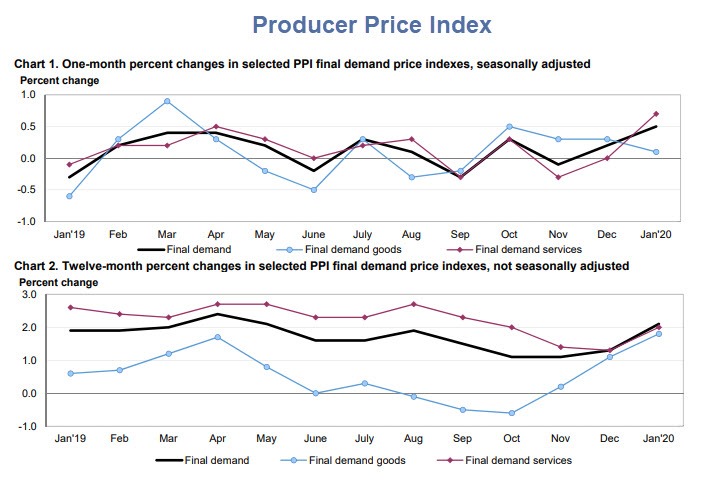

The BLS reports the Producer Price Index for final demand advanced 0.5 percent in January.

Final Demand Services

The index for final demand services climbed 0.7 percent in January, the largest increase since rising 0.7 percent in October 2018. In January, margins for final demand trade services advanced 1.2 percent, and prices for final demand services less trade, transportation, and warehousing moved up 0.6 percent. (Trade indexes measure changes in margins received by wholesalers and retailers.) In contrast, the index for final demand transportation and warehousing services fell 1.6 percent.

Forty percent of the January increase in the index for final demand services can be traced to margins for apparel, jewelry, footwear, and accessories retailing, which jumped 10.3 percent. The indexes for machinery and vehicle wholesaling; health, beauty, and optical goods retailing; inpatient care; guestroom rental; and portfolio management also moved higher. Conversely, prices for airline passenger services decreased 5.8 percent. The indexes for professional and commercial equipment wholesaling and for wireless telecommunication services also declined.

Final Demand Goods

Prices for final demand goods inched up 0.1 percent in January, the fourth consecutive rise. Leading the January increase, the index for final demand goods less foods and energy climbed 0.3 percent. Prices for final demand foods advanced 0.2 percent. In contrast, the index for final demand energy fell 0.7 percent.

Much Hotter Than Expected

The Econoday consensus was for a 0.1% rise with a range of -0.3% to +0.2%.

Economists were not in the ballpark and there was an upward revision in December from +0.1% to +0.2%.

Bond Market Reaction

- Yield on the 30-Year Long Bond: Flat

- Yield on the 10-Year Note: Flat

- Yield on the 2-Year Note: Up 1 Basis Point

- Yield on the 3-Month T-Bill: Flat

The reaction to the PPI was as interesting as the move itself.

Despite what appears to be inflationary pressures, the bond market just sat there and stared.

Coronavirus Impact?

It always hard to say why the market did any particular thing, but a huge coronavirus-related supply chain disruption is coming up.

Yesterday I commented Largest Shipping Decline Since 2009 and That’s Before Coronavirus

In light of recent events, perhaps the January PPI data is now too old for a reaction.

Note that Half the Population of China, 760 Million, Now Locked Down

Supply chain disruptions have barely started.

Mike “Mish” Shedlock

Great

[Google](https://www.google.com)

Students in London can pay someone to do my university assignment UK I provide the best academic writing help online at cheap price in the UK.

Nice that every student can have the best Nursing Essay Writers UK online now and can make the good academic grades in the university as well as in the final semester.

The economic politburo will make sure the revisions next month will smooth out these statistical “aberrations” so they can tow the line to fit their desired economic narrative. This way they can continue to finance their trillion dollar deficits at negative real interest rates and continue f’ing over savers.

“Supply chain disruptions have barely started.”

…

Yes, and easy to see why a bump in PRODUCER prices.

Good luck passing them onto end users.

How much will demand wilt?

It has been an ongoing theory in recent financial news that the market is still headed up despite SARS-COV-2 because central banks will print money to keep asset prices up. I wonder if that is actually an option. In a virus supply disruption scenario, goods will be more scarce. If more money is added to the system as that happens, there will be both more money and fewer goods simultaneously, which should strongly boost inflation. Can the Fed and other banks really print their way out of this or do they have to weather it without printing? Any thoughts?

Most governments are money printing so maybe it balances out a bit. A major currency that isn’t being printed is Gold & that’s been going up.

Bond markets have been “Nationalized” by the Central Banking cartel and no longer react to economic news or reality, for that matter.

We’ll see. Imo, the reality coming down the pike is a deflationary bust (followed by inflation, probably). Avenue for bond (smart money) rates is lower.