard to be optimistic at this point in time, the history of humans has always been one of boom and bust economic cycles, and things will get better at some point. Even if that point is decades in the future.

IMO, the U.S. is going through a slow collapse that began a few decades ago that is probably not reversible. Very similar to what happened to the Roman Empire. The Renaissance eventually happened, even though it was a long time after the dark times.

Humans are greedy, hysterical creatures.

It sure would be nice if at least some of our “flagship” housing datasets captured what was going on with the homebuilders in an accurate and timely fashion, so the average Joe wouldn’t/won’t be blindsided by the truth in 2027 😉

After the collapse?

That is why you seek a defensible home you can obtain when everything goes black.

Make certain to dig some trenches and trap holes.

If you put some human of animal crap in the end of the stick or knife you use, cause unlike the Walking Dead ain’t gonna be any ammo, it leads to septic infections.

You never want to leave dead bodies on the lawn either they breed disease and vermin.

You really need to research SCAFISM and understand proper placement so strangers looters avoid your now claimed property.

Remember this in 2028 and trade only for canned goods and NEVER trade for sex because NO ANTIBIOTICS!

Anecdotally, the job market here in the Northeast seems to have tightened in the last month or two. I know a lot of young people entering the work force are struggling to find jobs.

“Last month or two?” My experience living in the CT area is the job market became weak going back a couple years ago. The only thing that’s been holding up the CT economy the last few years is all the immigrants moving in with money. Just my opinion.

My small WNY town has no jobs and one of the last big time employers suddenly shut down due to Canadian tariffs.

But we have a whole bunch of homeless and mentally ill.

Pretty much sucks seeing the rise in gun violence as well.

No help will ever come our way.

But hey the homeless built three shanty towns in 2024.

Money is only given to those that already have it. This is the central premise of capitalism.

Only Fans.

People don’t recall the reason for Farmaid.

The banks loaned small farmers money and later suddenly called it in, much like 1893.

These farms were rural with the nearest cities being 300+ miles away, meaning the nearest jobs.

Because the farms went under and no one could afford the commute many working folk went on welfare.

These were the fly over states. The small farms were purchased by agribusiness and 60 minutes did a segment on the devastation.

But you know hey history only started yesterday.

I agree with DTJ. When my research department in CT was shuttered in 2024 after only 3 years of starting, I had 5 on-site interviews in CT and no offers. I ended up taking a job offer requiring relocation to a business friendly / tax friendly state. The state did away with tenure for teachers and has a goal of reducing income tax to 0%. There is an effort underway to allow people to claim private school tuition deductions on tax returns, but it will be short lived when income tax is 0%. I could see a school tax voucher system where a property owner can direct their assessed school tax to public or private schools of their choice.

Declining mortgage rates are not likely. This related article details what’s going on with US debt sales wrt who is buying and who is unloading US debt. The fed is losing money as it has not made a remittance to the treasury in a few years, and it is becoming a larger player in debt purchases. For more details see the linked article:

International Countries have only bought 10% of total new debt over 18 months | SchiffGold

Our country is broke and Trump declaring we have the strongest economy ever, even better than his first term, is a blatant lie. This post details one the the many problems. Our current fiscal problems first manifested with the guns and butter programs of the late 1960’s. The exposure mechanism was foreign central banks converting dollars for gold putting pressure on our gold reserves that backed the dollar. Rather than fix the problem, Nixon closed the convertibility ‘temporarily’ via executive order removing the last bit of discipline on congress to spend within its means. Deficit spending has generally trended up since and been exacerbated by artificially low interest rates set by the fed. Had the fed let markets set rates, the debt service burden would have much higher forcing congress toward more fiscal sanity. We would still be in a mess, but potentially not as severe in my opinion.

Bottom line, housing and about all other economic problems are not going to get better without first getting the federal spend below revenue on a continuous basis. It will be painful, but not doing so postpones and only makes the pain worse when the problem is finally confronted voluntarily or involuntarily.

Balancing the budget is never going to happen. Not even close. Even bringing the debt to a lower percentage of GDP won’t happen. It’ll go parabolic until collapse, and collapse will mean confiscation from all plebes and bare subsistence on CBDC. Also, Soylent Green is people!

So Soylent Green is people. Do you know about the active Cannibal community? Not only people who want to eat people but people who want to be eaten.

Goog;e some of the strange crap related to that practice.

Unfortunately there is absolutely no way to insult anyone in the 21st century because all the insults are normalized these days.

Best one may do is use the wrong pronoun.

AND this pisses me off, there are TWO biological sex and Hermaphrodites.

BUT gender runs the spectrum from male/male to female/female.

I see people confuse sex and gender in damn near every article written.

Ladyboys and Polynesian Third genders are not to big on western Tranny in your face mentality and don’t adopt it.

And C.M. Kornbluth’s The Marching Morons inspired Idiocracy!

Didn’t Turkey just dump all treasuries and china has been dropping them at a record pace while buying Gold at the same rate.

Oddly enough someday these wii be remembered as the good old days.

and whats in that 2 car garage?

https://gizmodo.com/as-1-million-new-car-buyers-vanish-from-u-s-economy-a-new-car-increasingly-becomes-a-distant-dream-2000765365

Read about the 2027 mandatory spy cameras mandated for every new car, eyes flick from the road and a warning goes off.

Also is the mandatory shut off for those of us not using ten and two but the gangster lean.

fake eye contact lenses to beat the monitors, coming soon to an economy near you?

A bunch of Chinese made crap accumulated over the years, usually.

yet numerous plans in Florida tout building hundreds and hundreds of new homes

They are probably needed… but the people that need them can’t afford them.

So that’s housing and healthcare, the other leg of the stool is food. How expensive does it get before people start going hungry?

The Golden Age continues…

After the collapse people will simply claim them.

They are still building massive developments (and I mean MASSIVE) in the outlying areas of Orlando. Old ranchlands, citrus/blueberry farms, and scrub prairie are being bulldozed at all points of the compass from central Orlando. An hour north, the retirement community of The Villages has bulldozed thousands of acres of land for more houses. If this continues, there will be one megapolis from Tampa to Daytona and from Ocala to Kissimmee.

My parents live in the Villages and you’re correct… they’re still gobbling up land and building like crazy. The Villages has reduced the options for home type and interior/furnishings to the basics for new buyers though, which I think is their way of trimming a bit of the fat for themselves and buyers who are maybe a bit more stretched nowadays.

For fun read the Carl Hiaasen novels. Florida reporter who wrote.

The novels,fun reads, also background the never ending building and destruction of Florida.

This would be over at least a thirty year period.

Really sad jumps between novels regarding the utter greed and destruction.

Similar thing with a Russian author of the watch series Daywatch is the first I think but the background stuff over the roughly same timespan for Moscow and Russia is about the same as Hiaasens work.

The “consumer” is in a death spiral when it comes to housing. The capital cost and interest rate is a major issue for most but the real problem for those that have owned real estate for a long time know that insurance, property taxes, and maintenance are the real enemy now. In a few years it will be utilities (water, gas, electric).

Seniors get a tax break in some states on property taxes but they don’t on insurance and maintenance. And god help you if you live in a disaster prone state (California, Florida, Texas) where you need to carry additional insurance.

The other problem that no one is talking about is that local governments have based their budgets on inflated housing prices and assumed property taxes, if and when housing corrects down those budgets are all going to be blown to pieces.

There is no fix. Immigration crackdowns will only drive costs up across the board for everything I’ve listed. Tariffs, trade wars and other Trump nonsense will only make costs soar as well.

The only solution is a good exit strategy, move away, wait for the epic crash and grand boomer die off, then swoop in like a vulture and pick the best meat on the market.

Do worry, Trump & Walrus will find a way to make things even worse.™

Yes BUT I’m not seeing a lot of good from state and local government. There was just a local vote allowing yearly political COLA raises and refusal to lower the county clerks salary.

A few years ago the state cut funding to the city who then cut funding to the library.

The library cried and put ads about cutting back on services and not being able to hire aids. Belly up genpop/

NOT A SINGLE POLITICIAN OFFERED TO TAKE A 5% PAY CUT AND LIBRARY HEAD WAS PULLING 80k A YEAR!

Then the council people voted for raises, which failed that ear but were rewarded two years later.

80k is barely lower middle class now.

Maybe for household income, but in Texas and a lot of other places, 80k is a lot for one person.

Sure looks a lot like 2007-08 on those charts.

The 2008 bubble printed such a PERFECT textbook chart (on this dataset especially). Flagpole, bear flag, flagpole, bottom. Now that “everyone” has access to chart data, we get the messiest looking bubble of all time, messy enough for people to constantly deny it exists.

Hockey stick?

They denied it last time too.

I suspect fewer and fewer people are ready to take on monthly payments they can barely afford, expecting rates to fall and enable them to refinance into a truly affordable payment.

They’re considering the fine, affordable communities you can find in the woods behind certain big box stores.

Under bridges.Then they roam at night like zombies. All with back packs, strollers, and kids wagons.

Imagine large amounts of inflation for 5 years and counting….who would have thought there’d be problems!?! No one, and I mean NO ONE is willing to accept any lowering of price on goods, services, stock, real estate, gold, silver, oil, etc….Until there is a requirement to blink, aka enough stress in the system without the immediate government backstop that is likely to come with the whining of prices finally relenting after 17 years, well, nothing gonna change except rising stress levels with those prices.

It feels like 2005 and 1999/2000 with the partisan political polarization that started in 2016 all rolled up into one ball. Just wonder what unforeseen event will trigger the tipping point of stress.

Despite lots of folks getting uber wealthy there’s lots of folks under greater pressure. Someone will have to blink. Hasn’t happened in a looooooong time.

Anecdotal piece: brother getting divorced, thankfully, despite having to pay out a huge amount to part, he’ll be able to retain his 2.4% mortgage as his is the only name on the note. Had he been forced to sell/refinance, he would have paid nearly the same amount for half the house. How long ago did he buy? 7 years but refinanced shortly thereafter. Imagine having to pay 6.75% instead of 2.4 with sellers unwilling to take less.

What a damn mess.

It’s only a mess because the government keep bottling up the free market. The natural cleansing forces are continually held at bay.

You mean economic collapse right?

I mean reversion to the mean, in all asset classes, including PMs. For real estate that would be the mean relative to incomes and also the mean relative to rents.